- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 25, 2025 at 11:00 am

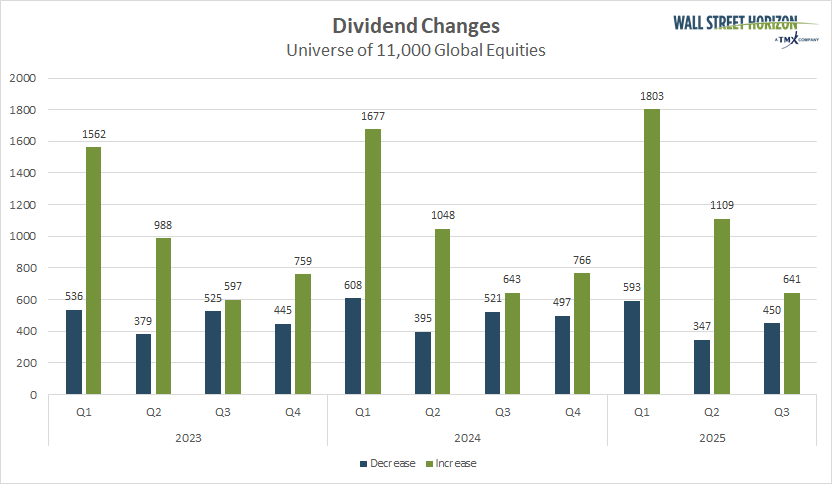

Dividend-increase announcements are on the rise. According to the Wall Street Horizon research team, 71.9% of all dividend changes have been positive so far in 2025. That tops the comparable year-to-date figures of 68.8% and 68.6% from 2024 and 2023, respectively. In all, the current-year hike tally is now 3,553. Perhaps the bump is not surprising, given that the global bull market is about to turn three years old.

Source: Wall Street Horizon

More dividend payouts mean investment teams need to adjust stock prices to reflect these corporate actions properly in order to conduct time-series analysis. TMX’s Price Adjustment Curve (PAC) provides price adjustments applicable down to tick level prices or even orders, and below you can see the number of recorded adjustments for North American dividends have been steadily increasing. Q2 2025 recorded 11,194 such price adjustments, the largest second quarter tally in our five years of data. With one week left in the current quarter, the Q3 2025 total stands at 8,904.

Source: TMX Datalinx

October also marks the start of the third-quarter earnings season. The big banks begin reporting profit numbers on October 14, with JPMorgan Chase (JPM) providing the unofficial kickstart.

In general, a softer greenback is a profit tailwind for large multinational corporations as they repatriate their overseas sales from foreign currencies to the dollar. Indeed, S&P 500 earnings per share estimates are at fresh highs. It’s against that backdrop that companies, despite the ongoing tariff threat, are willing to boost their dividends. It may leave you and other investors wondering: What could disrupt the steady diet of dividend-hike announcements?

As always, we can put the spotlight on the consumer. August’s Retail Sales report, released last week, confirmed that household spending is resilient, a softening labor market notwithstanding. The so-called “core control group” of the U.S. Census Bureau’s consumption snapshot rose by 0.7% over the middle month of the third quarter, a crucial period for domestic retailers.1 The back-to-school shopping season was apparently a hit—particularly for e-commerce firms.

Robust consumer spending may hinge on the employment situation. We’ll know more about that next Friday once the September jobs report crosses the wires. Expectations could be low after back-to-back soft payroll gains, not to mention the steep downward revisions from the annual Quarterly Census of Employment and Wages (QCEW) report put out by the U.S. Bureau of Labor Statistics two weeks ago. Further labor-market nuggets could be found in next week’s multitude of employment indicators.

According to our Economic Calendar, with data licensed from Econoday Inc., August job vacancy figures via the Job Openings and Labor Turnover Survey (JOLTS) prints at 10 a.m. ET on September’s final day, the ADP private employment numbers come the following morning, and the now widely followed Challenger Job Cuts survey publishes on Thursday, October 2, in the premarket. Investors shouldn’t discount the importance of the Employment sub index readings within both the ISM’s and S&P Global’s Purchasing Managers’ Index (PMI) surveys. Those are in next week’s queue, too.

How the macro setting unfolds could determine companies’ capital allocation plans heading into 2026. We typically don’t see a high number of dividend-increase or decrease announcements in the second half of the year compared to the first half. A strong finish to 2025, though, and next year’s first-quarter sum could eclipse the Q1 2025 dividend-hike tally of 1,803.

And here’s why that’s significant: Investors increasingly prefer that companies return cash flow to them via share buybacks and dividend payments. That was one of the takeaways from BofA’s September Global Fund Manager Survey. Along with increased capital spending, there’s less desire from shareholders for firms to shore up their balance sheets.

So, will that wish come true? With U.S. corporate buybacks reaching $1 trillion in August, we may learn more on the dividend front soon.2 It’s very much a “watch what I do, not what I say” situation.

It’s hard to go a few minutes with financial TV on in the background without your ears perking up due to cautious words from CEOs and other business executives. One of the poster children for cloudy executive outlooks is undoubtedly Jamie Dimon, CEO of JPM. America’s banker routinely expresses trepidation regarding fiscal and other macro matters. Yet guess what big bank announced a significant dividend boost? JPMorgan.

On September 16, the world’s most valuable bank by market cap raised its quarterly dividend from $1.40 to $1.50.3 The press release came after a strong Q2 report issued back in July and the authorization of a new share repurchase program. Now the third-best-performing component of the Dow Jones Industrial Average on the year, JPM may have eyes on the $1 trillion market-cap figure. If it were to do so, it would join fellow Financials-sector stalwart Berkshire Hathaway (BRK.A) in that exclusive club.

And here’s something else to consider on the topic of dividends at this juncture of the economic cycle: Given the Fed’s apparent willingness to run the economy hot in terms of inflation, additional rate cuts may be in store not just in Q4, but throughout 2026. If that happens (and Treasury yields hold in check), it could make dividend stocks all the more attractive compared to bonds.

Dividend-increase announcements are tracking above year-ago levels and 2023’s pace. Even with shakiness in the labor market and some guarded outlooks offered by companies during the busy Q3 conference season, shareholders are being rewarded with growing quarterly payouts.

We’ll find out more in the weeks ahead—first from next week’s employment numbers, and second as third-quarter earnings reports roll in (assuming we are sticking with quarterly updates!).

—

Originally Posted on September 25, 2025 – Global Dividend Growth Accelerates as the Bull Market Turns Three

Copyright © 2025 Wall Street Horizon, Inc. All rights reserved. Do not copy, distribute, sell or modify this document without Wall Street Horizon’s prior written consent. This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this publication, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This publication is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities, including any listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. This publication shall not constitute an offer to sell or the solicitation of an offer to buy, nor may there be any sale of any securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction. TMX, the TMX design, TMX Group, Toronto Stock Exchange, TSX, and TSX Venture Exchange are the trademarks of TSX Inc. and are used under license. Wall Street Horizon is the trademark of Wall Street Horizon, Inc. All other trademarks used in this publication are the property of their respective owners.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Wall Street Horizon and is being posted with its permission. The views expressed in this material are solely those of the author and/or Wall Street Horizon and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

| EPAT Project")

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!