- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 17, 2025 at 9:01 am

By Todd Stankiewicz CMT, CFP, ChFC

1/ The Fed Takes Center Stage

2/ Why Yields Could Rise After a Cut

3/ A Warning From the UK

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

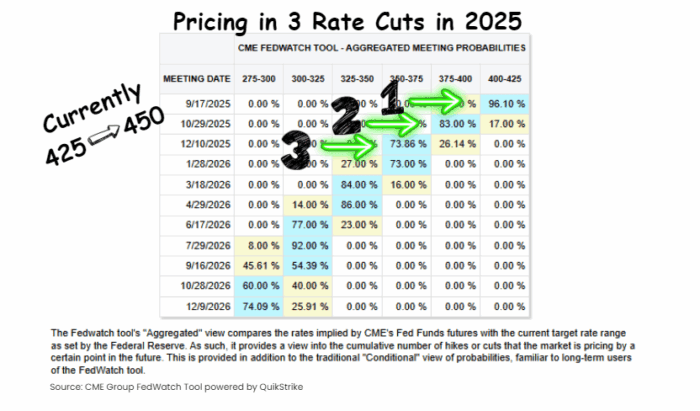

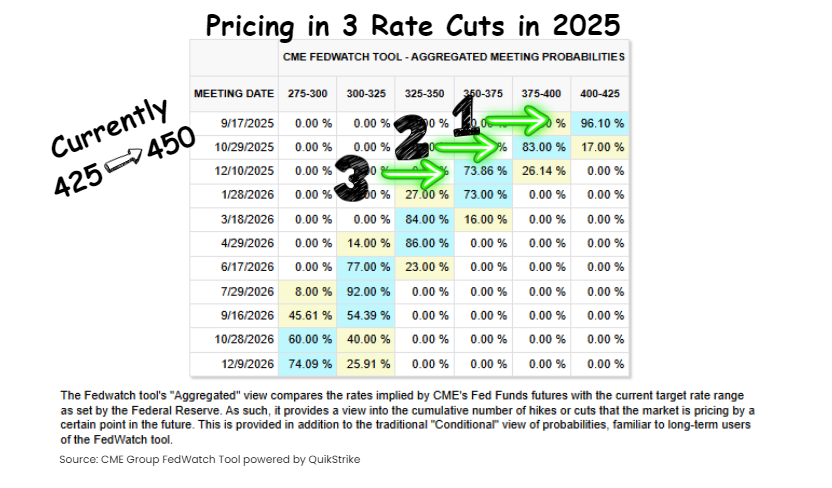

The Fed Takes Center Stage

This week all eyes are on the Federal Reserve. On Wednesday, the Fed is widely expected to announce its first rate cut in nine months, likely a 25 basis point reduction. While a larger 50 basis point cut is possible, that’s not the base case. Futures markets are pricing in a 96% probability of a 25 basis point cut, bringing the federal funds target range down from 4.25–4.50% to 4.00–4.25%.

Looking ahead, markets now expect three total cuts in 2025. One each in September, October, and December. The risk for investors is if the Fed doesn’t follow that path. A more hawkish tone or slower pace of easing could disappoint markets. Much of the recent rally has been fueled by expectations of easier policy, so any deviation could spark volatility.

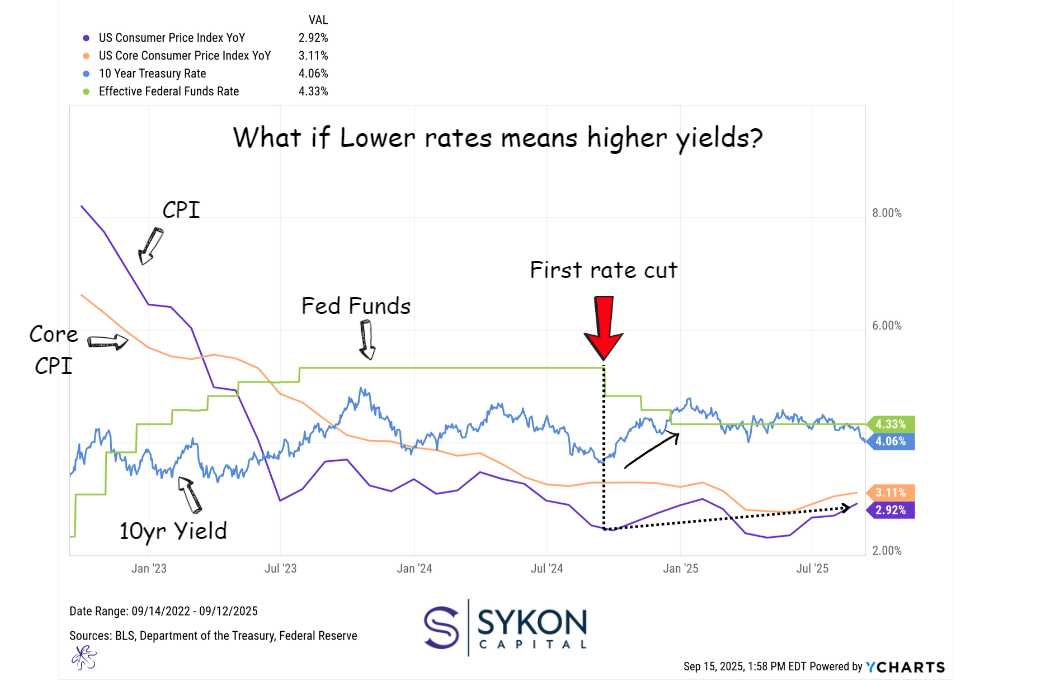

Why Yields Could Rise After a Cut

It may sound counterintuitive, but a Fed rate cut doesn’t guarantee lower borrowing costs. In fact, the opposite can happen. Back in September 2024, when the Fed cut rates for the first time in that cycle, the 10-year Treasury yield actually moved higher afterward. Mortgage rates, which are tied to the 10-year, followed suit. Many borrowers waiting for relief instead saw costs rise.

We may face a similar setup now. Inflation has not continued to trend lower since last year’s cut. Both headline CPI and core CPI have ticked higher from their recent lows. If the Fed cuts too early, it could stoke inflation pressures, pushing yields higher. In 2024, the 10-year yield bottomed just before the Fed’s move, and then climbed sharply. It’s a reminder that “rate cut” doesn’t always equal “lower rates” for consumers.

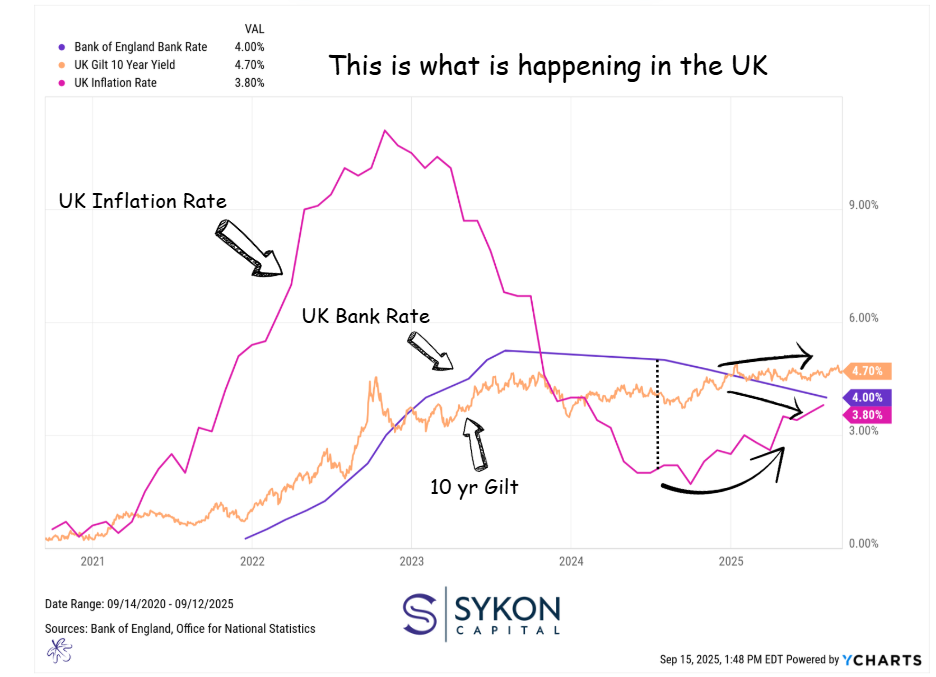

A Warning From the UK

For a live example, look across the Atlantic. The Bank of England has been cutting rates, but the 10-year gilt, the UK equivalent of the Treasury , has been moving higher. At the same time, UK inflation has picked back up from its recent lows, leaving policymakers stuck between slowing growth and persistent price pressures.

That dynamic looks familiar. Lending rates in the UK, tied to the gilt, haven’t eased, they’ve climbed. At the same time, savers are earning less on short-term deposits because policy rates are lower. The result: households face higher borrowing costs while earning less on savings.

The lesson applies here too. Don’t assume a Fed rate cut will automatically make life cheaper. Lending rates are driven by longer-term yields, not the Fed’s overnight rate. Cuts can relieve market stress, but they can also reignite inflationary fears and push borrowing costs higher.

—

Originally posted 16th September 2025

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Municipal Bonds are only available from Interactive Brokers for IBKR LLC, IBKR Canada, IBKR Hong Kong, IBKR Australia and IBKR Singapore entities.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!