- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 14, 2025 at 10:36 am

1/ Bear Market Averted, Now What?

2/ China Tariff Pivot

3/ Earnings Season

4/ Retail Sales

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

Bear Market Averted, Now What?

Wall Street got its much needed relief rally last week after a terrifying three day period – Thursday to Monday morning – that saw stocks fall over 14% in the quickest drop since the October 1987 crash.

As we begin this week, again, traders will be fixated to social media feeds and the newswires for the latest on this never ending saga of “tariffs-on, tariffs-off”. Scroll down and we will recap the crazy highlights in the week in review.

One thing the current administration has been great at is keeping market participants on their toes. I struggle to write this note as the news keeps changing. Sometimes it feels as if this administration is just making things up as they go along and using social media and market reaction to gauge if their ideas are good or not.

Let’s look at where we are before doing a deeper dive and the three things traders will be watching for this week.

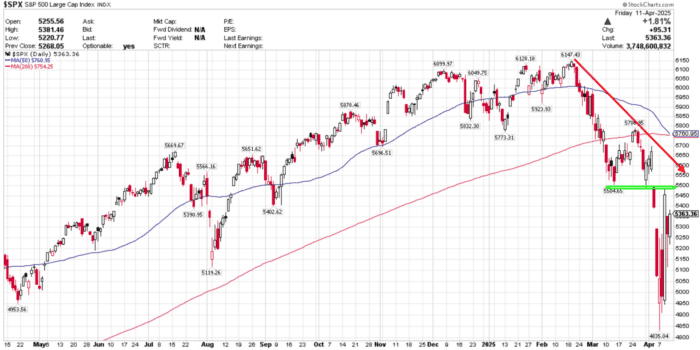

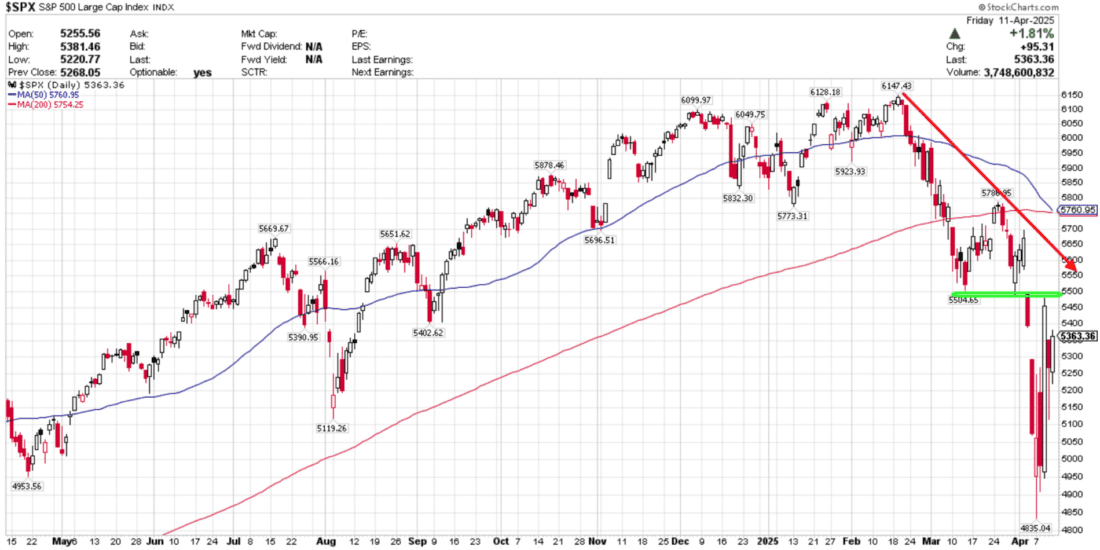

Bear market averted, now what? We never hit “official bear market territory” as the S&P 500 traded down 20% on an intraday basis on Monday, but never closed down 20% from its highest close.

Technically, we got a much needed relief rally from a very oversold condition. We still have room to run, but there are two key levels of resistance to clear before feeling we are out of the woods.

Traders will be watching the 5500 level closely. It was the prior support level in March from which we broke below on April 2nd. Step one to a recovery would be a close above this mark.

Step two is that flattening 200-day moving average at 5760. That’s 7.4% higher than current levels and if the market can get back to that area expect selling pressure to pause any rally.

As for the downside, battle lines have been drawn. The S&P 500 made higher lows each day last week. 5000 seems to be a psychological level to watch, but 4950 is the key closing low to stay above if there were to be a re-test of the lows.

China Tariff Pivot

China Tariff Pivot. Speaking of ever changing news, Chinese tariffs have been all over the place and the focal point in the trade war. Heading into the weekend the President increased import duties on goods from China to 145% but reduced those on imports with most other countries to a baseline 10%.

Last Wednesday, the President announced a 90-day review period to negotiate better deals with most nations initially impacted by his April 2nd “Liberation Day” announcement and the market reacted quite positively with the S&P 500 ending the week higher by over 5.6%.

However the news didn’t stop there. On Saturday, the Trump administration announced that smartphones and computers will be exempted from reciprocal tariffs. This move should help tech companies like Apple, which makes most of its products in China, continue to rebound in Monday’s trading.

Also announced were exclusions for other electronic devices and components which include semiconductors and devices used for storing data.

Yet on Sunday, the U.S. Commerce Secretary, Howard Lutnick, said on ABC’s This Week that recent exemptions for smartphones and other electronics from new tariffs “are temporary”.

So again, despite some positive news that could lift some beaten down sectors, confusion and uncertainty remain the theme in Washington as proven by the Commerce Secretary’s comments.

Earnings Season

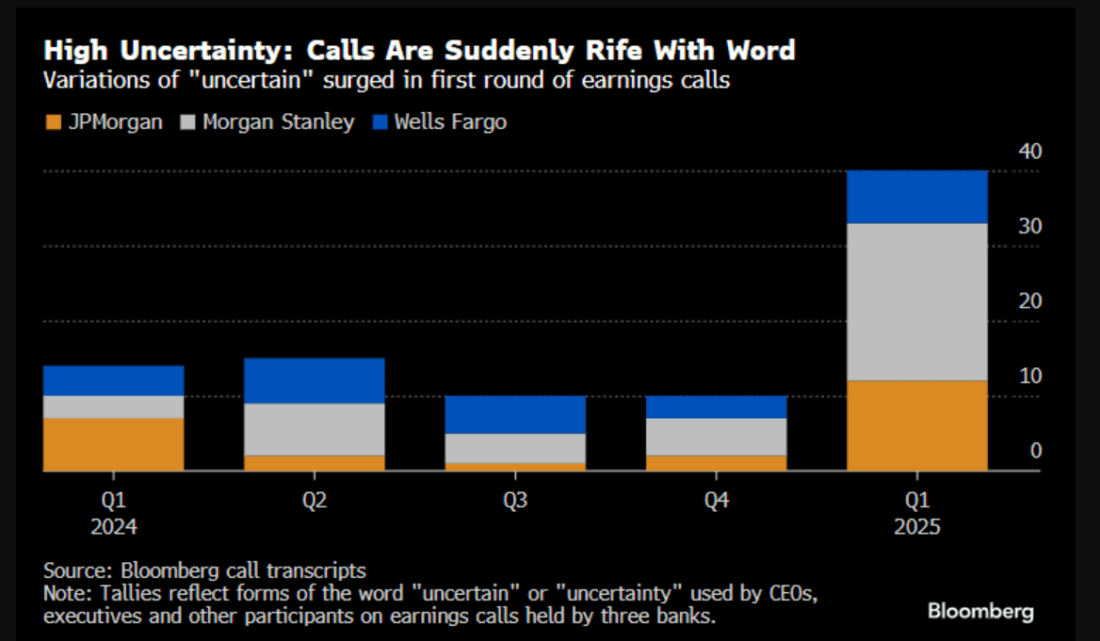

Earnings Season. The banks officially kicked off earnings season on Friday as J.P. Morgan (JPM), Morgan Stanley (MS) and Wells Fargo (WFC) announced their results.

This week the slate of reports grows louder but one common factor may persist – lack of guidance.

Last week, during the three earnings calls of the banks mentioned above, the word or a variation of the word “uncertain” was said 40 times! Expect that surge to continue as companies struggle to deal with the constant changes when it comes to tariff policy out of Washington.

That will directly impact the analyst community covering these stocks so expect cautious outlooks going forward as we head into Q2.

Retail Sales

Retail Sales. Analysts are looking for retail sales numbers to potentially surge as shoppers attempted to front-run the announcement of tariffs. The biggest benefactors should be imported autos and parts as prices were expected to surge by close to $5000 per vehicle.

According to Bloomberg data, despite an uptick in some big ticket items, investors may pull back on most discretionary items. Real personal spending continues to cool, but overall an uptick may be likely due to the fear of the April 2nd “Liberation Day” announcement.

Overall, reaction to the news will continue to be overshadowed by the continued headlines out of Washington. We experienced that last week positive inflationary data in the CPI figures made little impact to the market despite coming in better than expected.

Continue Reading at Freedom Capital Markets…

—

Originally posted 14th April 2025

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!