- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 28, 2023 at 12:15 pm

One of the global markets’ big “will they or won’t they” questions was resolved early this morning when the Bank of Japan (BOJ) announced a relaxation to its yield curve control (YCC) policy. The simplified version is that instead of buying Japanese government bond’s (JGB’s) to ensure that rates would not exceed 0.5%, they would now relax their purchases to yields of 1%.[i] This had the potential to send seismic ripples throughout global stock and bond markets. Instead, much of Asia and Europe yawned, and US traders decided it was not sufficient reason to disrupt the ongoing party.

There are several reasons why this move could have, or even should have, been a major event for global markets. One is philosophical. The BOJ is the last of the world’s major central banks to maintain an accommodate monetary policy. YCC is a form of quantitative easing (QE). The central bank is buying bonds, meaning that the money that they spend is going into the broader financial system. Compare this to the Federal Reserve, which is actively engaged in quantitative tightening (QT)[ii] by allowing notes it holds on its balance sheet to mature and not re-investing all the proceeds. The relaxation of the YCC target still means that QE remains in effect, just less aggressively.

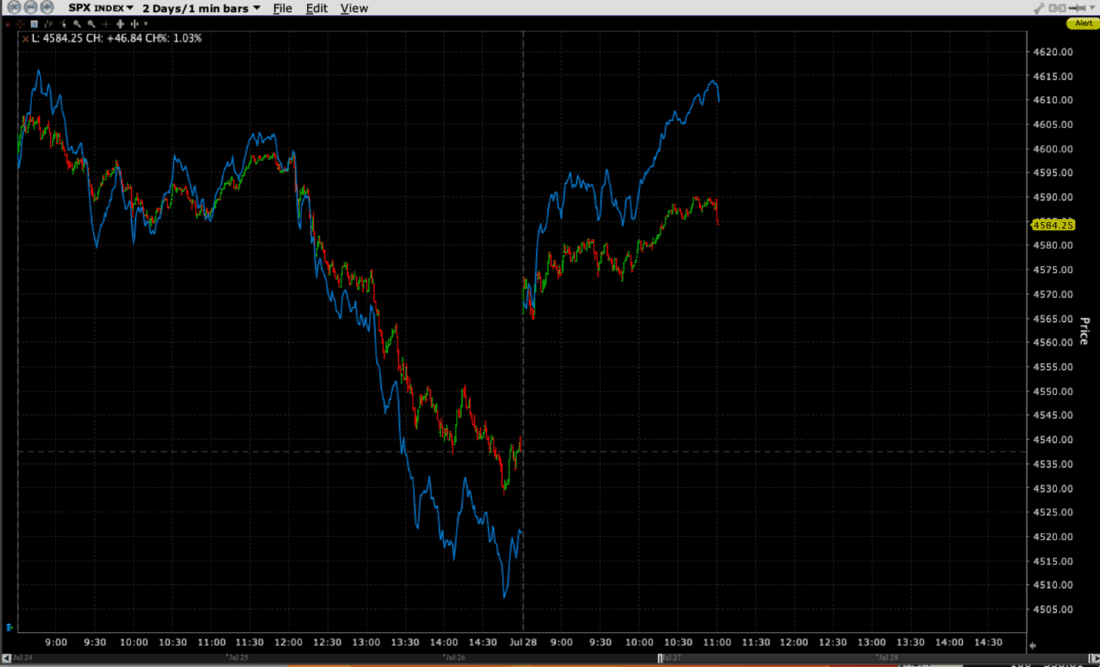

There was a bit of a head fake involved with the BOJ’s move. Last week, there were reports that the BOJ would be unlikely to change its YCC policy. The stories mollified traders, and at least one pundit (ahem) publicly changed his view that the BOJ meeting would be the most meaningful of this week’s Federal Reserve/European Central Bank/BOJ trifecta. Then, around midday yesterday, a report from Nikkei stated that the BOJ would indeed consider allowing a relaxation in YCC. That led to a sharp drop in major US indices during afternoon trading:

Source: Interactive Brokers

As we can see, SPX has recovered most of its losses and NDX has surpassed yesterday’s highs by midday. So why the head fake?

The decline was caused by concerns about carry trades. It is common for leveraged investors to borrow in low-rate currencies, such as the yen, and use the proceeds to buy higher yielding assets – either fixed income or equities. A rise in Japanese rates in theory should bolster the yen against other currencies. In turn, that could require those traders involved in carry trades to shrink their positions. Hence, the stock market’s reaction. I was asked for comment late yesterday afternoon, and responded thusly:

There’s a reason they call shorting JGBs ‘the widow maker.’ It’s been logical to short JGBs but it never works. So when it does, watch out because no one is prepared for it. And undoubtedly we have seen carry trades borrowing cheap yen to buy stocks on leverage. If YCC ends, those can get nasty quickly. Hence the reaction. Plus, BOJ is the last of the easy money central banks. The last domino.

Despite the head fake, Japanese investors, and those in much of the world didn’t end up reacting all that negatively. Indeed, JGB rates rose, but we hardly saw a wholesale rush from the exits by leveraged carry traders. Perhaps this is because we have seen YCC adjustments before, something we wrote about in December in a piece called: “The “Widowmaker” Pays Off as the Last Central Bank Domino Falls.” The yen strengthened briefly, but only by about 2% and is now back to yesterday’s levels. Even at its worst, the currency move was not enough to shake sanguine investors.

Another factor could be that the BOJ surprise was offset by vague but meaningful reports that the China Securities Regulatory Commission convened a meeting of some of the country’s brokerage houses to solicit ideas for boosted Chinese stocks. Remember, traders respond far more aggressively to reports of stimulus than contraction. The iShares MSCI China ETF (MCHI) is up over 4% today, to name one example; along with good earnings and positive comments from Intel (INTC), those were more than enough for US tech stocks to resume their months-long advance.

Was the BOJ a big yawn, or do today’s moves show that whiffs of positive market intervention outweigh concerns about rising rates? It’s tough to untangle the two. But either way, the inertia market remains in place. The BOJ was not a significant enough force to influence the market’s inertia for more than a few nervous hours.

—

[i] Remember, higher bond yields mean lower bond prices, and vice versa.

[ii] Sorry, I think I set a personal best for acronym use with five in the first two paragraphs

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!