- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 3, 2024 at 10:00 am

For the remainder of 2024, supply-side constraints, geopolitical risks and global economic trends will be in focus

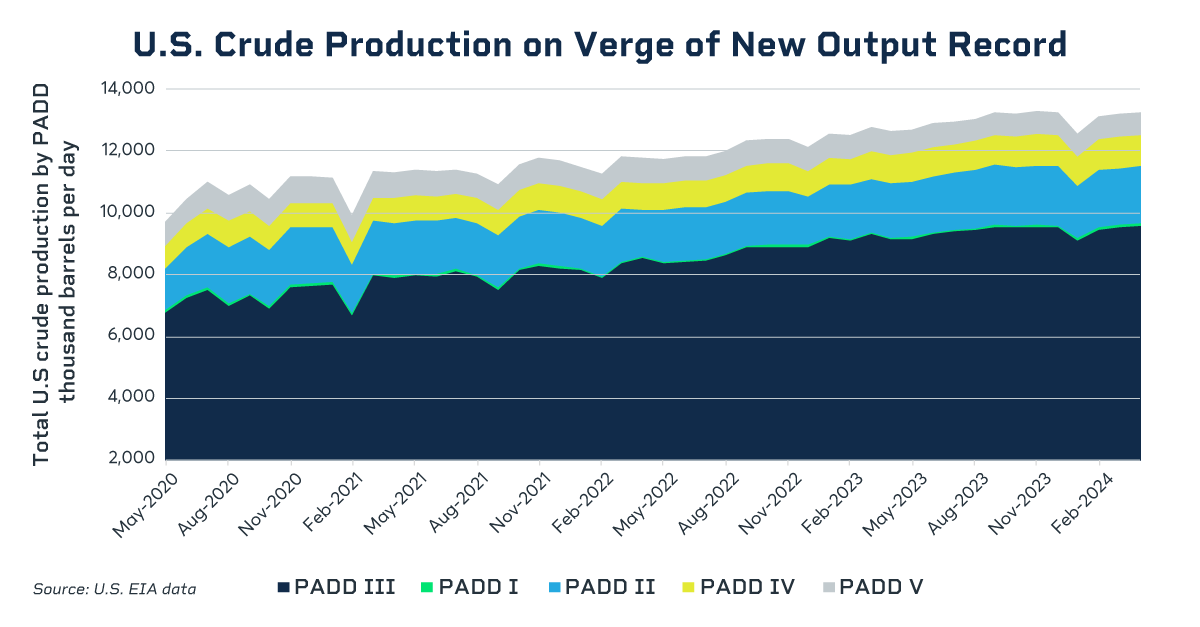

The U.S. is both the top producer and consumer of crude oil

As we approach the latter part of the year, crude oil prices remain under close scrutiny due to a combination of supply-side constraints, geopolitical tensions and changing global demand patterns. Several factors will likely influence the price and availability of crude oil, and understanding these dynamics is crucial for investors, policymakers and businesses alike.

One of the most significant factors influencing oil prices this year is the series of production cuts from OPEC+, a group of oil-producing nations led by Saudi Arabia and Russia. These countries have strategically reduced output to manage prices in a volatile global market. In particular, Saudi Arabia has extended voluntary production cuts several times to maintain a floor under prices, attempting to stabilize the market despite uncertain global demand.

Before the U.S. emerged as a major global producer, the strategy of production cuts from OPEC+ would typically lead to price spikes. However, in recent years, it has been less effective. The effect of recent cuts on crude prices has been mixed, prompting concerns about the negative effects on certain economies within the OPEC and OPEC+ groups. This is why analysts will likely continue to closely monitor any announcements of further cuts or changes in production strategy. Even a tiny shift can have immediate global effects on oil prices.

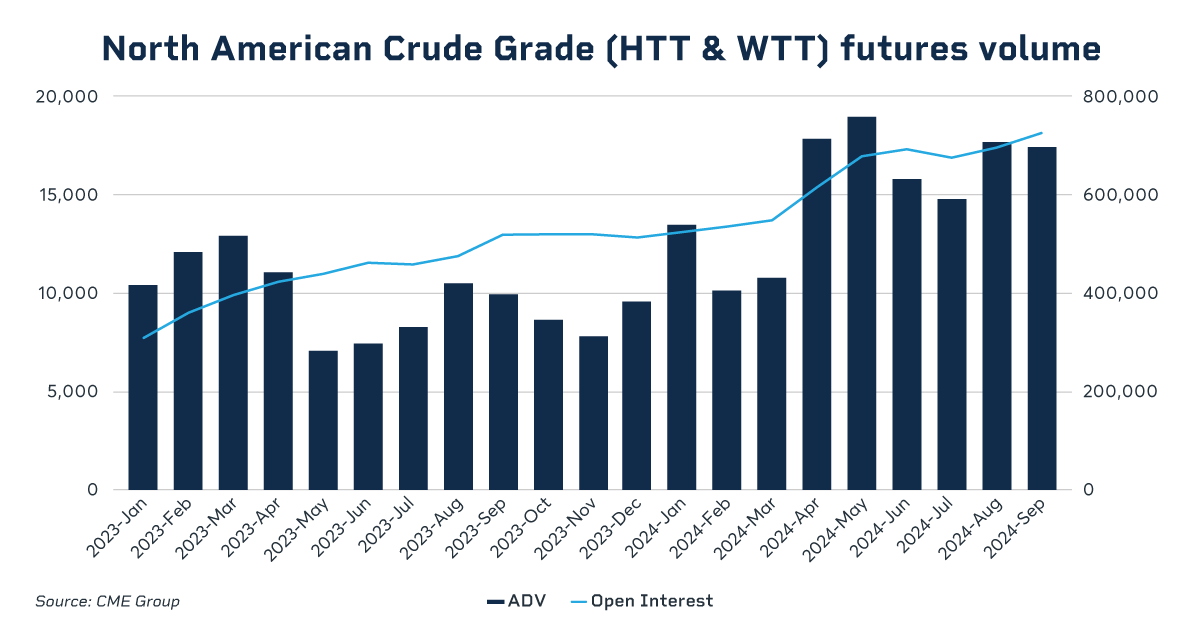

Amid the rise in U.S. crude oil exports, WTI has never been more relevant. This has prompted more market participants to turn to WTI-linked futures contracts to hedge U.S. crude basis risk, and the combined average daily volume in WTI Houston (HTT) and WTI Midland (WTT) reached a record over 19,000 contracts in October, while average day open interest also reached a record 719 contracts.

Geopolitical tensions have a long history of influencing the oil market, and 2024 is no exception. The heightened instability in several key regions could potentially disrupt global oil supply.

Middle East Tensions: Any diplomatic or military conflict could bring volatility to the crude oil markets if it involves a crude oil-producing nation. One country that crude oil traders and investors are watching is Iran, a large oil producer. The key is the actual disruption in oil supply, not just the implication of potential disruption, as those moves tend to be short-lived and tend to correct themselves very quickly.

Russian-Ukraine War: The Russia-Ukraine conflict continues to impact global energy markets. While Russia remains a major exporter of crude oil, Western sanctions have led to changes in the flow of oil, with more of Russia’s supply going to countries like China and India. Any escalation in the conflict or new sanctions targeting energy exports could have ripple effects through the market.

African and South American Instability: Political instability in oil-producing nations such as Libya, Venezuela and Nigeria could further exacerbate supply disruptions. While these countries may not individually have the same production capacity as the larger producers in OPEC, sudden disruptions could still impact global supply chains and prices.

Geopolitical risks remain a significant consideration in the oil markets, with the potential to create sudden and sharp price fluctuations.

The U.S. remains the largest oil producer in the world, mainly due to its significant shale oil reserves and the fracking industry. Shale oil production in the U.S. has helped offset some of the global supply cuts initiated by OPEC+ in recent years. Still, there are questions about how much more production capacity is available in the short term.

Fracking companies have been somewhat cautious in ramping up production. After years of aggressive drilling, many companies now focus on profitability rather than growth, contributing to slower output increases even when prices rise. Environmental regulations and concerns about the sustainability of production have also led to slower growth in the sector.

Still, any major shifts in U.S. shale oil production could counterbalance OPEC+ production cuts. If prices rebound, there could be more pressure on U.S. producers to increase output, especially if inflation ticks up again.

China’s demand for fossil fuels has been declining due to economic factors. However, the People’s Bank of China recently announced sweeping stimulus measures in September, which could affect oil demand positively in the jurisdiction. Monitoring whether the stimulus works is essential, as the Chinese market significantly impacts crude prices.

In September, the U.S. Federal Reserve cut its short-term interest rates by 50 basis points, which some people saw as a signal that the U.S. central bank is worried about future growth. However, the Fed has firmly rejected the notion that it believes the U.S. economy is in trouble, instead expressing the committee’s belief that the policy was too restrictive for the “soft landing” already in process.

If, however, a recession does occur, as some analysts believe, U.S. demand for crude oil will likely drop off. The U.S. is far and away the largest consumer of crude oil, and while there’s a certain baseline demand that is stable, a weaker economy still means less overall demand.

While short-term factors like production cuts and geopolitical tensions tend to dominate headlines, the longer-term shift toward renewable energy and lower-carbon energy sources will continue to shape oil markets. Many countries, particularly in Europe, are accelerating their transition from fossil fuels, aiming to reduce their dependence on oil and gas as part of climate change mitigation strategies.

This energy transition leads to investments in renewable energy and electric vehicles (EVs), which should reduce oil demand over time. The International Energy Agency (IEA) and other energy forecasters have already predicted that peak oil demand could come sooner than expected due to the rapid growth of renewable energy sources, EVs and energy efficiency improvements.

However, this long-term trend doesn’t negate the immediate need for oil in many industries and countries. The transition to a cleaner energy economy will be gradual, and oil remains a cornerstone of global energy consumption.

—

Originally Posted November 26, 2024 – Six Areas to Watch in Crude Oil Markets

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

The area to be in is leveraged midstream closed end funds like KYN, EMO and SRV. They are paid on volume for transport and storage.