- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 9, 2025 at 11:59 am

Three of U.S. President Donald Trump’s top aides will meet with their Chinese counterparts in London on Monday for talks aimed at resolving a trade dispute between the world’s two largest economies that has kept global markets on edge.

Agricultural markets were supported last week on trade optimism after Trump and Chinese leader Xi Jinping confronted weeks of brewing trade tensions in a rare leader-to-leader call.

On the weather front, rains helped improve soil moisture in parts of the U.S. Southern Plains and the Midwest, according to forecaster Vaisala.

But dryness lingers in north central Kansas, southeastern Nebraska, Iowa, southern Minnesota, northern Illinois, northern Indiana and western Ohio, according to the forecaster. That dryness could stress germination and early growth of corn and soybeans.

Ratings for French wheat and barley crops edged lower in the week to June 2, extending a decline in the past month as a dry spring has left northerly regions parched, data from farm office FranceAgriMer showed on Friday.

Ukraine’s grain exports in the 2025/26 July-June season are expected to fall to 35 million metric tons in the worst scenario against a forecast of 40 million tons in 2024/25, following a lower harvest, its first deputy agriculture minister Taras Vysotskiy told Reuters on Friday.

For the fourth consecutive session, Corn futures finished higher, with the July contract settling Friday at 442’4, up 3’0. Across all maturities, a heavy 548,738 contracts were traded, with 229,798 done in the July maturity. Overall open interest dropped 12,920, or 0.78%, to 1,640,337. July fell 32,843 (5.46%), finishing at 569,163.

July corn futures had a nice move higher on Friday but that firm trade has so far failed to materialize any meaningful follow-through with last week’s highs and the 20-day moving average acting as first resistance from 448 1/4-451. Of the Bulls can achieve consecutive closes back above this pocket, a move back towards 463 1/4-465 1/4 would be the next upside target. On the flipside, a break and close below last week’s low and a retest of the August contract lows could be in order, 421 3/4.

Resistance: 463 1/4-465 1/4***

Pivot: 448 3/4-451

Support: 433 1/4-437****

Option trading centered around the July 450 calls with 7,060 done and the Dec 370 puts with volume of 1,813. Options with the greatest open interest are the Sep 500 call with 40,319, and the Dec 400 put with 25,217.

Corn implied volatility ended the session up as CVL rose by 0.71 to close the day at 25.80, a one week high. The 30-day historical volatility closed the session unchanged for the day nan% to nan%. The CVL Skew closed the session moderately higher, gaining 0.48 to finish the day at a one month high of 4.73.

(Updated on 6.9.25)

Below is a look at historical price averages for December corn futures on a 5, 10, 15, 20, and 30 year time frames (Past performance is not necessarily indicative of future results).

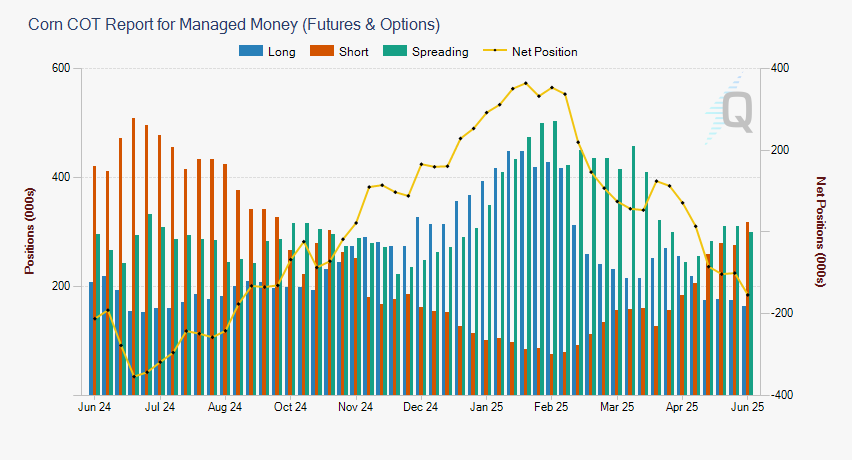

Friday’s Commitment of Traders report showed Funds were net sellers of 53k futures and options contracts through June 3rd. This is the largest net short since September.

Enjoyed the report? Unlock full technical breakdowns and our daily take on crude, metals, livestock, grains, and equities—sign up through the portal today and don’t miss a move.

**Bias shift to Neutral / Bullish

Friday’s Settlement: 64.58, up +1.21 [+6.23%] for the week, +1.21 [+1.90%] for the day

The announcement of a US – China trade meeting in London propelled crude futures to finish at the highs of the day / week on Friday.

For the week, geopolitical risk and Canadian wildfires outweighed accelerated OPEC+ supply as Crude finally broke out of a two week trading range. Sanctions on Russian oil continues to bite global export supply as the war rages on.

Today, WTI Crude Oil is higher by +0.34 [+0.53%] to 63.52

Crude is holding ground into the U.S. open as traders wait on news surrounding the US – China trade talks. The White House has announced that Howard Lutnick and Scrappy Scott Bessent will attend. The London trade meeting will be the key driver for markets today. No major data releases are scheduled for today.

Markets are trading risk-on in anticipation of the meeting. Over the weekend, the breakup of Elon Musk and President Trump and newsflow around Elon’s problems within the White House garnered a lot of attention.

N/A

Futures have settled back up above our longer term pivot and point of balance as of Friday. Crude oil momentum was very apparent last week. We got OPEC+ accelerated supply hikes, pretty bearish fundamental news, and a breakout higher of the most recent trading range – pretty bullish price action. Bullish price action in the face of bearish fundamental news is a pretty good sign these markets want to go higher.

Keep an eye on price action today as markets look to establish a new trading range. We would wait to establish longs until news out of the London meetings. Rhetoric out of the Chinese will be interesting and this “breakout” could be short-lived if these talks break down.

For intraday trading, our pivot and point of balance is set at…

Enjoyed the report? Unlock full technical breakdowns and our daily take on crude, metals, livestock, grains, and equities—sign up through the portal today and don’t miss a move.

Video: https://youtu.be/X2kDjFPGQ3o

E-mini S&P (June) / E-mini NQ (June)

S&P, last week’s close: Settled at 6006.75, up 60.75 on Friday and 90.75 on the week

NQ, last week’s close: Settled at 21,789.50, up 207.25 on Friday and 412.75 on the week

E-mini S&P futures finished Friday at the highest level since the month-end rip on February 28th, which was 6019.50. The E-mini NQ closed at its highest since February 21st, the day that sparked the rollover. On Friday, the Nonfarm Payrolls report was solid. Job growth came in better than expected for May at 139k versus 126k, but the prior two months were revised lower by 30k. Wage Growth was the strongest component, coming in at +0.4% m/m, the highest since January, versus +0.3% expected, and +3.9% y/y, versus +3.7%. The odds of a cut at the Fed’s July meeting have all but become priced away, now at 14.5% versus 23.9% one week ago. The Federal Reserve is in its blackout period, ahead of next week’s meeting. Although a rate cut is not expected, we will get the quarterly update of the bank’s Summary of Economic Projections. This will all be front in center as Wednesday’s CPI report quickly approaches.

Friday morning, we noted the shallow end of our upside targets, rare major four-star resistance, in both the E-mini S&P and E-mini NQ were tested. While there was a more significant test in the E-mini S&P on the opening bell range that was rejected Friday morning, the E-mini NQ traded to a lower high Friday than Thursday. Although the tape is firm this morning, we are on the lookout for some near-term exhaustion. If a reversal takes place, we maintain the supports highlighted here Friday, “Despite the weak tape late yesterday (Thursday), trading to a low of 5928.75, we are not going to adjust major three-star support in the E-mini S&P and still see 5938.25-5943.50 as a significant line of defense, with additional levels listed below. We also maintain that tech can be the leader here and this way will be paved as long as price action holds above major three-star support in the E-mini NQ at 21,509-21,545.” That said, we will be watching our Pivot and point of balance through the opening hour, and continued price action above here at…

Enjoyed the report? Unlock full technical breakdowns and our daily take on crude, metals, livestock, grains, and equities—sign up through the portal today and don’t miss a move.

—

Originally Posted on June 9, 2025

Futures trading involves substantial risk of loss and may not be suitable for all investors. Trading advice is based on information taken from trade and statistical services and other sources Blue Line Futures, LLC believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. All trading decisions will be made by the account holder. Past performance is not necessarily indicative of future results. The information contained within is not to be construed as a recommendation of any investment product or service.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Blue Line Futures and is being posted with its permission. The views expressed in this material are solely those of the author and/or Blue Line Futures and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!