- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 17, 2026 at 1:15 pm

In a normal week, tomorrow would be a market highlight. The combination of a PPI report in the morning and an FOMC meeting in the afternoon should have investors anticipating a pair of potentially market-moving events. Instead, both seem like afterthoughts amidst an ever-changing global scenario. Nonetheless, both can offer important insights into the state of the economy, and hence impact market psychology, even if the risks might be one-tailed.

First up tomorrow is the PPI report. Consensus expectations for the headline, core, and ex-food, energy and trade all show rises of 0.3% in February on a month-over-month basis. That would put the first two below last month’s readings of 0.5% and 0.8%, while the third would match January’s level. Even at 0.3%, all would annualize, whether on a one-, three-, or four-month basis, to an inflation reading well above the Fed’s 2% target, but a bunch of as-expected reports would show inflation moving in the desired direction.

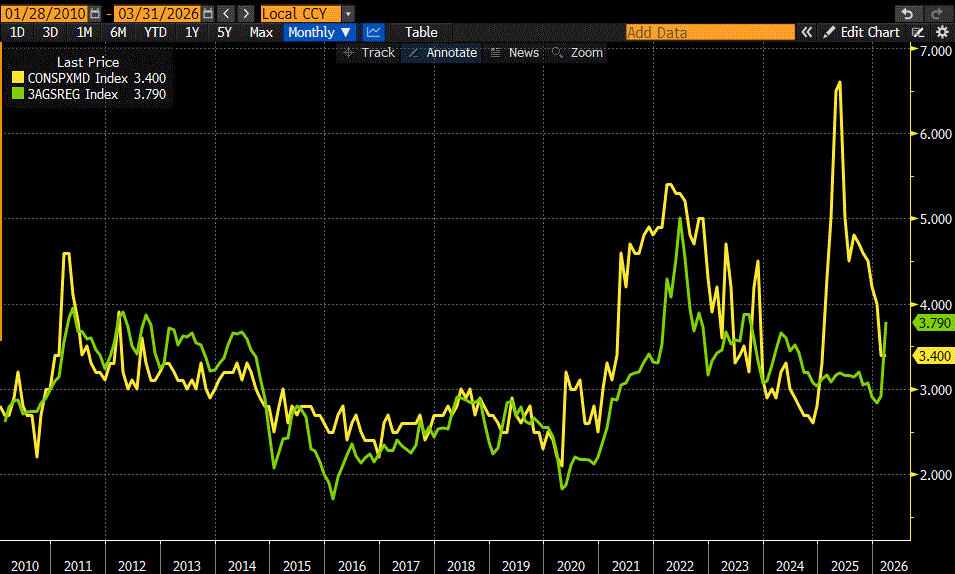

Yet even if the reports come in as expected, or even better, would that meaningfully change the FOMC’s outlook on the prospects for future inflation? Presumably not. A data-dependent central banker would be remiss to fixate on backwards looking data when there is a clear risk of higher energy prices creating price pressures throughout the economy. Sure, we know that inflation measures that exclude volatile food and energy components from the mix are considered preferable, but a sustained boost to energy prices spills into other prices and inflationary expectations. All manners of products use oil-related products for their manufacture and/or shipping, and there has historically been a close relationship between gasoline prices and 1-Year University of Michigan Consumer Inflation Expectations. As the chart below shows, that relationship broke last year as consumers feared the effects of tariffs, but it had finally returned to relative normalcy. It would be naïve to think that the sharp jump in prices at the pump will show no impact upon inflation expectations when the next Michigan data arrives on March 27th.

Since 2010, UMich 1-Year Inflation Expectations (yellow), National Average Regular Unleaded Gasoline Prices (green)

Source: Bloomberg

That points out the one-tailed nature of tomorrow’s PPI report. A better-than-expected report might be easily dismissed as poorly reflecting current conditions. Meanwhile, a worse-than-expected report could cause investors to think, “If it was this bad before the Iran situation, how much worse will it be afterwards?”

Something similar is in effect for the FOMC. Fed Funds futures and prediction markets agree in assigning virtually no probability to a rate change after tomorrow’s meeting. A lame duck Chair and a lack of economic clarity make that a very safe assumption. Although those sources now price in at least one rate cut by December, as recently as last week they were anticipating a cut no earlier than the first or second quarter of 2027. Some of the uncertainty may have cleared up on Friday afternoon after a Federal Judge quashed grand jury subpoenas of the Fed and Chair Powell. A cessation of that legal activity would allow NC Senator Tillis to remove his threatened hold on the nomination of Kevin Warsh, but yesterday’s Justice Department motion for reconsideration could further delay the process.

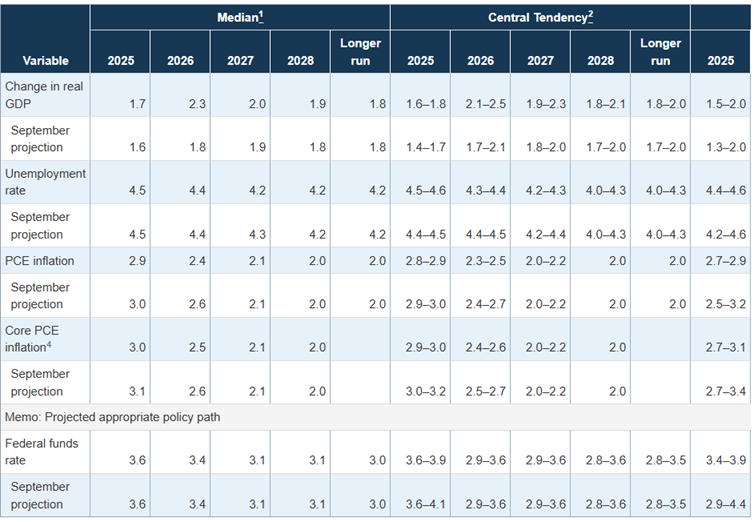

Instead, investors are likely to pay their closest attention to the Summary of Economic Projections, aka “Dot Plot”, that is due for release tomorrow. December’s SEP showed a median expectation for a 3.4% Fed Funds rate at the end of 2026, implying two cuts during the year. Bearing in mind that until very recently markets had consistently been more aggressive in predicting cuts than the FOMC, it will be fascinating to see if the FOMC members now match market expectations for fewer cuts. It will also be useful to note if the committee foresees changes in their GDP, inflation, and Unemployment Rate projections. Unlike with PPI, this could spur a move in either direction; the FOMC meeting could surprise positively if the Fed reaffirms the notion of cuts in 2026.

December Summary of Economic Projections

Source: Federal Reserve

Source: Interactive Brokers

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

How could the markets possibly go lower? Sell rallies.

Answer: the markets won’t go lower until they actually do go lower. Until then, it isn’t actually happening, so why would anyone sell until then? When it does happen, and good selling prices are hard to find, I’ll race you to the exits. Sell rallies.