- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 19, 2026 at 1:15 pm

As I type this, major stock indices are well off their opening lows. They’re not higher, at least not yet, but the S&P 500 (SPX) has recovered about half its early losses by 11AM EDT. The initial losses had notably overt causes – a solid break below SPX’s 200-day moving average, higher rates thanks to uncooperative central banks, and higher energy prices stemming from a widening of the hostilities in the Persian Gulf. Once again, though, we saw bids return to equities once the bad news began to abate.

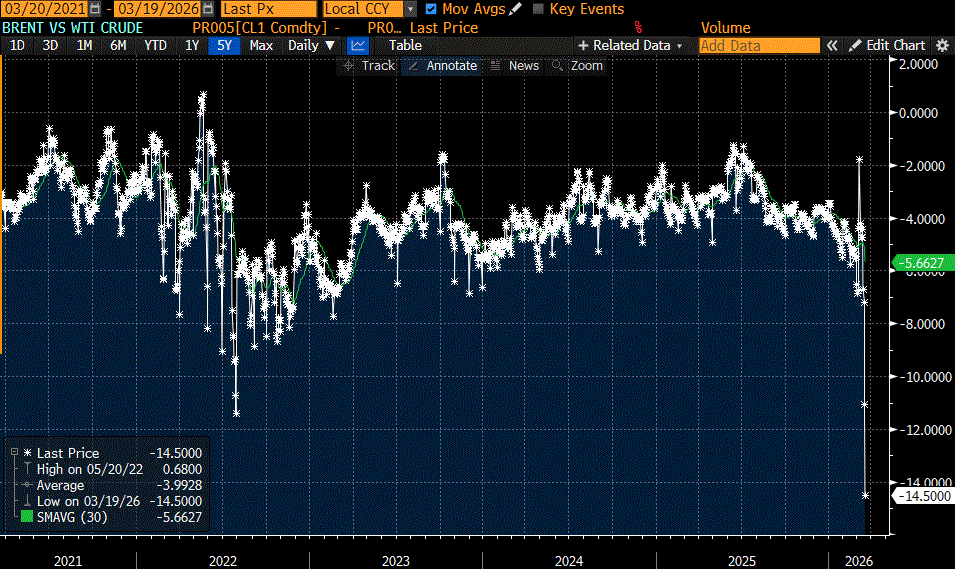

While those of us in North America were rubbing the sleep from our eyes, European investors had plenty of reasons for gloom. Brent crude futures spiked higher after Iran attacked Qatar’s Ras Laffan energy complex. WTI futures barely budged, however, which meant that the spread between the two contracts, which we highlighted yesterday as being near multi-year highs, widened even further.

Source: Bloomberg

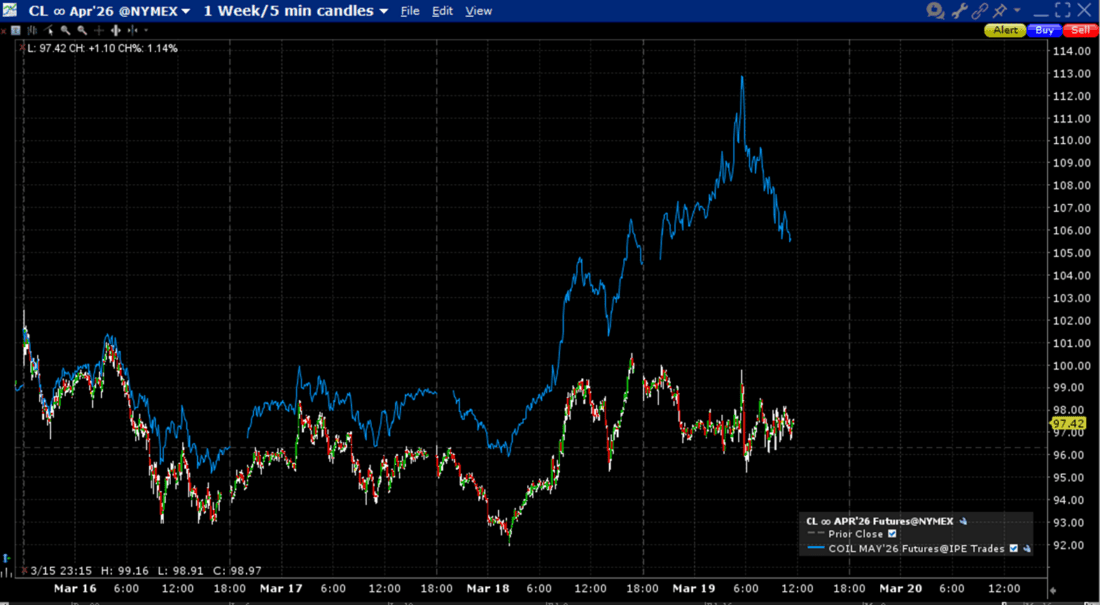

Yet as the morning wore on, Brent futures came well off their early highs:

Source: Interactive Brokers

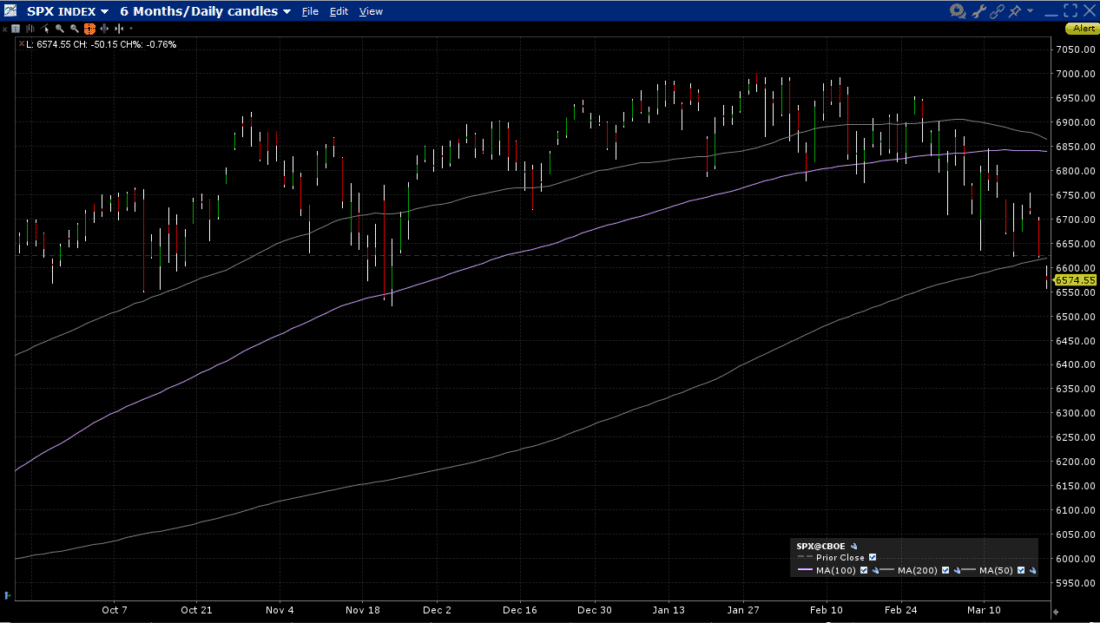

Meanwhile, stocks ended yesterday in a relatively tenuous technical situation, thanks to a poorly received post-FOMC press conference from Chair Powell. “Goldilocks in a Suit” was nowhere to be found. A late bout of selling left SPX perched on its 200-day moving average around 6620, a level that was nearly tested late Friday and held as we bounced on Monday and Tuesday. Today, we broke through during the pre-market and have yet to retest it during the regular session. While we have remained above the November low of 6522 so far today, the technical picture has weakened considerably. The 50-day moving average, which acted as trendline support late last year and early this year, has turned decidedly lower; the 100-day moving average, which acted as recent support and then resistance, has just begun a downturn of its own. The series of lower highs and lower lows since late February indicates that selling rallies has been more profitable than buying dips recently.

SPX Index, 6-Month Daily Candles with 50-day (top line), 100-day (middle line), 200-day (bottom line) Moving Average

6

Source: Interactive Brokers

Last week, we noted that rate cut expectations for 2026 had become rather uncertain. By Tuesday, Fed Funds futures were once again pricing in a December rate cut. Maybe it was a bit of St. Patrick’s Day enthusiasm, but Powell’s comments caused them to shrink once again. By the end of yesterday’s trading, there was less than a 60% chance of a cut, and those have all but evaporated this morning. Both the ForecastEx prediction market and CME FedWatch now show a roughly 17% probability for a cut this year. The Summary of Economic Projections, (aka “SEP” or “dot plot”) continued to imply a median estimate of one rate cut this year, but more “dots” moved toward no change than before. Traders were also taken by surprise when only one member of the FOMC – the ever-reliable Dr. Miran – dissented against holding rates steady. Governor Waller, who had previously advocated for lower rates, joined the majority and presumably was one of the raised dots.

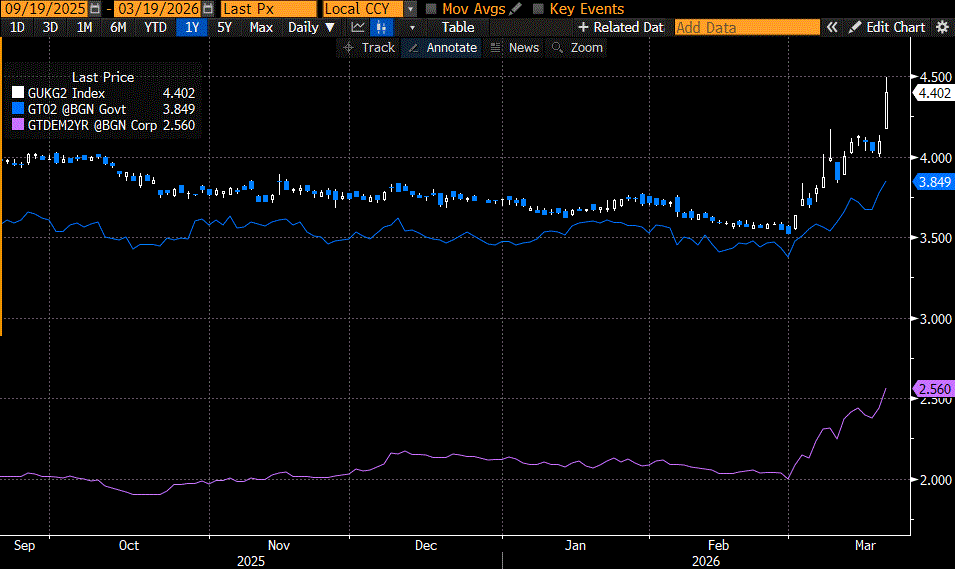

If Powell and the FOMC added a bit of murk to short-term rate forecasts, this morning’s rate decisions from the Bank of England (BOE) and European Central Bank (ECB) added a bit of unpleasant clarity. Both issued hawkish statements and commentary, raising concerns about rate hikes to combat inflation amidst rising energy prices. Note the sharp rises in 2-year rates over the past month – and especially today – in the US, Germany, and especially the UK in the chart below:

6-Month Chart of 2-Year Benchmark Yields in the UK (white/blue candles), US (blue line), Germany (purple line)

Source: Bloomberg

Against the backdrop of a technical breakdown in stocks (though above another support level), a jump in crude prices (which are off their intraday highs), and sharply higher global short-term rates (though worse abroad than in the US), we can once again say that the reaction in US stocks certainly “could be worse.”

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

As I write this amongst all the naysaying, market is barely negative( Russell positive).

Many forget a Fed board of 12 makes rate decisions. The tone of the messenger becomes far too emphasized given this reality. Goldilocks in a suit appears in a bad mood and the market participants give the messenger far too much weight, IMO.

When I first started using options, in the early ‘80’s. I had to take note of the brokerage costs, e.g. commissions, wide spreads, when I was taking all the risk, it bothered me to be sharing such a big percentage of the potential profit with the broker. It began to be clear to me that it wasn’t worth entering a trade where the potential profit was 5-7% if it only netted half of that after costs and taxes. There are some who will make such trades in the hope that they can do enough of them for the effort to be meaningful. At that time I had another fulltime job and the effort to manage that many trades wasn’t feasible. Plus the speed that the market moved these positions required more attention them I could provide;, it was better for me to look for larger and longer moves where the potential for gain was 12-20%. I called this my “cost of getting out of bed in the morning”. Granted this will differ from trader to trader (or investor to investor.) If you don’t understand what your personal cost of getting out of bed in the morning is, you will find yourself sitting with positions wondering why you got in them in the first place. Recently market has been quite erratic, but the actual amount of movement has been quite small. If you wish to try your hand making a living trading a few points up and down in the present market, sobeit. But for me I rather hold MU over the last year and a half, than play its daily up and down.