- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 18, 2026 at 1:00 pm

Rotation between stock market sectors has been a key topic of conversation this year. Investors are clearly changing their allocations, sometimes rather violently. Broadly speaking, the shifting sectoral preferences have been a boon to value investors but came at the expense of investors who favor growth stocks. Unfortunately, one of the first pieces of investing advice that I received is echoing through my mind: “Be careful when energy stocks lead the way.”

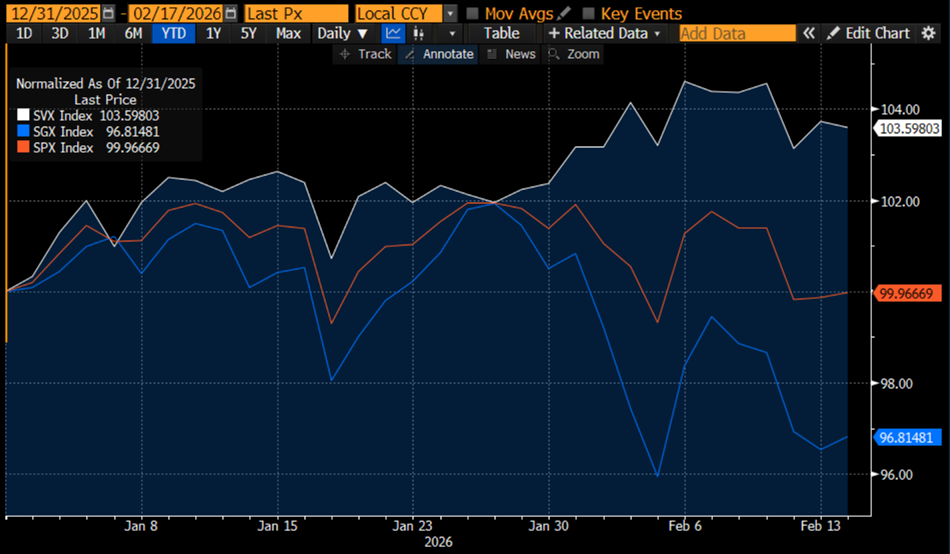

While I have long thought that the distinction between growth and value stocks can be arbitrary, the arbitrary distinction is necessary for comparison purposes. We can see that so far this year, the S&P 500 Value Index (SVX) has substantially outperformed its counterpart, the S&P 500 Growth Index (SGX). On a year-to-date basis through yesterday, while the S&P 500 Index (SPX) was almost exactly unchanged, SVX was up about 3.5% while SGX was down by a similar amount. This is the inverse of what occurred in 2025, when SGX outperformed SPX by about 5% but SVX underperformed SPX by a slightly larger margin.

Source: Bloomberg

Source: Bloomberg

The outperformance of growth over value has been a theme since the current bull market began in November 2022. We can see from the chart below that the recent resurgence of value vis-à-vis growth is just a blip on their relative performances since that time:

Source: Bloomberg

You might rightly think, “OK, so value is having a moment. Big deal, every dog has its day.” I could come up with several more dismissive clichés, but you should get the point. It’s entirely natural, and in fact desirable, for investors to seek out unloved stocks and sectors rather than continuing to chase winners in perpetuity. The problem occurs when we dig deeper into which sectors are leading the way.

Source: Bloomberg

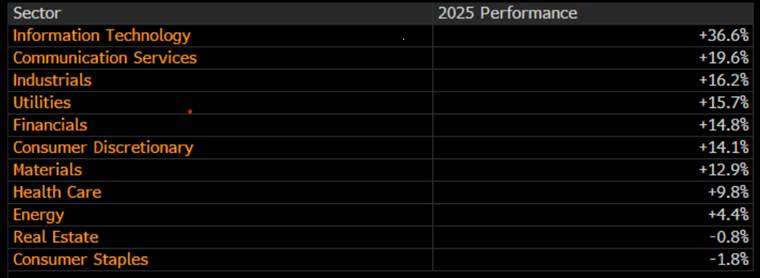

Indeed, we are being led by Materials, followed closely by Energy. That is terrific if you’ve been invested in those sectors. It is far less terrific if you are concerned about inflation. Rising prices of energy and materials create inflationary pressures throughout the economy, even if energy prices are not factored into measures of core inflation.

That was the root of the admonition that I received early in my career. Sectors that benefit from rising commodity prices indicate either that prices in the economy are moving substantially higher or that investors are hedging concerns about incipient inflation later. Since inflation measures are generally not racing ahead, the latter factor is likely the case – especially with longer-dated Treasuries showing strength this month.

The underlying reasons for the recent rallies in those sectors should be somewhat apparent to engaged investors. We have all witnessed, if not participated in, the stunning rally in precious metals, but that is far from the whole picture. The rush to build and power AI-related data centers will require infrastructure and energy buildouts. Commodity metals like copper and aluminum are certainly required. Although energy prices have been relatively contained in recent months, concerns about Iran-related saber-rattling and weather-driven spikes in natural gas and heating oil have returned energy stocks to the forefront of many investors’ minds.

Does this mean imminent danger for the stock market? Far from it. Might it mean that investors are getting squirrely about the types of factors that could impede economic progress in the intermediate term? Yes. Even today, when stocks are rallying sharply off their test of the lower end of their recent trading range, Energy is only trailing Technology by a modest amount thanks to a $2.50 pop in March WTI futures. Concerns abound, but they are not of the immediate variety amidst the current news flow.

Source: Bloomberg

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!