- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 27, 2026 at 12:58 pm

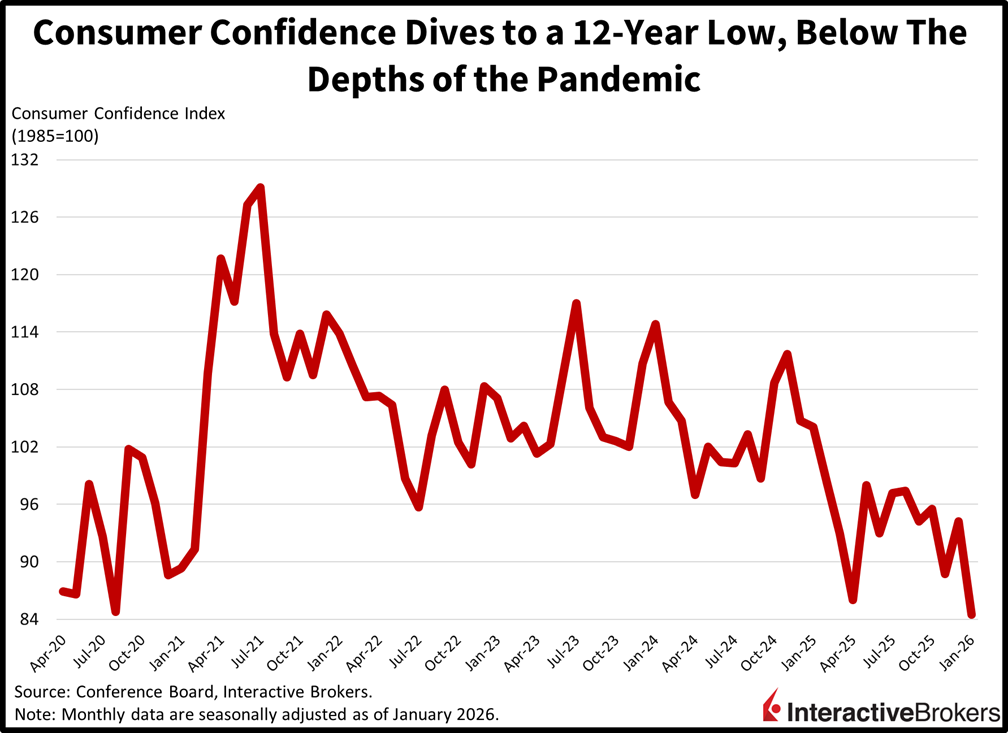

The S&P 500 jumped to a fresh record this morning as tech gains countered sharp 20% declines in UnitedHealth and Humana. Those selloffs were sparked by Washington considering providing no annual rate change in outlays to private Medicare insurers that were expecting a bump to generate revenue expansions. The 0.09% planned raise for 2027 was well below both the average and expectations as high as 6%. The proposal would likely compress margins in an industry that has been managing higher patient expenses amidst federal payments that firms say were already insufficient. The dynamic has equities trading in bifurcated fashion in what could have otherwise been a broad rally, with the Dow and Russell retreating notably while the S&P 500 and Nasdaq 100 appreciate substantially. But the weakest consumer confidence print in 12 years is also denting the cyclical areas of the market despite ADP’s weekly jobs numbers hanging in there. In fixed-income, currency and commodities, Treasuries are near their flatlines although duration is taking modest losses, the greenback is getting slammed, marking a four-year low, and silver, gold and crude are advancing as natural gas, lumber and copper descend. Risk-on mindsets on Wall Street have investors unwinding hedges as volatility protection instrument premiums drop while strong animal spirits drive interest in cryptocurrencies and prediction markets.

Consumer Confidence plunged to the worst level in over a decade with households feeling worse about economic prospects than even during the pandemic. The Conference Board’s 84.5 headline score for January was well below the 90.9 median estimate and the 94.2 from December. Gauges for both the present and for future expectations declined from 123.6 and 74.6 to 113.7 and 65.1. Outlooks for business, income and employment all weakened substantially as survey respondents referenced inflation, tariffs, job opportunities, healthcare and geopolitics as headwinds.

Non-government payrolls increased by an average of 7,750 workers in each of the four weeks during the period ended Jan. 3, according to ADP. The result is a modest deceleration from the 8k seven-day average expansion for the interval culminating on Dec. 27, but recent figures continue to point to a solid labor market.

Investors are looking for tech earnings to drive the next leg of this bull market with equities reaching fresh records prior to the quarterly reports even being published. The risk-on attitude on Wall Street amidst a lack of hesitation to lift exposures is emblematic of participants believing that the prints will deliver beats and raises overall while pointing to an extended runway ahead for AI that could continue bolstering economic performance and asset prices. Meanwhile, tomorrow’s Fed decision is likely to be a non-event for stocks, since a pause is expected and no cut is projected by the funds curve until June, after Chair Powell’s term ends in May. Domestic yields and the greenback could react; however, those paths aren’t wide enough to impact the equity benchmarks significantly at this juncture, as a softer dollar is positive for the bottom lines of global corporates while Treasuries, particularly at the long-end, are set up for gains from here rather than losses in the short-run in consideration of decelerating inflation and slowly improving fiscal conditions, assuming no imminent Supreme Court verdict on tariffs.

China’s strong export volume and a government crackdown on aggressive price discounting contributed to the country’s industrial profits growing 0.6% in 2025 after three consecutive years of declines. December was also strong with profits up 5.3% year over year (y/y), ending a three-year streak of sinking results. Metal rolling processing and ferrous metal companies produced the strongest earnings followed by electronics manufacturing.

Hong Kong’s exports on a y/y basis grew at a slower pace than imports in December and the special administrative region’s monthly deficit grew from $48.5 billion in November to $63.3 billion, according to the Census and Statistics Department. Margins fell in coal mining and washing industry. Exports last month were 26.1% higher than in December 2024. The shipments abroad accelerated from the 18.8% y/y jump in November. Import expansion, meanwhile, sped up from 18.1% in November to 30.6%.

The following countries or regions and the growth of their purchases of Hong Kong goods experienced the largest increases:

The following countries and the extent of the growth of their shipments to Hong Kong experienced the biggest gains in exports to the special administrative region:

Among products shipped to other countries, the biggest gains occurred within electrical equipment, machinery and mechanical appliances.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!