- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 23, 2026 at 1:08 pm

The ongoing frenzy in semiconductors paired with better-than-expected PMI data intraday lifted the S&P 500 and Nasdaq indices briefly from the red and to fresh records even as tensions escalated in the Middle East. Investors have persistently looked past hostilities along the Strait of Hormuz this month, although risks of a significant energy supply shortage are rising with the US and Iran continuing to pose threats to vessels attempting use the important trade route. Emblematic of the hazards is a raised geopolitical premium, reflected via WTI changing hands at almost $97 so far this session. Meanwhile, strong bids in chipmakers and AI-related names are being supported by the notion that these firms won’t be as impacted by disruptions to the real economy, as their business models are increasingly insulated to cyclical developments. Just 4 of the 11 sectors in equities are appreciating against this backdrop, and volatility protection instruments are hanging in there as traders add hedges to their books. Elsewhere on Wall Street, rates, the greenback and cryptocurrencies are nearly unchanged, and prediction markets are experiencing engagement.

Economic conditions improved slightly this month, as consumer demand, business production, employment and corporate sentiment hung in there despite supply chain disruptions and accelerating prices denting performance and the outlook. The manufacturing sector stood out, meanwhile, as proactive inventory increases motivated by the Strait of Hormuz closure and incentive measures from last year’s passage of the Big Beautiful Bill drove a beat in the S&P Global Flash Purchasing Managers’ Index (PMI), with the segment coming in at 54, ahead of the 52.5 expectation and March’s 52.3. The Services PMI fared much worse as revenue pressures attributed to Middle East uncertainty and sluggish exports weighed on transactions; it came in at 51.3, arriving higher than the 50 projection and the prior month’s 49.8 contraction.

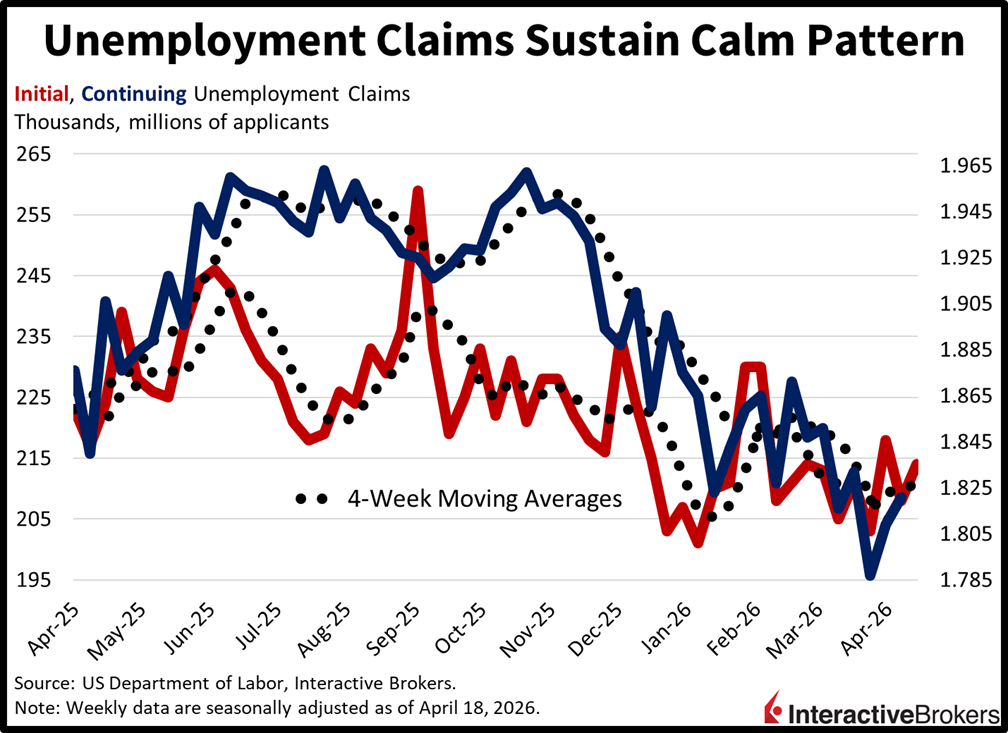

Unemployment claims are sustaining their calm pattern of recent months and providing further evidence of stable labor conditions. Initial and ongoing filings for the weeks ended April 18 and April 11 rose slightly to 214k and 1.821 million, near estimates of 212k and 1.820 million and the prior week’s 208k and 1.809 million. Four-week moving averages were also well behaved, climbing modestly to 210.75k and 1.812 million.

With West Texas Intermediate (WTI) back at $95 and roughly 51% higher than it was 12 months ago, the chances of a 4-handle Consumer Price Index (CPI) this summer are rising fast as the struggle along the Strait of Hormuz continues. Markets are underpricing this risk, which would likely converge right around the time the new Fed Chair Kevin Warsh is confirmed. Treasurys are poised to test the head of the central bank as a result of accelerating cost pressures that are significantly above the institution’s 2% objective, with the 2- and 10-year yields meaningfully below my assessment of fair values, which are 30 basis points heavier at 4.10% and 4.60%, leading to a mid-year correction in stocks just as the heat of election season arrives. Equities are not only vulnerable to the potential of climbing inflation and tighter financial conditions, but ever more so to the shocks that a prolonged energy supply shortage would cause across the global economy amidst an associated destruction in demand.

South Korea rode the wave of growing demand for artificial intelligence products in the first quarter with sales of computer chips pushing the country’s gross domestic product growth to 3.6% year over year (y/y) and 1.7% quarter over quarter (q/q). Both metrics accelerated considerably from the 1.6% y/y and negative 0.2% q/q results in the preceding quarter and jumped past the economist consensus y/y and q/q estimates of 2.7% and 1%. The q/q pace was the fastest since the third quarter of 2020, which recorded a 2.2% advance. In the recent quarter, semiconductor manufacturers increased their investments in production facilities by 4.8% q/q. In other areas, construction outlays, private consumption and government consumption climbed 2.8%, 0.5% and 0.1%, respectively.

The South Korea Consumer Confidence Index sank 7.8 points in April to 99.2, dropping below 100 pessimism/confidence threshold for the first time in 12 months, according to the Bank of Korea. The decline followed the 5.1-point retreat in February. Consumers’ views of current economic conditions and their economic outlook sank 18 and 10 points to 68 and 79. Meanwhile, headline inflation expectations for the coming 12 months hit 2.9%, up 0.2 percentage points from March.

Singapore’s CPI depicted costs climbing 1.8% y/y and 0.5% m/m in March, with the annual pace intensifying from 1.2% in February. The m/m pace eased marginally from the preceding month’s 0.6% rate. The Core CPI, which excludes items with volatile prices, also depicted stronger inflation with a 1.7% y/y print, up 0.30 percentage points from February.

For the headline annual result, higher stickers for oil pushed transportation costs up 6%. Other groups with the most significant y/y increases and the extent of the changes included the following:

• The health category, 6%

• Recreation, sport and culture, 1.7%

• Food, 1.6%

• Miscellaneous goods and services, 1.5%

Higher energy costs also pushed the transport category up 2.9% m/m while clothing and footwear became 1.5% more expensive.

Prices in Hong Kong last month were stagnant relative to February and experienced no change in the rate of inflation y/y. Indeed, the March CPI was flat m/m, easing from the 0.5% ascent in February, and it was up 1.7% y/y, matching the preceding month’s ascent rate. Economists anticipated a 1.8% y/y result.

The m/m level was the lowest since June, which also produced a goose egg result. For the y/y print, the following items and the extent of their sticker growth contributed to the headline:

• Miscellaneous services, 4.6%

• Transport, 3.9%

• Electricity, gas and water, 3.9%

• Miscellaneous goods, 2.8%

• Alcoholic drinks and tobacco, 2.1%

• Basic food, 1.2%

• Housing, 1.0%

• Meals out and takeaway food, 0.8%

Conversely, durable goods and the category consisting of clothing and footwear were the only areas to experience declines with 2.2% and 0.7% descents.

Europe slipped from slow growth to contraction this month with the S&P Global Flash Eurozone PMI Composite Output Index sinking from 50.7 in March to 48.6, a 17-month low and weaker than the economist consensus estimate of 50.2. The services industry was the culprit with its corresponding PMI gauge descending from 50.2 to 47.4, marking a 62-month low and missing the 49.8 result expected by economists. Conversely, the broader Manufacturing PMI and the Manufacturing Output Index both reached 52.2 following March’s 51.6 and 52 levels. Manufacturing activity picked up as businesses added inventory in anticipation of supply chain obstacles caused by the Middle East war, a conflict which also sparked higher input and output prices.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!