- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 28, 2026 at 1:07 pm

Wall Street is poised for meaningful losses today in response to rising doubts about a quick reopening of the Strait of Hormuz paired with subdued tech enthusiasm subsequent to a WSJ report of OpenAI missing internal revenue targets. The bearish one-two punch is lifting WTI crude oil north of $100, while raising inflation expectations and interest rates as a result. Simultaneously, the semi and mag7 trades are getting battered on pessimism regarding the return prospects of massive capital expenditures at a critical time—5 of the 7 firms are set to deliver earnings tomorrow and Thursday. The risk-off sentiment is further justified by a fed funds complex that for the first time in roughly a month is pricing in a 4% chance of a hike this January and fixed-income observers are impatiently awaiting this Wednesday’s monetary decision and Powell presser to gauge the committee’s appetite for a potential increase in borrowing costs as well as whether the current chair will continue as governor after nominee Kevin Warsh is confirmed. A hawkish tilt is certainly warranted, especially following this morning’s weekly ADP-employment print reflecting strength alongside higher-than-expected consumer confidence tied to better labor conditions. Furthermore, in my view, the CPI is geared to accelerate to 3.7% in April and reach a level between 3.8% to 4.1% in May, pushing the US central bank to join its G7 peers in planning for increases, like Japan did yesterday. On the trading floor, the yield curve is ascending in bear-flattening fashion led by the policy sensitive shorter tenors, all equity benchmarks are sinking along with cryptocurrencies in light of cautious investor positioning although 6 of the 11 sectors are advancing. Elsewhere, the greenback is appreciating, volatility protection instruments and prediction markets are catching bids, but non-energy commodities are facing selling pressure.

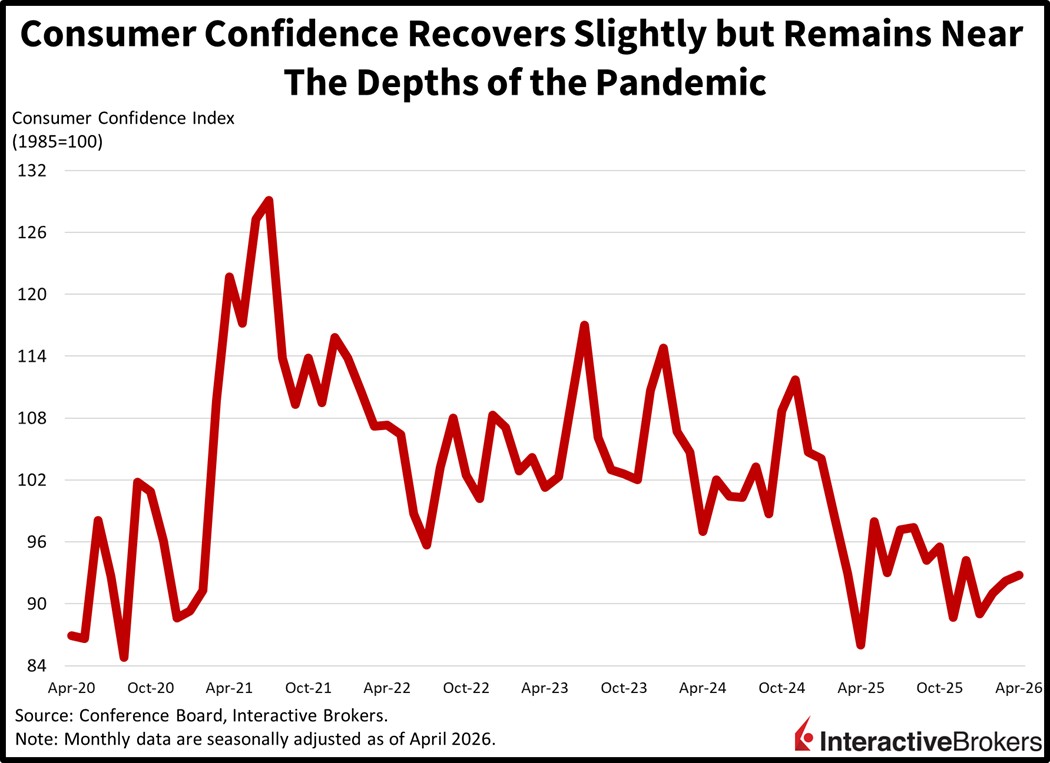

Improving views of the labor market drove a modest increase in consumer confidence even though the indicator remains near pandemic depths. Still, elevated prices, pain at the pump, the Iran war and heavy interest rates were significant headwinds, contributing to a subdued April headline number of 92.8; however, the figure surpassed the median estimate of 89 and March’s 92.2. The present and expectations sub-indices shifted in bifurcated fashion from 124.1 and 71 to 123.8 and 72.2, as the road ahead looked better than current conditions. Household spending plans were indeed weaker, as big-ticket buying and discretionary services intentions softened in response to economic uncertainty and rising projections of recession in the next 12 months.

Private sector hiring decelerated slightly at the beginning of this month but remained much stronger than at the start of the year. Payrolls jumped by an average of 39.25k employees in each of the four weeks during the period that ended April 11, lighter than the 40.25k print from the prior publication, according to ADP. Despite the slower increase, the report points to monthly gains of around 170k, which is quite robust.

Last night’s Bank of Japan meeting featured a highly contested hold, as 3 of the 9 voting officials preferred to hike in consideration of significant inflation risks looming. The huge surprise has fixed-income observers heavily favoring an increase at its June gathering, as monetary policy documents pointed to the institution raising borrowing costs in response to subdued real rates and speedier price pressures, especially as it pertains to wage forces. In light of the hawkish turn and a lack of resolution in the Middle East, international duration is getting creamed as investors consider the restart of tightening cycles across most of the G7 nations. Meanwhile, tomorrow will offer clues as to where the US stands after a convention last month included several committee members opining that the next change in fed funds should be a lift, not a reduction. The development is noteworthy with cost gauges accelerating towards a 4-handle just as nominee Kevin Warsh is set to be confirmed in the coming weeks. Finally, another key focus will be whether Chair Powell stays on as governor, as his voice can influence a tougher posture amongst the group, which is under close watch by President Trump.

Bank of Japan (BoJ) inflation hawks tried to raise the organization’s key rate 25 bps to 1% with policymakers voting 6-3 to maintain the current level, a decision that was widely expected by economists. The BoJ also lowered its outlook for 2026 gross domestic product (GDP) growth from 1% to 0.5% while boosting its core inflation forecast from 1.9% to 2.8%. In the fourth quarter, the country’s economy expanded by 0.3% quarter over quarter and 1.3% year over year (y/y) and last month, the core Consumer Price Index depicted costs climbing 1.8% y/y, an acceleration from 1.6% in February. During the meeting, proponents of tighter monetary policy maintained that the US-Iran war has increased price pressure risks. The upward revision to inflation, furthermore, is higher than the bank’s 2% target. At the same time, the BoJ believes the conflict will cause a deterioration of trade, weaker corporate profits and a further decline in real household incomes, which will hinder GDP expansion.

Japan’s unemployment rate climbed from 2.6% in February to 2.7% last month, exceeding the economist consensus estimate of 2.6%, according to the country’s Statistics Bureau. Also in March, the country had a job opening to job applicant ratio of 1.18, pointing to a marginally tighter labor market than in the preceding month, which had a 1.19 ratio. Regarding the unemployment rate, the country’s payroll total of 67.73 million expanded by 30,000 relative to March 2025 while the number of unemployed, at 1.94 million was 140,000 higher y/y, marking the eighth consecutive month of increases.

Hong Kong’s trade deficit widened from $64.2 billion in February to $89.1 billion last month with an acceleration in both imports and exports. It was the 13th consecutive month of the value of imports exceeding exports. Imports were 41.2% higher y/y, a strong acceleration from the 24.7% pace of expansion in April. Exports also jumped, but the 35.8% y/y increase trailed the growth of imports. In the preceding month, shipments to foreign markets climbed 24.7% y/y.

Relative to March 2025, the shipments to the following countries and the y/y extent of their changes, grew considerably:

Shipments to the UK, however, slipped 29.1%.

Also in March, imports from the UK, Korea and India were up by 118.5%, 112.2% and 88.1%. Vietnam, the US and Mainland China also experienced strong demand with the value of shipments to Hong Kong up 85.7%, 66% and 48.8%. The strongest growth in merchandise sent to foreign markets occurred with electrical machinery, apparatus and appliances, and electrical parts category, which climbed 47.9%, and telecommunications and sound recording and reproducing apparatus and equipment group, which grew 94.7%. Non-ferrous metals, with a 175.9% jump, also support export volumes. A Hong Kong spokesperson says the strong export growth was driven by demand of artificial intelligence products.

Retailers ushered in 1% y/y price increases this month, a slower pace than both the 1.4% expected by a consensus of economists and the preceding month’s 1.2% ascent, according to the British Retail Consortium (BRC) Shop Price Index. The result sank below the three-month average of 1.1% and was dampened by bigger discounts for clothing, furniture and DIY products, according to BRC Chief Executive Helen Dickinson. Weakening consumer confidence during the month caused retailers to work harder to maintain spring spending levels. Looking beyond non-edibles, prices of non-food items sank 0.1% y/y following the preceding month’s gain by the same amount. Fresh food and food prices, furthermore, became 3.9% and 3.1% more costly y/y, moderating from the 4.4% and 3.4% northward movements in March. The results were also below the three-month average inflation rates of 4.2% and 3.3%.

Retail sales were below seasonal norms in April with the shortfall increasing from March’s weakness, according to the Confederation of Business Industry index. Retailers judged sales to be poor and cashier activity fell at a rapid rate year to date as of April. The results point to weak consumer confidence as households feel the economic impact of the US-Iran war, according to the organization.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

Regarding consumer confidence, we may be starting to see an improvement, particularly as New York begins to address deed theft in a more meaningful way. This is an issue my own parents have faced, and I’ve spent considerable time trying to help—reaching out to elected officials, hiring legal counsel, and even contacting the media, without much success. The recent creation of the Mayor’s Office of Deed Theft Prevention is an encouraging first step. While many families, including mine, are still waiting to see how policy will be implemented, this initiative signals progress in addressing a long-standing issue.