- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 23, 2025 at 12:49 pm

Stocks jumped to new record highs shortly after the bell before investors pared back some of their enthusiasm prior to Fed Chair Powell’s scheduled visit to the podium this afternoon. It’s been an eventful week for speakers from the central bank, with a few officials preferring a slower walk down the monetary policy stairs, opining that inflation has hovered above the institution’s target for over four years amidst uncertainty about the potential for tariff-fueled price pressures. Others, including Governors Miran and Bowman, however, believe that the current stance is far too restrictive in light of risks to the employment mandate. This morning’s economic calendar supported the doves, meanwhile, with the Flash PMI signaling softening ordering this month, which have constrained pricing power, margins and hiring. Still firms, were upbeat concerning future prospects, with expectations of lighter borrowing costs countering worries related to possible trade headwinds. Today’s equity market performance is being led by the small-cap, cyclically oriented Russell 2000 Index, which may be finally breaking out to the upside due to its heavy leverage to reaccelerating domestic conditions as well as rate cut optimism. All sectors and subcomponents are advancing minus consumer discretionary, while the entire commodity complex ex copper, bitcoin and forecast contracts catch bids. Treasuries and the greenback are nearly flat, though, and are awaiting catalysts that may come from the upcoming US government debt auctions at the belly of the curve. Offerings of $69 billion, $70 billion and $44 billion across the 2-, 5- and 7-year maturities are on deck today through Thursday.

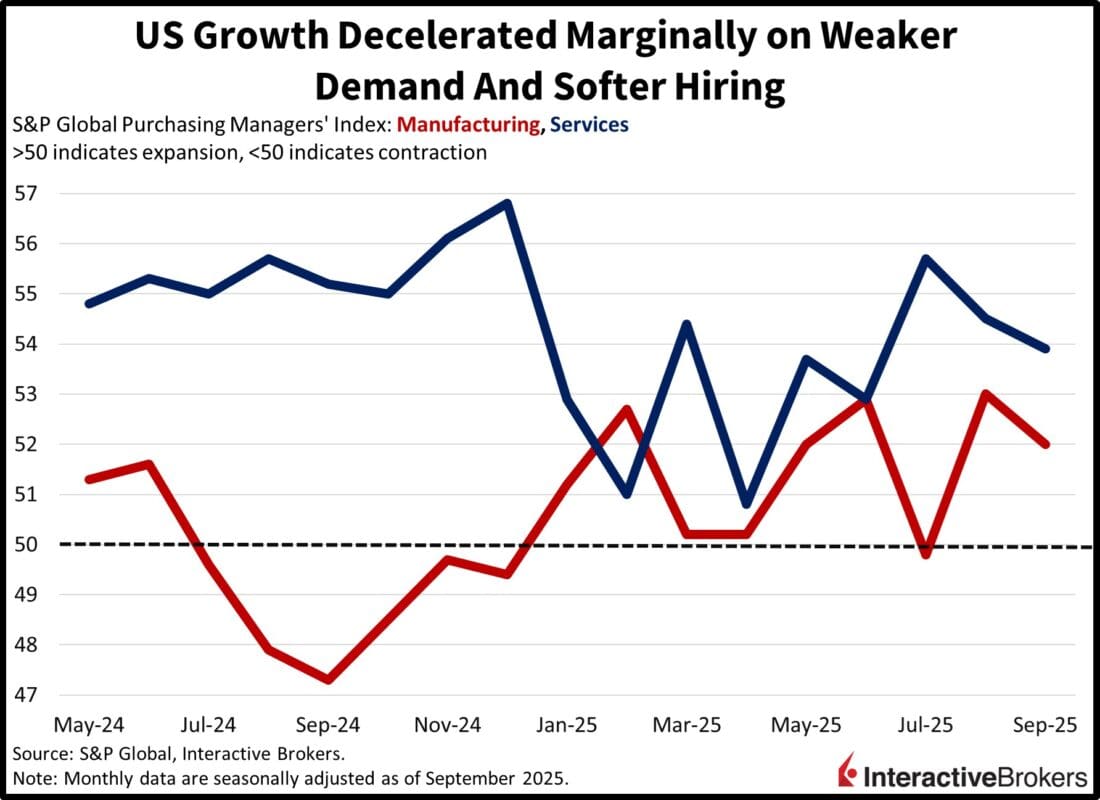

Economic activity decelerated slightly this month, according to the Flash Purchasing Managers’ Index (PMI) from S&P Global, which depicted slower momentum in the services and manufacturing sectors. The headline results fell to 53.9 and 52 from August’s 54.5 and 53, but the figures arrived near estimates and were well above the contraction-expansion threshold of 50. Both segments saw sluggish new orders amidst slimming backlogs, which caused firms to delay adding workers while struggling to pass rising input costs on to consumers in light of fierce competition and limited buyer capacity, which compressed margins.

Some companies took advantage of softening cost forces by building up inventories that they plan to sell at a later date. Overall, however, the outlook for the road ahead improved, as prospects of easier financial conditions offset worries related to general uncertainty and tariffs. Manufacturers, in particular, were enthusiastic about onshoring, domestic investment and future production levels.

Today’s data from S&P Global was friendly on the inflation front amidst an expansion that still has legs, which is music to the ears of stock bulls that crave corporate earnings growth. Meanwhile, the softening price forces are conducive to lighter interest rates, which are critical to supporting heavy valuation multiples. But the Flash PMI numbers are early and can be volatile, so investors will be awaiting more statistics in the coming days to assess the economic cycle’s momentum. For now, however, the second-half reacceleration theme remains intact, although unemployment vulnerabilities are front and center, especially following a downwardly revised June that featured 13k jobs lost. It was the first month of an overall payroll reduction in around four and a half years, since December 2020. In light of significant risks of continued job market weakness, the Fed should have a firmer commitment to a looser stance and forget about cost pressures for just a few months while employment conditions strengthen.

The eurozone manufacturing sector slipped into contraction this month but the services industry pushed the HCOB Flash Eurozone Composite PMI Output Index to a 16-month high of 51.2, up from 51 in July. The HCOB Flash Eurozone Manufacturing PMI component was a major headwind, sinking from 50.7 to 49.5, a three-month low and below the contraction-expansion threshold of 50. In a similar change, the manufacturing output component weakened from 52.5 to 50.7, a two-month low. While factories cranked out more items, new orders were unchanged from August, weighing on the PMI. Conversely, the services PMI strengthened from 50.5 to 51.4, a nine-month high, causing overall output growth for the composite measurement to hit its fastest pace since May 2024.

Despite the strong services result, hiring within the industry slowed while the manufacturing sector continued to eliminate positions, resulting in a flat month for payrolls. The composite PMI also depicted easing input cost inflation and descending sales prices with the latter development driven by the manufacturing industry, which also accounted for weakening business sentiment.

The UK’s manufacturing sector is continuing to contract— its flash September PMI sank from August’s 47 print to 46.2, a five-month low. Similarly, the industry’s output gauge dropped from 49.3 to 45.4, the worst result in nine months. In another discouraging development, the S&P Flash UK Services PMI Business Index, while staying in expansion with a score of 51.9, hit a two-month low following its August print of 54.2. The sector, however, was strong enough to keep the flash UK PMI Composite Output Index in expansion with a score of 51. Nevertheless, it was the lowest composite level in four months. With rising costs and subdued demand from slumping overseas trade putting pressure on margins, employers trimmed payrolls, but business activity expectations for the coming 12 months remained positive, albeit at a three-month low. Weak client confidence combined with uncertainty regarding politics and the economy weighed on sentiment.

While inflation has trended above of the Bank of England’s 2% target, the central bank last month slashed its key interest rate from 4.25% to 4% in response to job market weakness. Today’s PMI report, including the depiction of easing input price increase, could provide fodder for BoE policymakers who want the organization to continue its easing cycle.

South Korea wholesale prices, as measured by the preliminary Producer Price Index (PPI), were down 0.1% m/m but climbed 0.6% y/y following July’s positive readings of 0.4% and 0.5%, according to the Bank of Korea. Among broad classifications, the agricultural, forestry and marine products group was 3.4% higher m/m. Heat waves hindered farming while demand grew, supporting price pressures. At the same time, prices were stable for the manufacturing products segment and the electric power, gas, water and waste category, but they descended 0.4% for the services sector.

The m/m discount that Singapore shoppers enjoyed in July reversed in August with the Consumer Price Index up 0.5% after sinking 0.4% in the preceding print. Price pressures on a y/y basis eased, however, climbing 0.5% compared to the economist consensus estimate for a repeat of July’s 0.6% result. The core y/y index, which excludes items with more volatile prices, reflected a similar change as the headline, climbing 0.3%, a slower pace than both the economist consensus estimate of 0.4% and July’s 0.5%.

With the m/m headline, the housing and utilities component cost consumers 1.6% more with the accommodation component driving the northward movement. Other economic areas that became more expensive and the amount of their changes included the following:

Miscellaneous goods and services were unchanged while the recreation, sport and culture classification and the household durable and services area sank 0.3% and 0.2%, respectively.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!