- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 24, 2026 at 12:27 pm

The lack of Middle East peace is reversing some of yesterday’s bullish market progress that was ignited by President Trump signaling productive discussions with Tehran. But Iran’s ongoing denials that communications have begun with Washington are escalating geopolitical angst, resulting in expectations for higher inflation. Crude oil and rates are indeed back on the upswing due to the uncertain conditions; however, stocks have bounced to the flatline after experiencing morning turbulence, as equity investors gear up for a potential TACO style rally, especially as they consider that the commander in chief has increasingly shifted from an apprehensive stance to his classic deal man approach. Meanwhile, the economic calendar has also reminded folks of the dangers of an extended war, with the US, EU, UK and Australia flash PMIs all reporting sharp decelerations in activity amidst a pickup in cost pressures, a harmful stagflationary development that is poised to worsen if the conflict continues. On Wall Street, the Treasury curve is ascending in bear-flattening fashion led by the monetary policy sensitive shorter tenors, generating a greenback advance as well. Sector breadth for shareholders is impressively positive though, with 8 out of 11 gaining. Healthcare, communication services and technology are the day’s laggards. Volatility protection instrument premiums remain elevated although they are lightening up modestly as participants inch closer to risk-on mode. Commodities minus lumber and copper are appreciating for the most part and cryptocurrencies are nearly flat as speculative enthusiasms are on pause for now. Forecast contracts are catching bids.

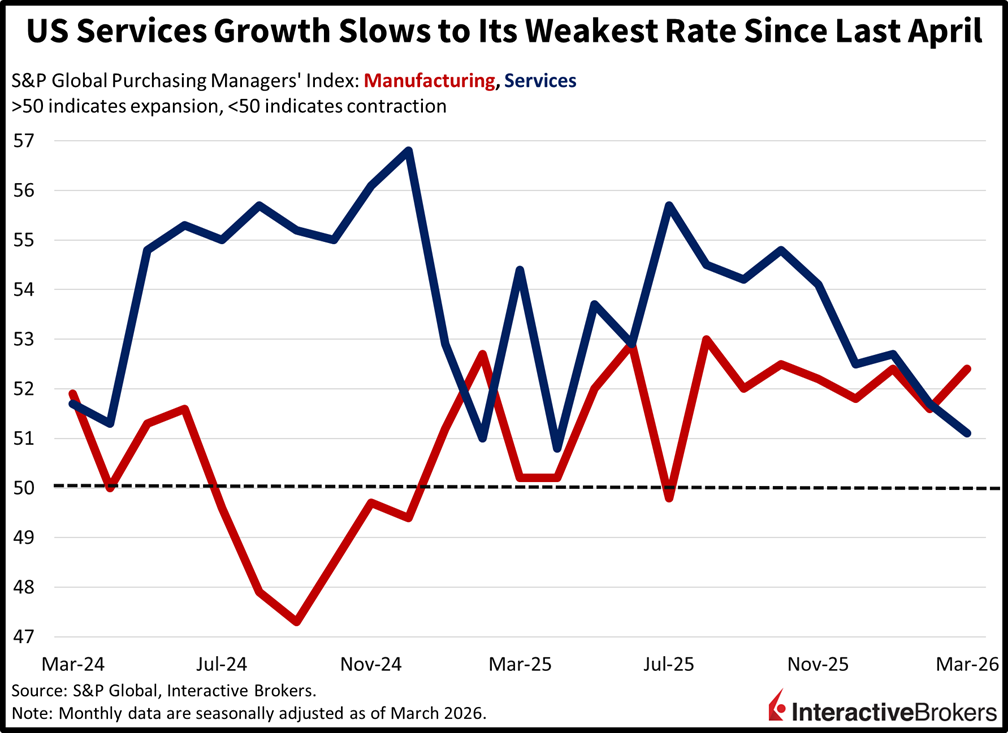

US firms are experiencing decelerating transactions amidst stronger cost pressures, according to this month’s Flash Purchasing Managers’ Indices (PMI) from S&P Global, although factory momentum progressed for the 8th consecutive period. The buoyancy continued to be driven by investment incentive measures from last year’s passage of the Big Beautiful Bill, which allows first-year 100% depreciation on capital expenditures across a wide array of projects. Services barely grew, however, dropping to an 11-month low, as contracting payrolls, slower orders, weaker exports and surging prices weighed on overall performance and confidence amongst survey respondents. General concerns included elevated interest rates, volatility on Wall Street, travel uncertainties due to the Iran war, and heavy energy costs, which led to a composite PMI score of 51.4, beneath the 51.9 reported in February. Throughout industries, manufacturing and services came in at 52.4 and 51.1, which compare to expectations of 51.3 and 51.5 and the prior interval’s 51.6 and 51.7.

Private-sector payrolls ramped up to begin this month as the slow expansion in hiring ensues. Employment increased by an average of 10k workers in each of the four weeks during the period that ended March 7, north of the 9k print from the previous report, according to ADP. Even as economic uncertainty continues, the figures still mark a modest acceleration that began in January at below 10k.

Equity investors are reflecting impatience regarding a potential ceasefire announcement from President Trump, as their behaviors stand in contrast to participants in the fixed-income and commodity markets who are proceeding with a significant amount of caution. It appears the former group is projecting a sooner end to the war than the latter bunch, as peace is needed soon to avoid a persistent surge in costs that would hurt economic performance and portfolios across the board. Absent an armistice, price pressures will jump north of 4% by this summer and derail the conditions that drove strong advances for stocks and Treasuries to begin the year. Indeed, adverse impacts to inflation expectations, corporate margins, consumer spending capacity, business investment appetites and rate cut prospects as a result of an extended conflict would materially raise slowdown angst, generate stagflationary winds and drive an even deeper selloff on Wall Street.

Overall eurozone activity weakened to a 10-month low with new orders easing and input cost climbing at a faster pace due to the Middle East war, according to the S&P Global Flash Eurozone PMI Composite Output Index. While services slowed considerably, manufacturing activity hit a 45-month high with an increase in orders breaking a 44-month period of declines. The composite benchmark consisting of both services and manufacturing segments sank from 51.9 in February to 50.5, only 0.5 points above the contraction-expansion threshold.

The following changes occurred with individual gauges:

Within the Composite Index, input price increases accelerated at a faster pace than output stickers. The Iran conflict, furthermore, disrupted supply chains with delivery times lengthening to the longest periods in three-and-a-half years. Meanwhile, new export orders fell for the 49th consecutive month. Jobs expanded in the services industry but fell in manufacturing, a segment that has reduced payrolls every month since June 2023. Going forward, business confidence sank to its lowest level in almost 12 months despite expectations that output would increase in the coming year.

Australia business activity contracted in March for the first time in 18 months with the S&P Global Flash Australia Composite PMI Index dropping from 52.4 in February to 47. It was the steepest decline since December 2023. The services gauge descended from 52.8 to 46.6 and the manufacturing benchmark stayed barely in expansion, dipping from 51 to 50.1. Manufacturing output, however, rose from 49.6 to 49.8

Cost pressures rose with overall input inflation climbing at the fastest rate in more than three years. In manufacturing, the pace was the highest in three-and-a-half years. Businesses were able to pass on only a portion of the higher input costs to customers, which hurt margins. Overall demand, furthermore, weakened despite an increase in export orders. Payrolls, encouragingly, grew in the services sector, but at the slowest pace in four months, although job losses in manufacturing were the most severe since October 2024. Sentiment also weakened with expectations for output hitting a 20-month low.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!