- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 29, 2025 at 12:57 pm

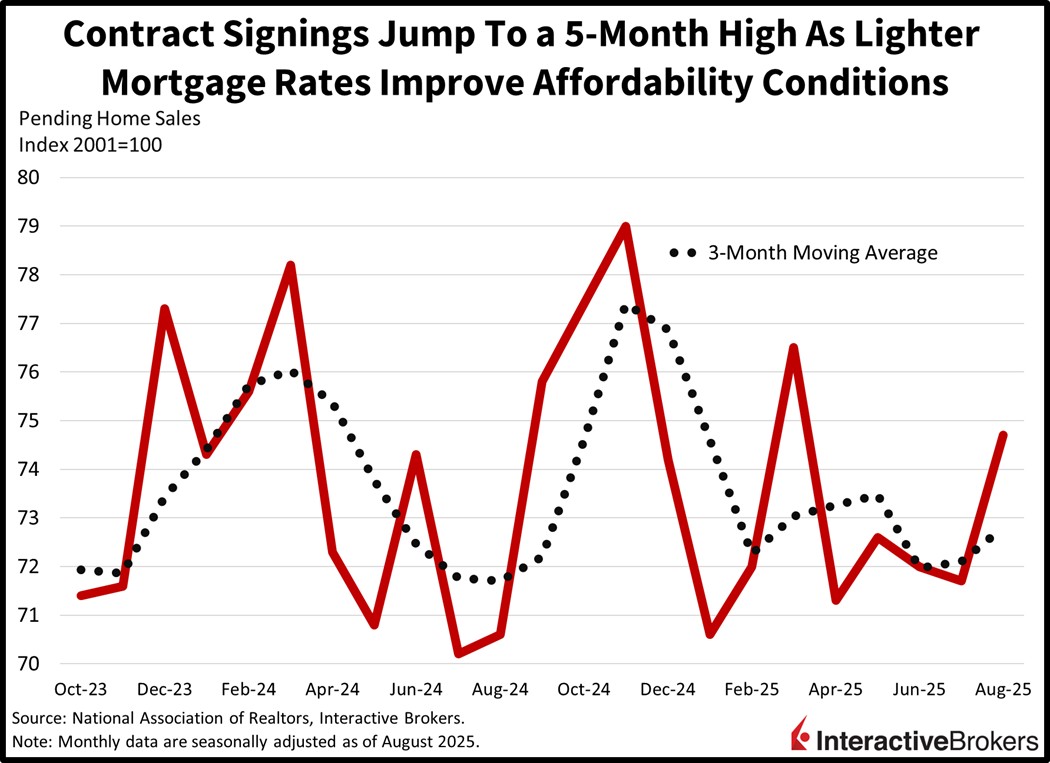

Wall Street is grabbing the bull by the horns to finish off a superb September with stocks, fixed-income and safe-haven commodities rallying. Investors are hoping that the heavy slate of economic data scheduled for this week will signal hiring strength consistent with an ongoing expansion that is supportive of corporate earnings prowess while they cautiously keep in mind that robust numbers could derail rate cut prospects. But Washington shenanigans could block the releases of unemployment claims on Thursday and the nonfarm payrolls main event, Jobs Friday, as folks brace for the elevated likelihood of a government shutdown beginning this Wednesday. President Trump, GOP officials and Democratic party leaders have yet to make any meaningful progress on reaching an agreement, although negotiators are finally meeting for talks today at the White House. Meanwhile, a relatively quiet domestic economic calendar this morning featured a big beat for pending home sales, just a few sessions after closings for new residences marked a 43-month high. Today’s print is adding to evidence that the real estate sector has bottomed. Markets are thriving in the absence of any significant catalysts so far, with equities advancing in all major sectors except energy and utilities. Treasuries are gaining across the curve as well, with yields plunging in bull flattening fashion led south by the longer tenors. Gold set a fresh record, while silver, copper and natural gas commodities also climbed; crude oil and lumber are lower. Bitcoin and forecast contracts are additionally benefiting from the enthusiasm; however, volatility protection instruments are catching bids as participants purchase insurance to protect their portfolios from possible turbulence around the corner.

Pending home sales jumped to a five-month high in August as plunging mortgage rates offered enthusiasm to bidders. Indeed, lighter borrowing costs are improving affordability conditions in the pivotal housing sector and driving a strong recovery in activity. With long-end yields stabilizing amidst not much room to march higher, in my opinion, the bottom is here folks. Contract signings climbed 4% month over month (m/m) and 3.8% year over year (y/y), accelerating sharply from the -0.3% and 0.7% figures in July. Furthermore, the results blew past the median projection of 0.3%. Transactions grew 8.7%, 5% and 3.1% across the Midwest, West and South regions, but declined 1.1% in the Northeast.

The Department of Labor announced around noon today that shall a government shutdown occur, economic data will not be released during the lapse. As the agency potentially declares a full suspension of operations at its Bureau of Labor Statistics, investors will be left in the dark concerning pivotal information regarding the health of employment conditions, which are central to upcoming interest rate decisions from the Federal Reserve. If the closure extends for several weeks, then inflation figures could additionally post a blank on economic calendars across Wall Street. While short disruptions haven’t been disruptive to markets and the economy, longer ones can certainly have an impact. An extended halt would drive consumer spending south and unemployment north, since certain incomes and jobs would be nonexistent for the time being. That would meaningfully raise risks of a slowdown, sending stocks into volatile terrain, although Treasurys would rally strongly.

Europeans’ views of the economy strengthened this month, but a gauge of employment conditions fell, according to the European Commission. On a positive note, the Economic Sentiment Indicator (ESI) climbed 0.6 points to 95.5. Conversely, the Employment Expectations (EEI) Indicator sank 0.9 points to 97.1. Both metrics were below their long-term average levels of 100.

Within the ESI, consumer confidence strengthened by 0.5 points followed by services, which was 0.4 points higher. The industry score advanced 0.3 points. Consumers were less pessimistic about their future finances, and they became more likely to make a major purchase in the next 12 months. For the services metric, managers increased their outlook for future demand and views of past orders, but their assessment of past business conditions weakened. Within the industry survey, production expectations were elevated, a tailwind that was partially offset by the current level of orders.

Conversely, the retail category descended one point in response to lower expectations for future stocks and opinions regarding past business conditions. The impact of those challenges was partial offset by a modest increase in business expectations for the next three months. In another matter, the construction category was unchanged from August.

The EEI weakened in response to services, retail trade and construction businesses scaling back hiring plans. Industry managers bucked this trend with slight improvements in staffing expectations.

Demand for mortgages in the UK declined last month but new consumer credit climbed slightly. The number of mortgage approvals in August, at 64,680, slipped from 65,160 in July and was below the economist economic consensus of 65,000. The aggregate value of mortgages, however, fell considerably more, dropping from £4.51 billion in July to £4.31 billion last month. Economists expected an increase to £4.8 billion. Also in July, new consumer credit increased marginally from £1.66 billion in July to £1.69 billion, exceeding the estimate of £1.6 billion.

Japan’s Leading Index climbed from 105 in June to 106.1 in July, surpassing the economist consensus estimate of 105.9. In the same month, the Coincident Indicator sank 1.8%, which was better than the economist estimate for a 2.6% fall but a reversal from July’s 0.7% northern movement.

Bank of Japan member Asahi Noguchi, an advocate of loose monetary policy, says it’s time for the central bank to raise its key interest rate. His comments come just 10 days after the organization voted to keep its benchmark at 0.5%. His statement points to a possible shift with the BoJ that could lead to a rate hike early next month. Noguchi maintains that the risks of price increases and labor costs escalating now outweigh downside risks.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!