- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 26, 2026 at 1:13 pm

A beat-and-raise earnings report from Nvidia signaled robust demand for AI capital expenditures but stocks are tanking anyway against the backdrop of lackluster moods on Wall Street. Concerns that much of the modern technology’s runway has been covered leading to worries of maturity are generating losses across all of the Magnificent Seven names. More specifically, the quarterly call’s failure to overwhelm expectations sparked today’s turbulence and is sending participants into safe-haven instruments. Folks piled into the rotation trade at the opening bell, bolstered by softening interest rates amidst lighter-than-expected unemployment claims; however, the Dow Jones Industrial and Russell 2000 are now joining the S&P 500 and Nasdaq 100 in the red, as just 3 of the 11 major sectors appreciate on the session. Yields are plunging in bull-flattening fashion led by duration, as fixed-income observers consider the possibility that weakening investor sentiment could drive an economic slowdown irrespective of the strong fundamentals within the cycle. Treasuries and the greenback are gaining simultaneously in light of defensive winds throughout markets with put option premiums and volatility levels climbing. Cryptocurrencies are getting battered as enthusiasm dives, while forecast contracts and commodities are catching bids overall.

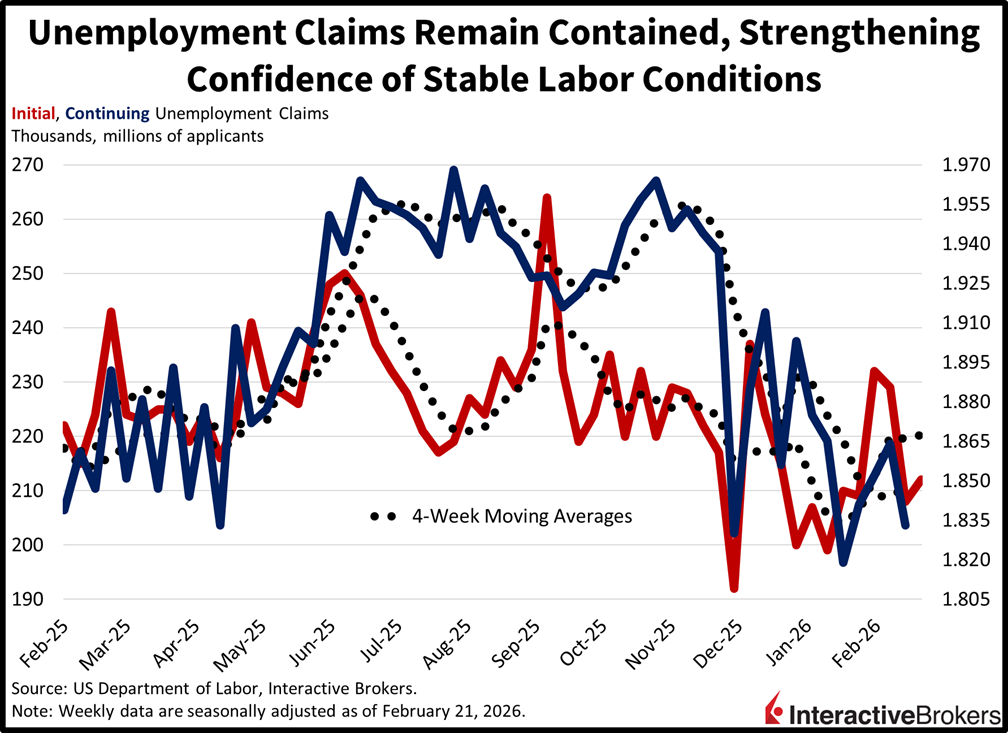

Unemployment claims continue to reflect a lack of layoff appetite across corporate America, as workforce reductions remain contained. Indeed, initial applications totaled 212k for the week ended Feb. 21, better than the 215k expected but slightly higher than the 208k from the prior period. Continuing filings sank to 1.833 million in the interval culminating on Feb. 14, beneath the median estimate of 1.860 million and the previous timespan’s 1.864 million. Four-week moving averages were little changed, standing at 220.25k and 1.848 million.

Early trading favored the cyclicals as participants rotated away from tech in light of maturity concerns. Nonetheless, the Magnificent Seven firms carry too much weight within investor psyche, and it is incredibly difficult to replace their role in supporting Wall Street’s enthusiasm for equities. Furthermore, the lack of growth narratives surrounding the old-school names in the market could cap their gains on a relative basis, as the companies struggle to counter 2026 weakness across the AI theme. Indeed, the Dow Jones Industrial and Russell 2000 benchmarks are already higher by 2.6% and 6.3% year to date, but with the Nasdaq 100 unable to catch up and collect bids, there’s significant risk of a down year in stocks overall. Meanwhile, Treasuries are still attractive, as decelerating inflation and progress on the deficit are poised to send the 10-year south of 4% soon while the 30-year tenor takes out 4.65%. Tariff revenues, if sustained, can drive even more meaningful Treasury asset appreciation.

The AI theme appears healthy when assessing industrial production in Singapore. In January, overall output climbed 16.6% year over year (y/y) and 5.3% month over month (m/m), exceeding the economist consensus expectations for 11% and 4.5% and strengthening from December’s 10.9% y/y gain and -0.3% m/m contraction.

Electronics production soared 44% y/y with AI-related products accounting for the strong demand for semiconductors. Factories were also busy fulfilling orders for electronic modules and components. Other leading categories and the extent of their growth were as follows:

The biomedical manufacturing sector, however, sank 33.1% with disappointing results for biological products and active pharmaceutical ingredients. Medical devices were also weak.

The February Economic Sentiment Indicator (ESI) for the euro area sank one point to 98.3, a worse reading than the 99.8 anticipated by a consensus of economists. The Employment Expectations Index, furthermore, dropped 0.6 points to 97.6. In both instances, the results were below the long-term averages of 100.

The ESI was pulled down by weakening confidence in the services sector with the category sinking from 7.2 to 5. Economists anticipated that the gauge would increase to 7.5. All three components of the category, past demand, past business situation and expectations for future demand, deteriorated. While confidence among industrial companies and consumers was unchanged, an uptick in sentiment among retailers helped to partially offset the impact of the services sector’s outcome.

Within the Employment Expectations Indicator, softening plans for staffing among services providers were the strongest headwinds. Retail trade improved but only partially offset the broader impact of the services industry. Consumer confidence, meanwhile, was unchanged at -12.2, which met the economist consensus estimate.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

It’s safe to say the US deadlines against Iran are at hand and a major event over there will cause an equally major drop. So, safe bets to go into puts and out of stocks for now. I see gold rose about the same % the SP fell so a safer play until this threat blows over.