- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 25, 2026 at 11:00 am

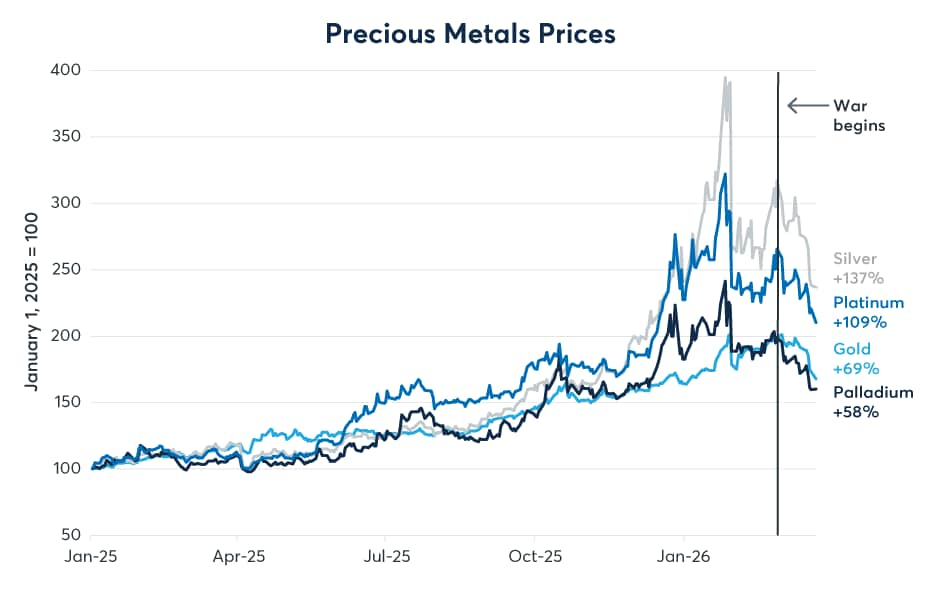

The outbreak of war in the Middle East has stoked the prospects for higher inflation, disrupted energy supply chains, boosted military spending and intensified geopolitical uncertainty. This should have carved out a bullish environment for precious metals as a safe haven. Instead, gold, silver, platinum and palladium prices have fallen sharply since the conflict began on February 28, adding to declines that began in the last week of January (Figure 1). So, what’s fueling this downtrend, and what are their prospects going forward?

Several factors drove precious metals prices higher from early 2025 through late January 2026 that can be boiled down to one basic fundamental: fear of inflation. The factors that fed inflation concerns include:

But this dynamic began changing in January with the nomination of Kevin Warsh to lead the U.S. Federal Reserve (Fed) in mid-May. Markets saw him as somebody who was likely to strike an independent stance on monetary policy and a long-time opponent, or at least a skeptic, of quantitative easing, a central bank policy of buying government bonds and financial assets to inject liquidity into the economy. With the idea of the Fed losing independence fading, precious metals prices fell sharply. By late February, however, precious metals prices were on their way back up before the Mideast conflict broke out.

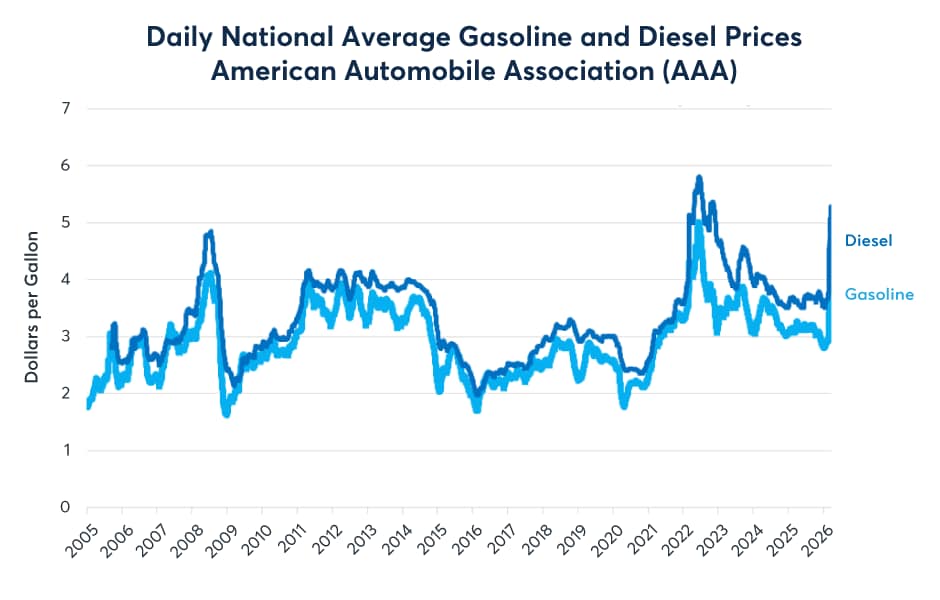

The conflict has proven to be bad news for gold, especially for palladium, platinum and silver. In some ways this may appear to be paradoxical. Consumer prices for gasoline and diesel fuels have jumped sharply. According to data from the American Automobile Association (AAA), Americans are now paying nearly $1 per gallon more for gasoline and $1.50 more for diesel (and heating oil) than they were in February. Given that gasoline and other fuels account for up to about 3% of the consumer price index (CPI), this could push headline U.S. inflation as much as one percent higher over the next couple of months if prices of these fuels stabilize at their current levels (Figure 4). And, the rise in prices could be even more pronounced in the rest of the world, where crude benchmarks like NYMEX’s Brent Last Day Financial Futures are trading $15 higher than West Texas Intermediate (WTI) crude oil while GME Oman crude is over $60 higher than WTI. This suggests a potentially bigger energy inflation shock across Europe and Asia than in the U.S.

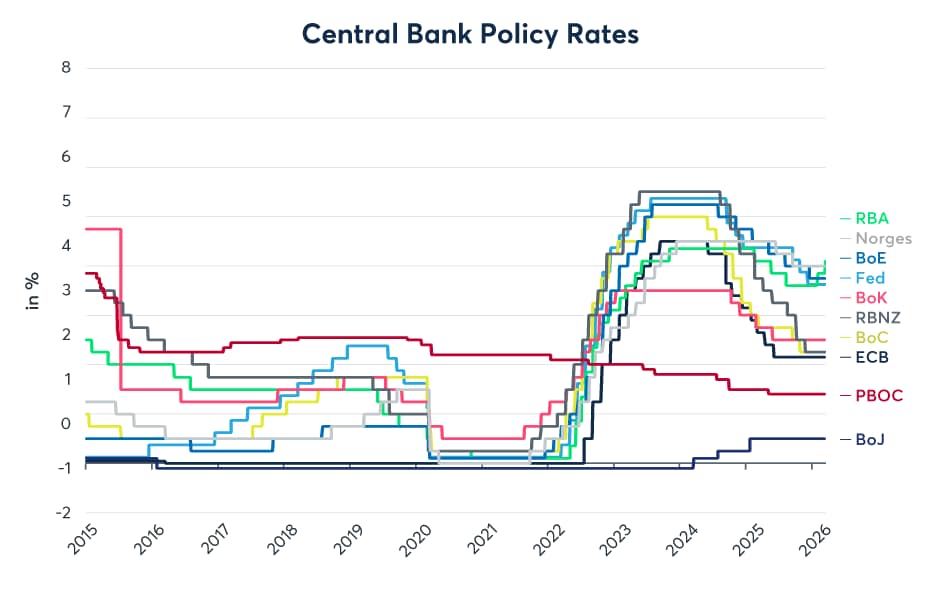

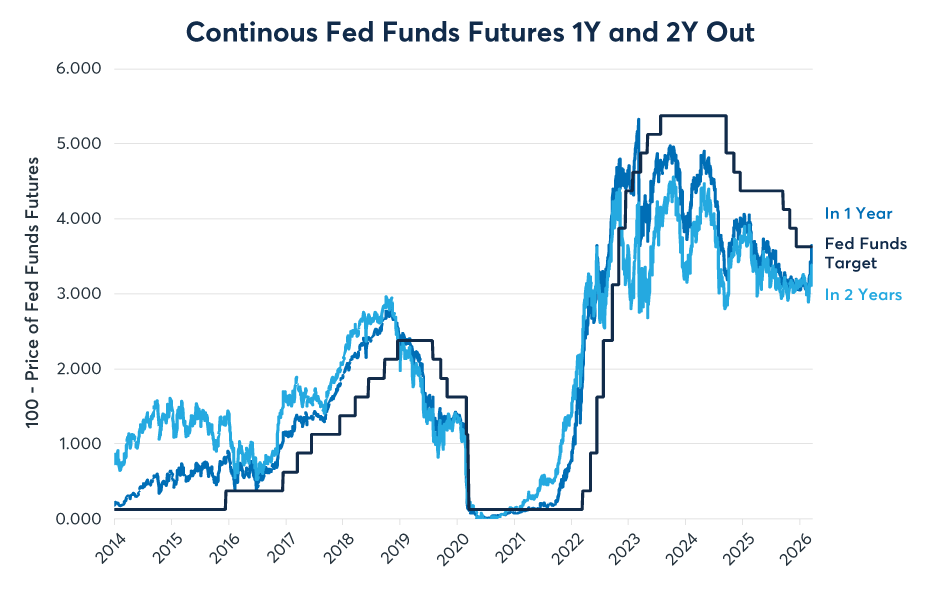

Now that higher inflation, at least in the very near term, is crystallizing, it isn’t good news for precious metals for a simple reason: central banks are beginning to reverse course and consider rate hikes. In the U.K., the Bank of England suggested that it might hike rates as many as three times. The European Central Bank has also warned of potentially higher rates. While the Fed suggested after its March meeting that it still penciled in one 25-basis point rate cut for 2026, Fed funds futures have largely de-priced any further Fed rate cuts for 2026 and 2027 (Figure 5). The prospects for fewer rate cuts, or even rate hikes, make holding fiat currency relatively more attractive compared to precious metals than it seemed when investors still priced deeper rate cuts.

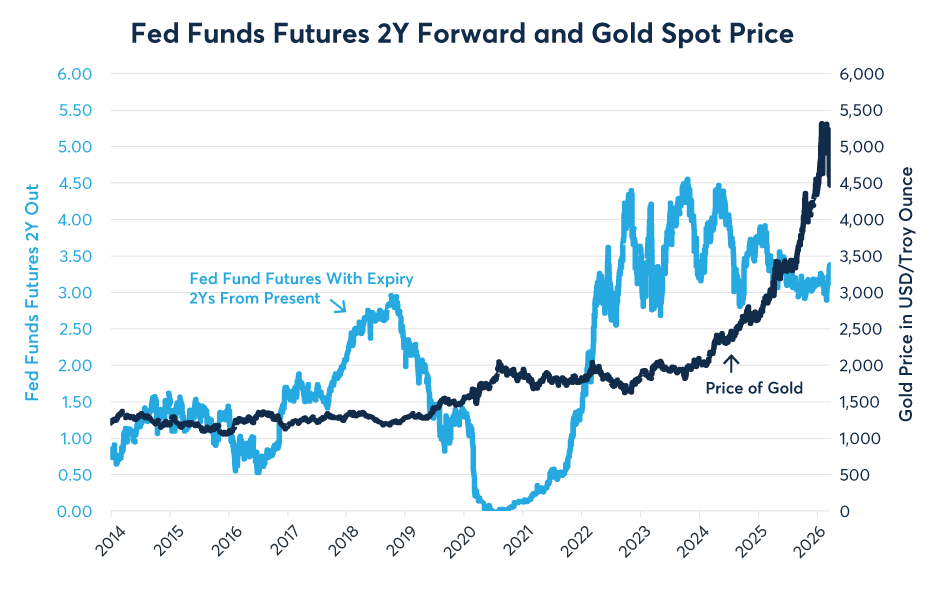

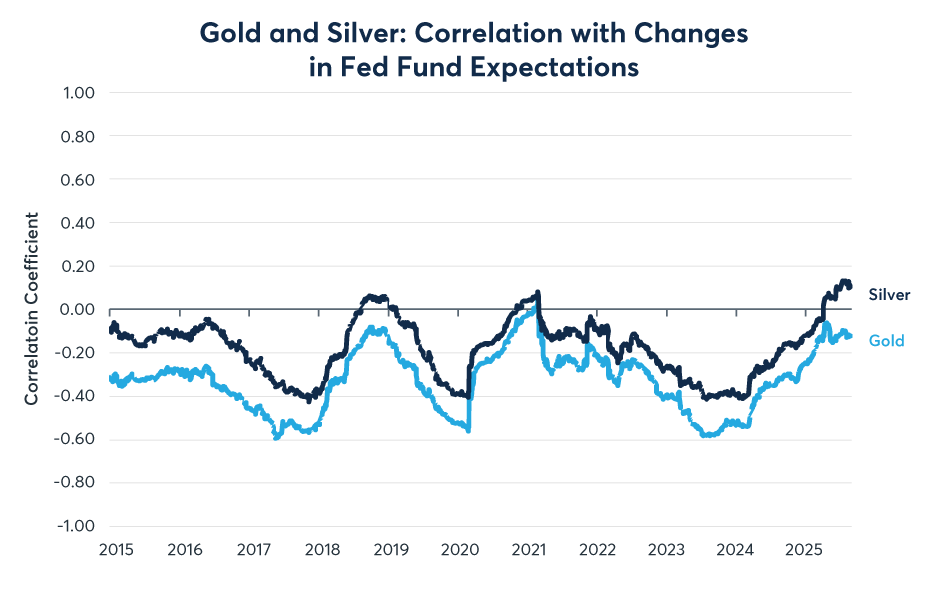

In some ways the 2025-2026 behavior of precious metals is reminiscent of the period from 2019-2023. From early 2019 to mid-2020, gold prices soared as markets de-priced expected Fed rate hikes and the central bank eventually put rates at zero at the beginning of the pandemic. Then, from 2021 through 2023 when inflation rose, gold prices fell from $2,100 back to $1,600 as a result of central banks having to undertake the biggest tightening of interest rate policy since the late 1970s (Figure 6). It was a classic case of “buy the rumor, sell the fact.” Gold and silver accurately anticipated higher inflation to come in 2019 and 2020 but when it actually arrived, inflation proved to be bad news, at least in the short-term, because precious metals are usually negatively sensitive to rate expectations (Figure 7).

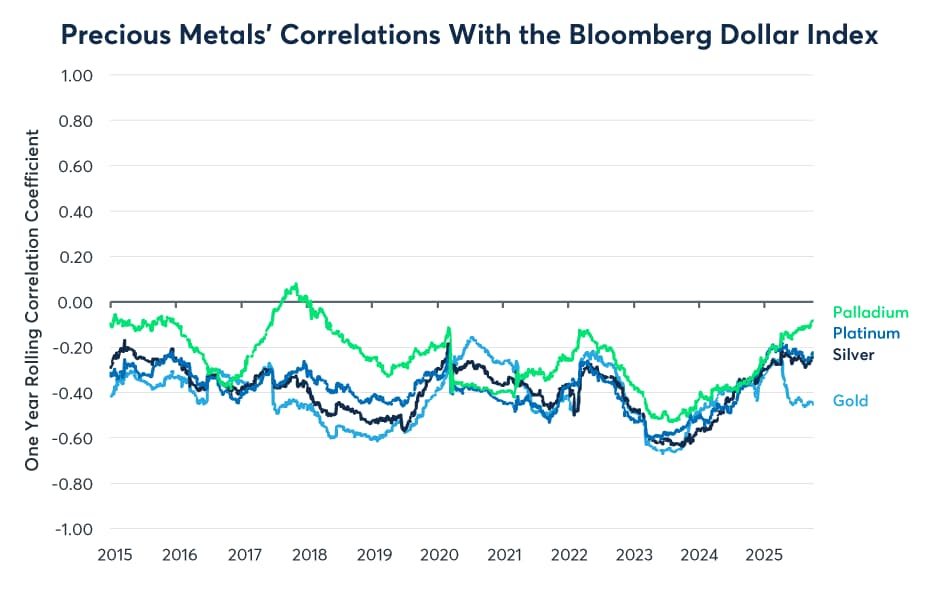

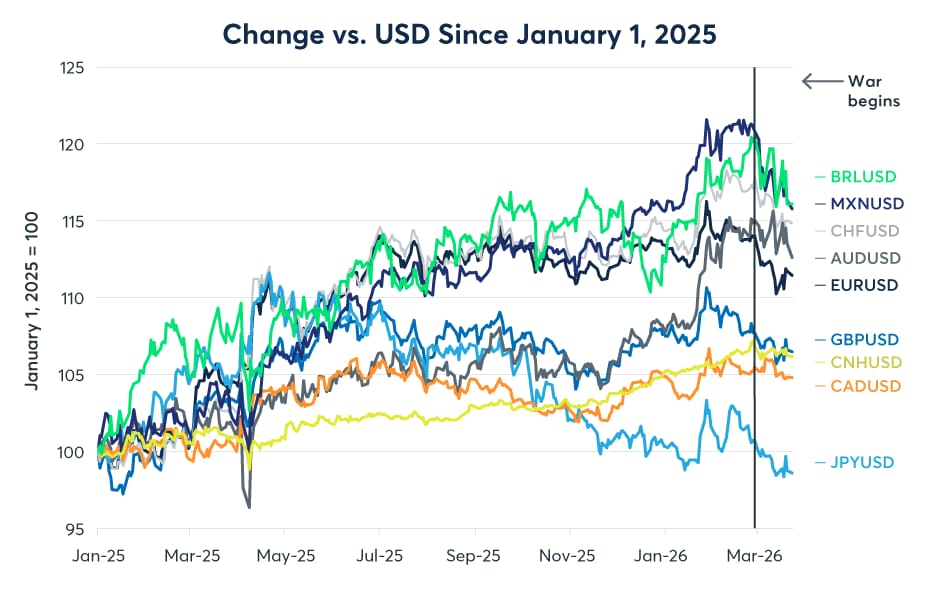

The U.S, dollar (USD) mostly fell from late 2024 to early 2026. This probably also strengthened gold and the other precious metals which correlate negatively with the daily changes in the Bloomberg Dollar Index (Figure 8). Since the Mideast conflict broke out, however, USD has proven to be a flight-to-quality instrument and has rallied versus most other currencies to the detriment of precious metals (Figure 9). This coincides with a general de-risking of portfolios that has led to a minor decline (so far) in equity prices, crypto assets and other risk-on assets.

Many of the fundamental factors that led precious metals prices to rise are still present. Most critically, there is no effort to rein in budget deficits in any major economy. Moreover, the conflict will likely lead many countries to further boost military spending as they adapt their armed forces to a rapidly changing technological landscape. Indeed, even before the war, the U.S. Administration requested a permanent boost of 50% or $500 billion per year for U.S. defense spending and have recently requested $200 billion to replenish depleted stocks of munitions.

When it comes to central banks, some of them may follow the Reserve Bank of Australia towards tighter monetary policy, but any policy tightening will likely be much milder than what occurred in 2022 and 2023. Indeed, certain central banks, like the Bank of Japan, have even delayed planned rate hikes because of concerns that higher oil prices will slow growth. Precious metals prices began to emerge from their 2020-2023 period of consolidation led by gold as central bank rates topped out and expectations of policy easing began to form in the markets. When investors start to price renewed central bank easing at some point in the future, this could also help to spark another precious metals rally, especially if core inflation remains above target.

—

Originally Posted March 23, 2026 – Do Retreating Precious Metals Prices Offer a Buying Opportunity?

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

U.S. Spot Gold trading through IB LLC accounts is only available to legal residents of the United States that do not reside in Arizona, Montana, New Hampshire, and Rhode Island.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Spot currencies are not available at IBKR Singapore.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!