- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

It has struck us for some time that crude prices continue to reflect an overly optimistic view about when normal shipping will resume in the Strait of Hormuz. There is no acceptable military solution available to the US. The Iranian threat will stop when Iran so decides. Nonetheless, every positive social media utterance from President Trump draws algorithmic selling of crude oil futures and related energy stocks.

In late May Bernstein hosted executives from both Exxon Mobil and Chevron at their 42nd Annual Strategic Decisions Conference. Energy insiders have long been warning about the price risks caused by depleting oil inventories. Nonetheless, the transcript was startling.

XOM SVP Neil Chapman said, “We’re approaching unheard of inventory levels…going to hit really low levels in two weeks or three weeks. But once you get to that point, then you’ll see prices shoot up.” Chapman thinks Brent crude could soon reach $150-160.

Chevron CEO Mike Wirth warned that, “…the buffers and the shock absorbers are being steadily drawn down and the ability of the market to absorb this imbalance is drastically diminished today versus where we started.” He added, “,,,there’s more upward pressure that I would expect as we get into June and certainly into July.”

Neil Chapman felt that the loss of Persian Gulf supply has been partly offset by large volumes of sanctioned crude from Venezuela and Russia that was already in ships and became available to buyers. Much of that has now gone. China also stopped building their substantial supplies of stored crude.

Mike Wirth expects that even after shipments return to normal through the Strait of Hormuz, rebuilding strategic stocks that have been drawn down will increase demand, boosting prices.

Trafigura also warned that inventories were dangerously low when reporting a doubling in quarterly profits on Thursday.

When the Strait opens up, you could see a rush to rebuild stocks that would push prices higher. Many operators might worry that any peace deal is fragile and rush to take advantage of supplies while they can. There’s little point in building inventories when supply is constrained. It would be ironic and not a little frustrating to the White House if they announced a deal to re-open the Strait and oil prices rose. It seems to us a plausible result.

Trading is driven by algorithms that sweep news stories faster and more efficiently than any human. When I was trading interest rate futures in the 80s and 90s, occasionally a story would break that allowed a profitable trade for those with fast enough reactions. That time long ago passed.

I wonder if the transcript from a sell-side conference doesn’t receive the same type of AI analysis as the regular posts from our president. Executives at America’s two biggest energy companies both see a plausible risk for oil prices to jump 50% in a month or two. That offers more important insight into future prices than the regular promises from the White House that the Strait will soon open.

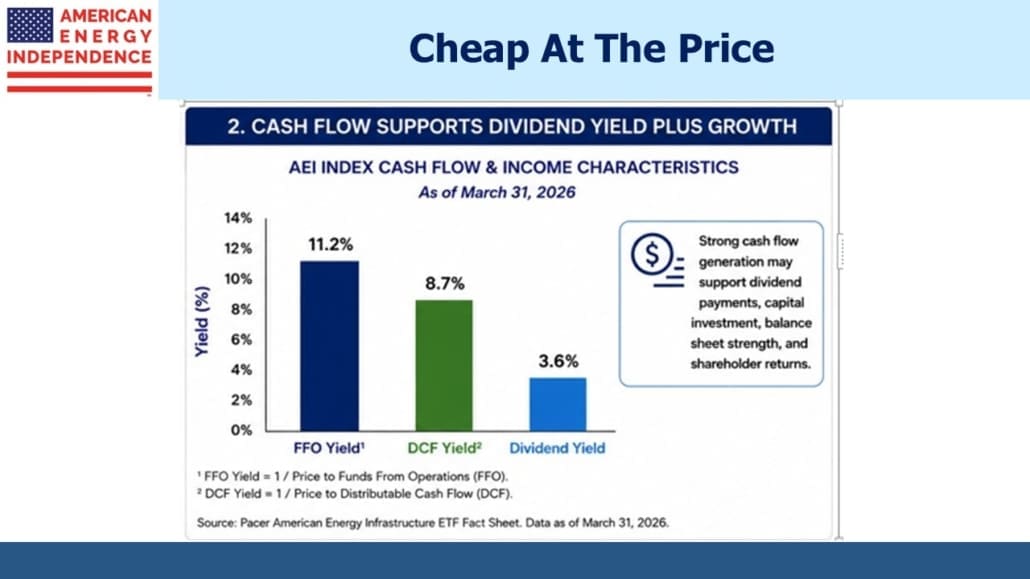

Investors often ask me what percentage of my investable assets are in midstream energy. It’s a high percentage, balanced with a healthy dollop of treasury bills. Why not diversify? During the pandemic a concentration in energy wasn’t a pleasant experience, but the sector rebounded strongly and the 14.1% ten year return on the American Energy Infrastructure Index (AEITR) is steadily closing in on the S&P500’s 15.6%.

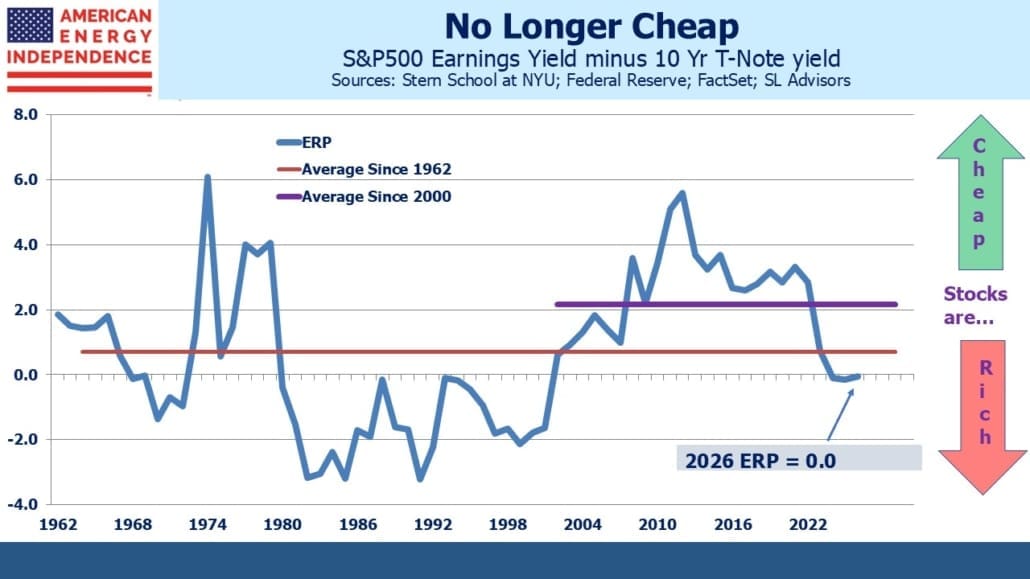

With current valuations it’s not clear that diversifying towards the S&P500 would be helpful. The Equity Risk Premium (ERP) shows stocks to be at their most expensive in a quarter century. On a relative valuation basis I find the cash flow multiple in midstream more compelling.

The ERP isn’t a great timing tool. It’s been showing stocks as overvalued for at least three years. During this time earnings have grown at double digits, justifying historic purchases. Factset shows 2026 earnings growth of 23% and 15% next year, which supports today’s apparently lofty valuations. The AEITR’s cash flow yield is over 2X the S&P500, reflecting the latter’s growth orientation but also the bullish outlook of so many investors.

The big four hyperscalers (Google, Meta, Amazon and Microsoft) are projected to have depreciation expense of $200BN next year. All the numbers related to AI are superlative, and there’s a case the revenues will easily justify valuations. But if things don’t work out as currently priced, to quote a long-time friend who used to run government bond trading, “Down’s a long way.”

We prefer the predictable cashflows of midstream energy stocks.

—

Originally Posted June 7, 2026 – Is Crude At A Tipping Point?

Please go to following link for important legal disclosures: https://sl-advisors.com/legal-disclosure

SL Advisors is invested in all the components of the American Energy Independence Index via the ETF that seeks to track its performance.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SL Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or SL Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

{kind=link}

{kind=link}

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!