- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 26, 2025 at 12:59 pm

One of the classic adages that guides my thinking is “don’t short a dull tape.” The construction is anachronistic – there hasn’t been a ticker tape in decades – but the logic is not. Periods of low volume imply lower liquidity, and lower liquidity implies that intraday moves can get extended. We’re seeing this in action this week, and it could easily persist on Friday’s half-day/month-end.

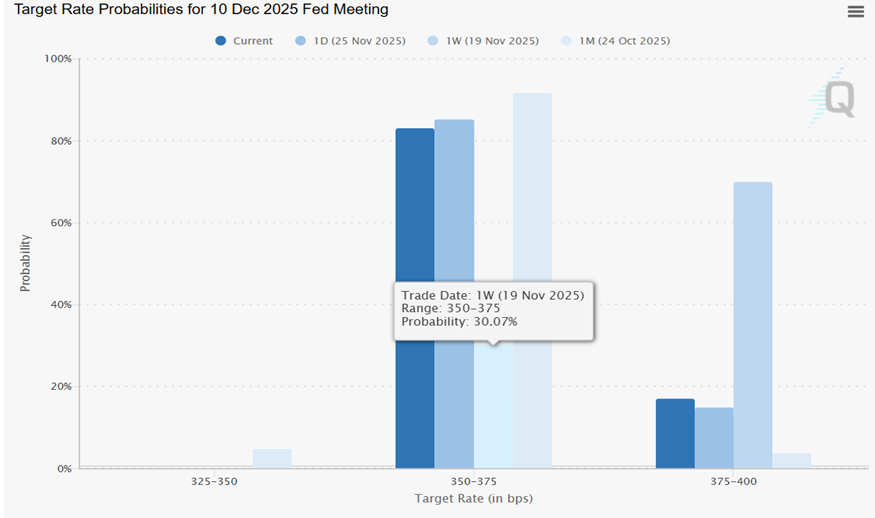

There is a solid rationale for the recent enthusiasm that is taking advantage of the pre-holiday relative lull. As we noted last week, the market’s mindset flipped almost instantly on Friday morning after comments by New York Fed President Williams that he favored a 25-basis point cut in the Fed Funds target rate at the upcoming December 10th meeting. We saw an immediate near doubling in the market’s expectations for a cut, and those odds have continued to improve in the ensuing days. Both the CME FedWatch and ForecastEx currently show a roughly 82% likelihood for a cut as I type this. This is up from roughly 30% just last week.

Source: ForecastEx

Source: CME

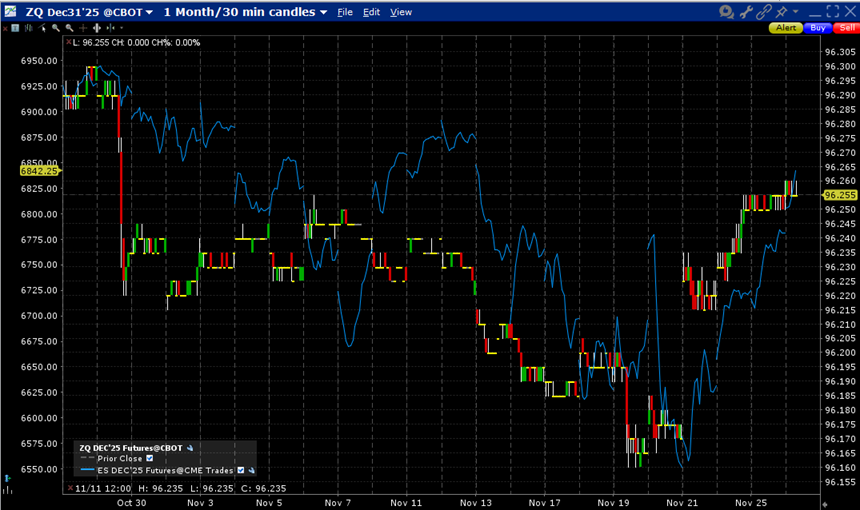

Stocks love the prospect of interest rate cuts. They are catnip to liquidity-loving traders. Heck, there is a reason for the more powerful adage “don’t fight the Fed.” Liquidity is the lifeblood of financial markets, and if the Fed is planning to make liquidity either more plentiful or cheaper, there is little reason to stand in the way of that activity. The following chart shows the relationship between Fed Funds and ES (S&P 500 Mini) futures since the last FOMC meeting – which, not coincidentally, was the last closing high for the S&P 500 (SPX) index:

Source: Interactive Brokers

When we look at the chart above, the influence of Fed Funds on SPX becomes apparent. Yet as last Thursday’s huge reversal was occurring, we noted the short-term relationship between NQ (Nasdaq 100 Mini) futures and bitcoin, and blamed a slide in bitcoin for turning enthusiasm for Nvidia (NVDA) earnings into a substantial decline. Various factors can influence stocks at any given time, and the recent precarious nature of the cryptocurrency markets amidst a sustained decline in those assets was enough to flip the mood among a wide group of active traders. A big part of bitcoin’s recent uptrend was powered by the popularity of bitcoin ETFs in the wake of a new crypto-friendly administration. But that also meant that there was a convergence between those who traded and invested in cryptocurrencies and stocks. As I put it recently,

The bottom line is, bitcoin is for normies now. As a result, the normies are going to view it as another speculative holding in their portfolio … it’s going to be treated like a volatile mainstream investment.

But after that brief flirtation with using bitcoin as a “lead” for stocks, we’re back to the more meaningful relationship between rates and stocks. We can certainly question whether 25 basis points is really worth adding trillions of dollars of market capitalization to the entire stock market, but that would be nitpicky. This is less about the effect of short-term rates on the bottom lines of index constituents than the willingness of investors to expand multiples (paying higher prices for a given level of earnings) when rates decline.

Back to the original premise of “don’t short a dull tape” – when volumes and trader attention decline, so does liquidity. Spreads widen and posted sizes shrink, meaning that less volume is required to get prices moving. Given the path of interest rate probabilities and its tight relationship with major indices, it is quite possible for sizeable rallies to take hold on skimpy volume. The recent average daily volume on the consolidated US tape is around 19 million shares. Monday’s sharp advance occurred on roughly that level of volume. We normally want to see major moves be bolstered by higher-than-average volume, which was the case last Friday. Volumes were nearly 11% lighter yesterday, and the pace is even slower today. Yesterday we noted that Friday’s half-day coincides with month-end, meaning that an institution that wants to do a bit of window dressing might find it especially easy under those conditions. We may be getting overbought and overextended on a short-term basis, but it is difficult to stand in the way of a concerted advance when volumes are light.

Happy Thanksgiving to those who celebrate. Happy Thursday to everyone else.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

La negociacion de futuros, contratos de eventos y contratos de pronóstico no son adecuados para todos los inversores. Antes de operar con estos productos, por favor lea la divulgación de riesgos de la CFTC. Para una copia visitenos aqui <a href="https://www.interactivebrokers.com/en/general/homepage-disclosures.php

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!