- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 6 of 11

New to Interactive Brokers?

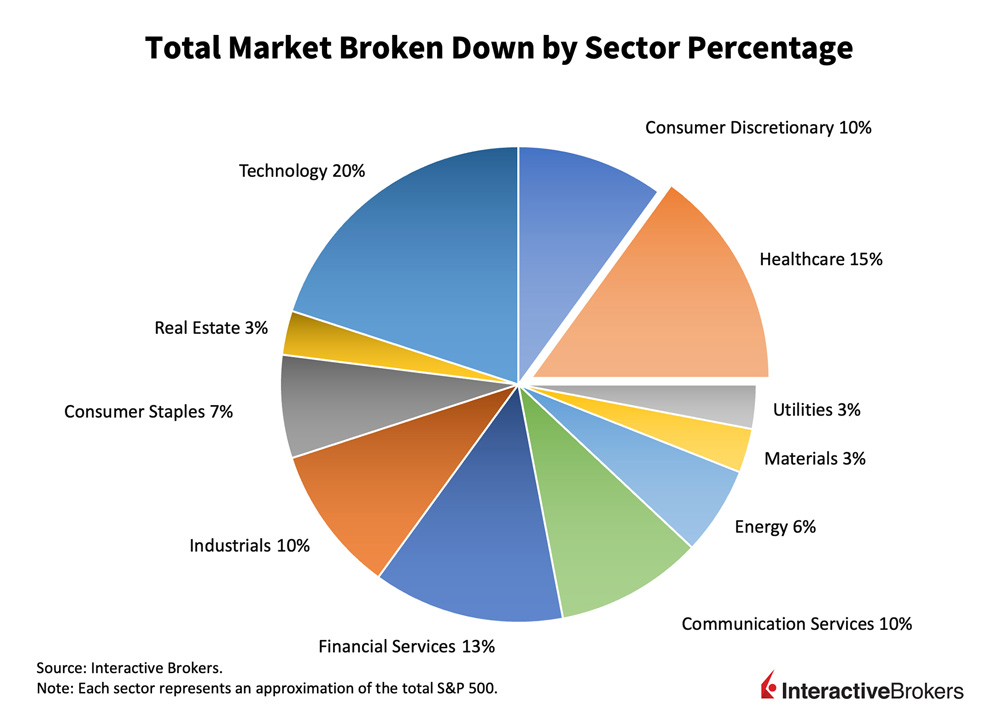

The Healthcare Sector is the second largest of the eleven sectors that comprise the economy. The sector represents approximately 15% of the total market, and approximately 17.3% of the US GDP as of 2022. Between 2021 and 2022, the sector grew 4.1%, reaching $4.5 trillion or $13,493 per person. In 2022, 14.7 million people aged 16 and older were employed in healthcare occupations, accounting for 9.3% of total employment in the US. Investing in the Healthcare sector is widely considered valuable among investors and financial advisors as there is always a demand for healthcare products and services regardless of overall market growth or direction. For example, despite setbacks in international GDP and economic growth from the COVID-19 pandemic, the healthcare sector grew significantly as the world required research and invested money into preventing the pandemic from growing.

The broader healthcare markets have experienced significant growth and transformation in recent years, with national health spending exceeding $5 trillion, according to Alterum’s June 2024 Health Sector Economic Indicators (HSEI) brief. This growth trajectory reflects the increasing demand for health care services and the ongoing advancements in medical technology and treatment methodologies. Notably, the growth in health spending has outpaced nominal GDP growth, indicating a shift towards prioritizing health care expenditures amidst broader economic expansion. This trend is particularly evident in the personal health care spending category, which saw a 7.6% year-over-year growth in April 2024, driven by factors such as increased utilization and the continued evolution of health care delivery models.

Furthermore, the healthcare price growth reached a 15-year record high, signaling a period of inflationary pressures within the sector. This increase in prices has implications for both providers and payers, affecting the profitability of health care organizations and the affordability of health care services for consumers. Job openings in the healthcare and social assistance sectors also reflect the sector’s vitality and the need for skilled professionals to meet the demands of an aging population and the ongoing technological advancements in medicine.

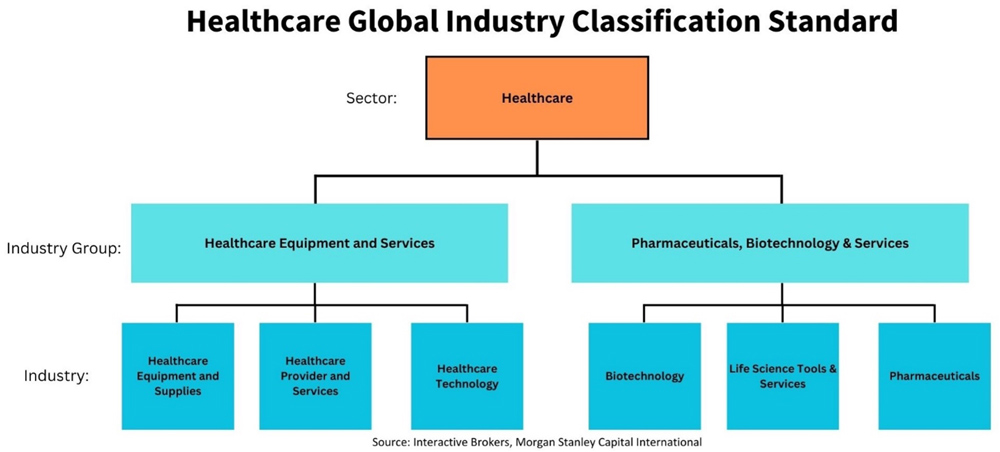

Underneath the umbrella of the Healthcare sector, there are two industry groups and six industries that can be further established. The first industry group is Healthcare Equipment and Services, under which are the industries of Healthcare Equipment and Supplies, Healthcare Provider and Services, and Healthcare Technology. These industries include companies that manufacture equipment and supplies, companies that own and operate healthcare facilities, and ones that engage in research and development. The second industry group is Pharmaceuticals, Biotechnology and Services, under which are the industries of Biotechnology, Lie Science Tools and Services, and Pharmaceuticals. These industries include companies that perform research and development derived from living organisms, companies that develop and produce chemical vaccines, and companies that study living things and provide analytical tools.

As mentioned before, the Healthcare Sector is often viewed as a ‘safe haven’ for potential growth opportunity with investors. Since demand for healthcare is price inelastic, meaning demand will remain stable when prices fluctuate, the sector is resilient to changes in the business cycle.

This does not mean that investing in the Healthcare sector does not come with certain risks. Because of the intertwining nature of private and public healthcare, the sector can often be subject to significant government intervention. This can be difficult when private companies are incentivized to maximize profit, yet public ones are incentivized to serve the good of the people. This dichotomous nature means the government must regulate the sector cautiously and ensure that individuals can have adequate access to the services they require. Furthermore, political influences in the sector can create uncertainty for investors, therefore monitoring policy changes is key.

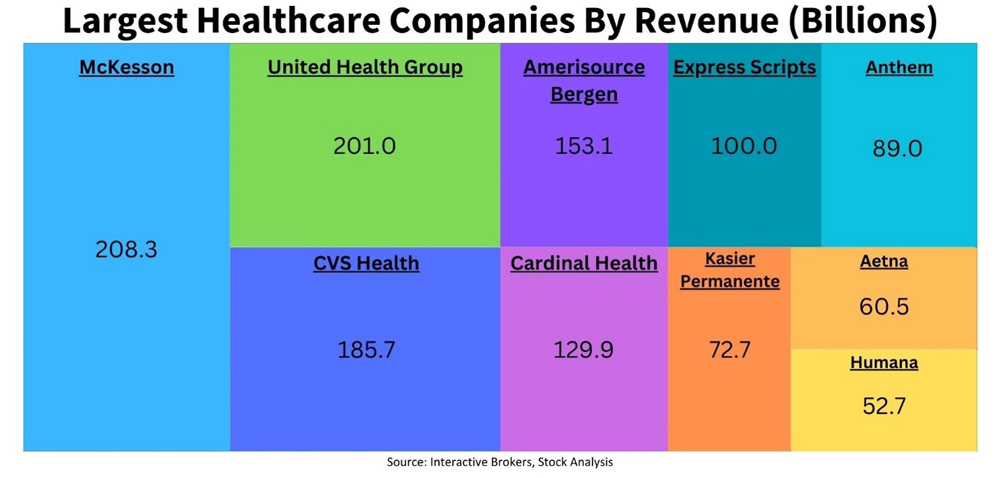

When investing in the Healthcare sector, it can be a powerful tool for investors to select a specific industry in which they want to grow their wealth. Investing in biotechnology and pharmaceuticals can be beneficial for those who want to invest in smaller companies and feel confident about certain medical advancements. However, this can be riskier as the market value of the company may depend entirely on the expectation that a drug or treatment will gain approval by the FDA. Some larger biotech and pharmaceutical companies include Johnson and Johnson (JNJ), Gilead Sciences Inc. (GILD), and Pfizer (PFE). Investing in the Healthcare Equipment and Supplies industry can be beneficial as there is a constant demand for medical products. Medtronic PLC (MDT) is an example of a medical equipment manufacturer that one can invest in. The Healthcare Services industry is comprised of companies that provide health insurance policies, currently dominated in Medicaid by UnitedHealth Group Inc (UNH), Anthem Inc (ELV), Aetna Inc (AET), Molina (MOH), and Centene (CNC).

Investing in the Healthcare sector is beneficial as it can be personalized by industry and benefit companies that are at the forefront of medical innovation. Industry leaders such as UnitedHealth Group Inc (UNH) and Johnson & Johnson (JNJ) contribute to the sector’s expansion despite fluctuations in the business cycle. These companies develop new treatments and services that address some of the most prevalent and life-threatening health challenges, making the healthcare sector a compelling investment opportunity for those seeking to align their portfolio with positive societal impacts.

There are a set of advantages and disadvantages to investing in the Healthcare sector that individuals must carefully consider when deciding to make an investment.

In terms of benefits, the healthcare sector plays a vital role in the economy, contributing a substantial portion of GDP and driving high demand for services. As stated before, the price inelasticity of healthcare services means that demand remains relatively stable during economic downturns, providing a degree of stability to investors’ portfolios. Ongoing research and development efforts also promise continuous innovation, potentially leading to breakthroughs that could revolutionize healthcare delivery. For example, Moderna (MRNA) was the first to bring a COVID-19 Vaccine to clinical trials.

Investing in Healthcare does come with potential disadvantages. Government intervention and regulations pose significant risks, as changes in policy or regulatory oversight can dramatically affect the profitability and operations of healthcare companies. High uncertainty regarding costs and outcomes is another challenge, given the rapidly evolving nature of medical technology and the complexity of healthcare delivery systems. Asymmetric information challenges also exist, with disparities in access to information potentially leading to inefficiencies and inequities in the healthcare market. Furthermore, political risks, such as discussions around universal healthcare and proposals including “Medicare for All,” introduce additional layers of uncertainty for investors. Regulatory risks, including the potential for failure to secure FDA approvals, further complicate the investment landscape.

Despite these challenges, the Healthcare sector is both resilient and has demonstrated long-term profitability, driven by demographic trends, technological advancements, and the continuous demand for health services.

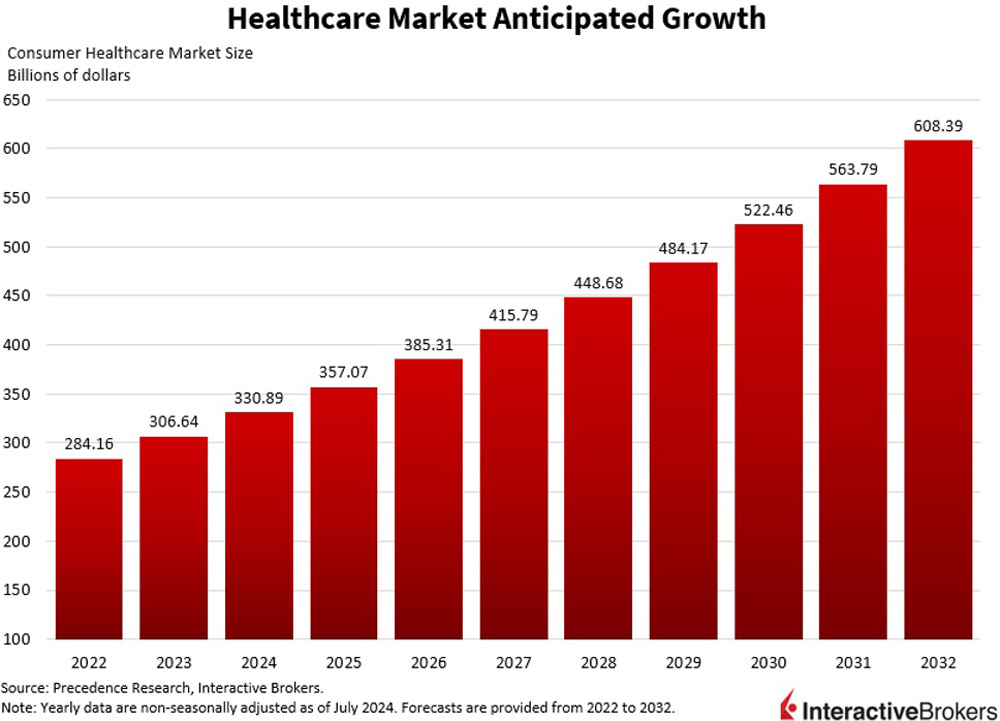

There is a potential positive outcome for investments in the Healthcare sector for the future. Predictions indicate that healthcare profit pools will expand at a compound annual growth rate (CAGR) of 7.0% from 2022 to 2027, reflecting the sector’s resilience and potential for sustained growth. The anticipated recovery in early 2024, fueled by margin and cost optimization and reimbursement-rate increases, suggests a favorable environment for investors. Several segments within the healthcare sector are expected to experience potential growth. The payer segment, particularly Medicare Advantage, is benefiting from the rapid growth in the dual’s population and the post-pandemic recovery of margins. Health systems, especially outpatient care settings, are seeing growth driven by shifts in the site of care. The healthcare software and technology sector (HST), including patient engagement and clinical decision support platforms, is flourishing, with an estimated CAGR of 12% from 2022 to 2027. Pharmacy services, especially specialty pharmacies, are also experiencing rapid growth, with total pharmacy dispensing revenue projected to reach $700 billion by 2027.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

No mention of the anger felt by many people at the Delay, Deny, Defend approach favoured by most large companies. I wouldn’t invest in these companies because of their appalling ethics