- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 22, 2026 at 11:25 am

The White House has extended the ceasefire with Iran to give peace talks enough time to run their course. Unfortunately, the statement offers little clarity to investors. Iran and Israel have not confirmed if they’re on board with the plans. Reportedly, Iran has attacked at least three ships in the Strait of Hormuz since the new ceasefire announcement.

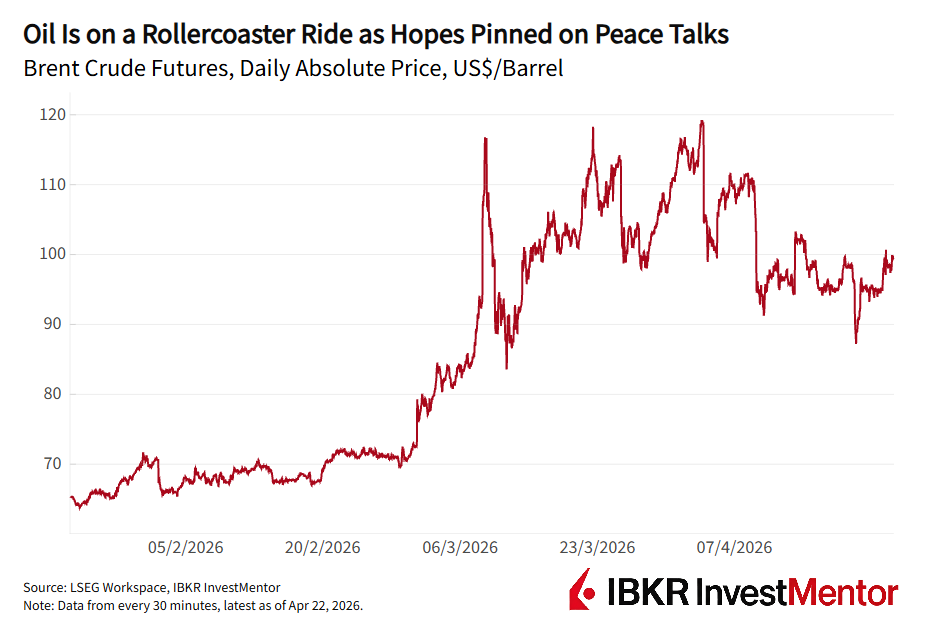

The planet’s most important energy corridor remains largely impassable, with Iran intercepting foreign vessels and the US Navy blocking Iranian traffic. On-off peace negotiations and a patchy ceasefire have somewhat reined in the oil shock, but Brent touched above $100 a barrel again on Wednesday.

The final pre‑war tankers that slipped out of the Persian Gulf in late February have reached their destinations in places like Malaysia and Australia. Europe received the final shipments a week earlier. Saudi Arabia and the Emirates can move some of their oil via pipelines, but the majority is stuck behind the blockade. The International Energy Agency has estimated a peak supply loss of about 12 million barrels per day, amounting to 11.5% of the global oil demand. This will likely continue as long as the strait remains closed.

The shock is now spilling from charts to the real economy, with physical shortages already apparent in Asia.

“The price of oil” quoted daily in the news is usually the latest Brent front-month contract, meaning the nearest futures contract that hasn’t expired yet. This week, Brent has traded around $95-$100 per barrel.

Refineries don’t run on promises of later deliveries. They have a constant need for the actual product. Forties Blend, a benchmark that follows spot prices of North Sea oil, has been trading as much as 50 dollars above Brent futures. That gap is a sign of stress. It shows refineries are willing to pay a steep premium to secure physical oil right now.

The physical market is pricing a world where barrels are scarce, logistics are broken, and the speed of recovery is uncertain. The Gulf exports via the strait have hit a near-total halt, and many of the oil production facilities in the region are badly damaged.

Jet fuel is often the first refined product to feel pressure in an energy crisis, and this time is no different. Prices have more than doubled since the conflict began. The International Energy Agency says Europe is only weeks away from shortages.

Storing kerosene safely is very expensive, which is why airports don’t hold big jet-fuel reserves.

In addition, Europe’s reduced refining capacity leaves it acutely dependent on imports. And the ones that still operate can’t just turn up the dial. Kerosene comes from the same “middle part of the oil barrel” as diesel, so making more of one automatically means making less of the other. Similarly, making more gasoline reduces the amount of middle‑distillate material available for jet fuel and diesel. Refining is a complex process of compromises.

Airlines in parts of Asia have already cancelled flights or scrapped some of the least economical routes, and European carriers may have to start similar measures by late May.

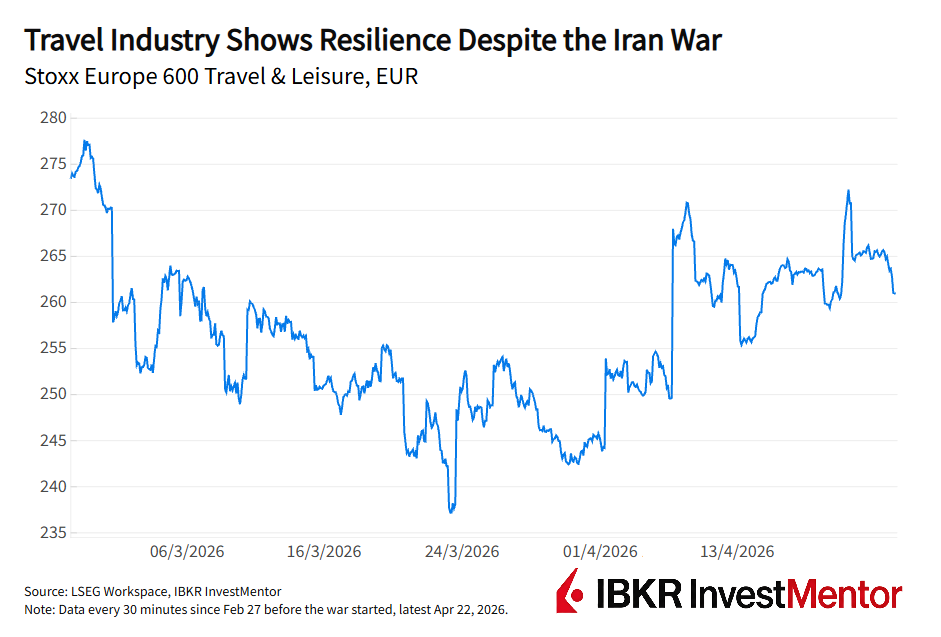

The timing is difficult. The summer travel season is crucial for airlines. And it’s not just holidaymakers that are hit. Air freight — which moves roughly a third of global trade by value — depends on steady kerosene supplies too. Travel stocks have proven surprisingly hardy in a crisis (and the wider stock market even more so), but pressures will mount as summer approaches.

Oil grabs attention, but the Hormuz disruption is hitting a list of other essentials, often by-products of oil and gas production in the region.

These are the building blocks of food systems, electronics, packaging, and healthcare. If the Strait of Hormuz continues to be disrupted for months or even years, the global economy will feel huge inflationary pressures. As the pandemic showed, supply chains will adjust but not as quickly as companies, consumers, and investors may wish.

Even if the Strait of Hormuz reopens, flows won’t normalize quickly. Shipping data from Kpler shows there are about 260 vessels laden with oil and LNG floating in the Gulf of Persia, waiting to exit.

If the ceasefire holds and Iran allows it, these ships could provide the world with around 170 million new barrels of oil and 1.2 million metric tons of LNG relatively quickly. But shipowners and insurers need security guarantees. And beyond that, the Gulf oil and gas infrastructure is badly damaged and could, in some instances, take years to fix.

The next few weeks will show how prepared countries really are. Europe faces a tight summer for fuel. Asia is already rationing. Airlines are adjusting schedules. Manufacturers are bracing for shortages of chemicals and gases they once assumed were always available.

The global economy relies on a handful of strategic corridors, and when one of them closes, the effects ripple through farms, factories, hospitals, and households, eventually reaching us all.

If you want to learn more about the commodity markets, download the free IBKR InvestMentor app: interactive lessons and fun, jargon-free explainers on everything finance-related.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

IBKR InvestMentorSM is a service of Interactive Academy LLC, an affiliate of IB LLC and majority-owned by IBG LLC. All content provided by IBKR InvestMentorSM is for informational and educational purposes only and should not be interpreted as implying any sponsorship, partnership, endorsement, recommendation, or approval by IB LLC or its affiliates.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!