- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 12, 2024 at 10:00 am

As the Q2 earnings season begins Wall Street Horizon hosts a Data Minds event on July 18 featuring industry experts, such as Steve Sosnick from Interactive Brokers, who will discuss dissecting data as global markets shift in the second half of 2024. Topics for discussion include: global H2 trading and risk outlook, how sector correlations can affect volatility, investor AI use cases, the latest trends in ETFs and more.

US markets have been rising in anticipation of Q2 earnings season which unofficially kicks off Friday with results from the big banks.

The good news is that earnings are expected to continue to be a bright spot through the second half of the year. What’s especially bullish as we enter the Q2 earnings season is the fact that Wall Street expectations have barely budged since the end of Q1. According to FactSet, S&P 500 EPS growth is anticipated to hit 8.8% for the second quarter. This is down just ever so slightly from the 9.0% expectation on March 31.1 This is pretty atypical as far as estimate revisions go. In response to more conservative corporate guidance, analysts tend to pull their estimates down by 3-4% in the weeks ahead of an earnings season. The fact that analysts mostly kept their estimates as is suggests that corporations believe they can surpass these expectations. If growth comes in at 8.8% it would be the highest growth rate in over two years, that’s with eight of the eleven sectors anticipated to show YoY increases.

On the flipside, however, while earnings growth is expected to be a highlight of the Q2 season, revenue estimates still remains a little light. Large corporations continue to cost cut their way to profit growth, which is a fine short-term solution, but soon investors will want to see a return to robust revenue growth driving earnings. Q2 revenue growth is expected to come in at 4.6%.2 Analysts have also barely touched that estimate, down from 4.7% expected on March 31, but it’s important to note that Q1 2024 saw a trend of more revenue misses than the historical average. In Q1 only 60% of S&P 500 names surpassed analyst expectations, well below the one, five and ten year average beat rate.3

In its usual fashion, Q2 earnings season will begin with the big banks, with JPMorgan Chase (JPM), Citigroup (C), and Wells Fargo (WFC), reporting on Friday. While these banks struck a bit of a cautious note in their Q1 reports, recent commentary has sounded a bit more upbeat.

While similar headwinds were still in play for Q2, investment banking showed signs of rebounding. Citigroup’s CFO Mark Mason recently spoke on the uptick of the investment banking business thanks to strong M&A activity,4 while Goldman Sachs (GS) President John Waldron noted that dealmaking was making a comeback thanks to investments in AI.5 Overall we noted 84 IPO announcements in Q2 2024, the strongest pace since Q3 2022 saw 112 such announcements. M&A announcements for the quarter totaled 98, just about with the prior three quarters, but otherwise a little light in the context of the last four years.

Investors seem to like the banks as well, given that stock prices rose steadily throughout the quarter. Of the six big banks, JPMorgan Chase has seen the largest gains YTD of 35%, followed by Citigroup at 25% and Goldman Sachs, Bank of America and Wells Fargo all just above the 20% mark. This is in comparison to the S&P 500 which is up around 18% on the year.

Source: Wall Street Horizon

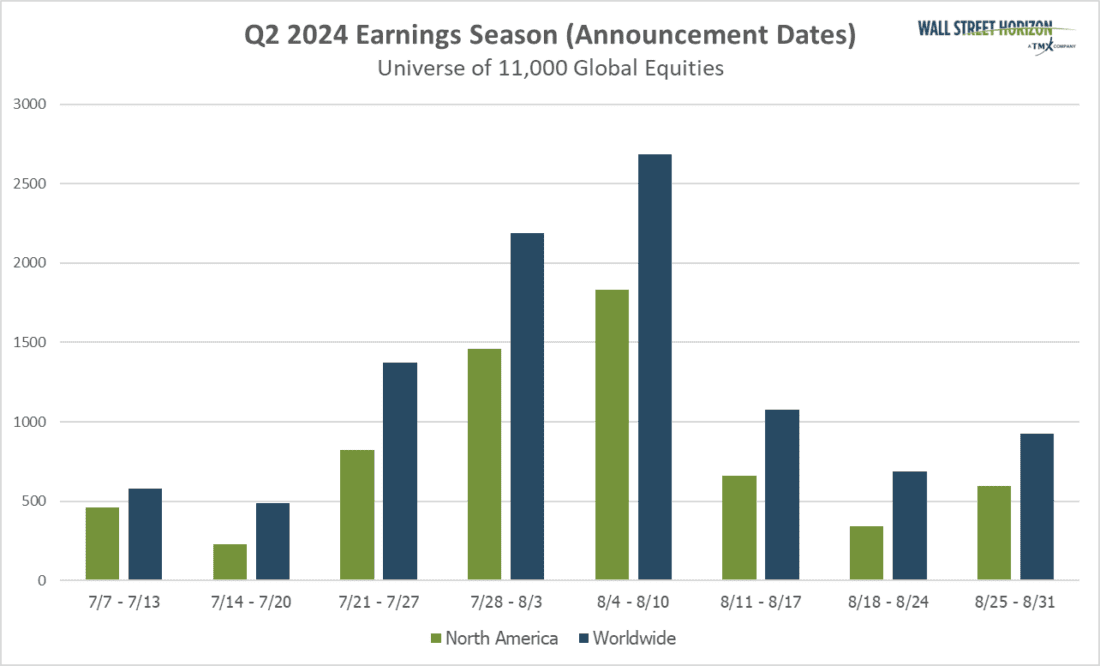

This season peak weeks will fall between July 22 – August 16, with each week expected to see over 1,000 reports. Currently August 8 is predicted to be the most active day with 1,445 companies anticipated to report. Thus far only 46% of companies have confirmed their earnings date (out of our universe of 10,000+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data.

Source: Wall Street Horizon

—

Originally Posted July 11, 2024 – Q2 Earnings Season Preview – The S&P 500 Breaks Records Ahead of Bank Reports

1 FactSet Earnings Insight, FactSet, John Butters, July 3, 2024, https://advantage.factset.com

2 FactSet Earnings Insight, FactSet, John Butters, July 3, 2024, https://advantage.factset.com

3 FactSet Earnings Insight, FactSet, John Butters, July 3, 2024, https://advantage.factset.com

4 “Citigroup CFO: Second Quarter Investment Banking Revenue up 50%,” Wall Street Journal, Justin Baer, June 18, 2024, https://www.wsj.com

5 “‘Our view is a soft landing is still the base case’: Goldman Sachs exec,” MarketWatch, Steven Gelsi, May 30, 2024, https://www.marketwatch.com

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Wall Street Horizon and is being posted with its permission. The views expressed in this material are solely those of the author and/or Wall Street Horizon and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!