- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 13, 2023 at 10:45 am

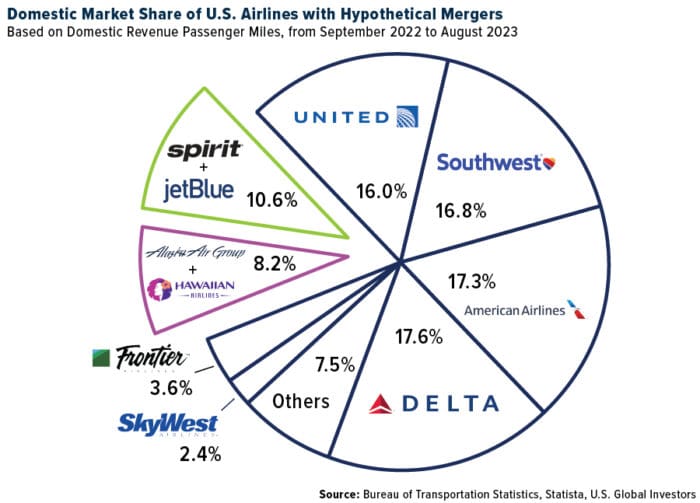

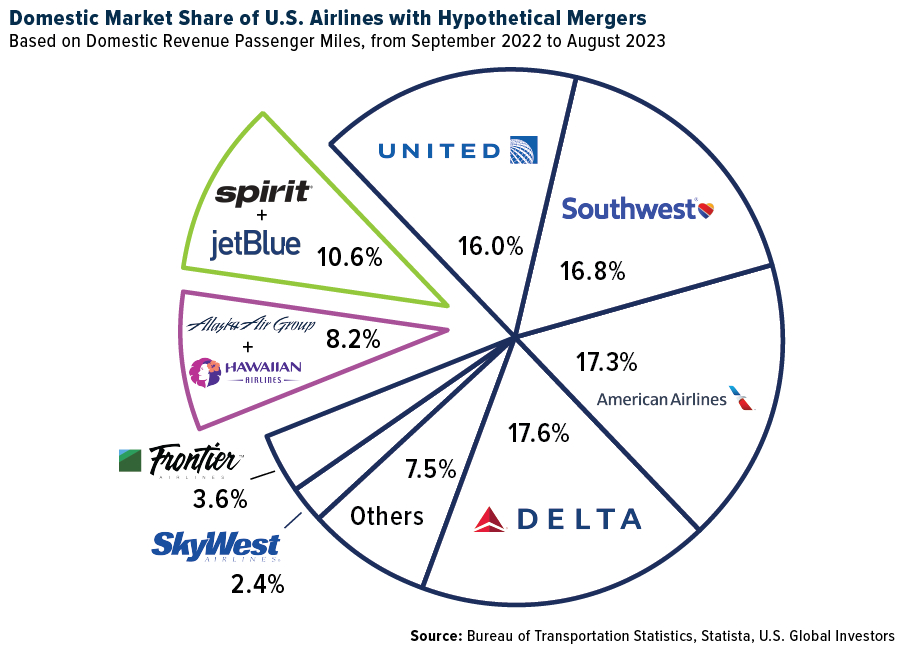

Airline consolidation is not only relatively common but necessary for growth and competitiveness, and the recent announcement of Alaska Airlines’ planned acquisition of Hawaiian Airlines is a prime example of this trend.

The move, valued at $1.9 billion, signifies more than just a business transaction. It represents a strategic positioning for future growth in a highly competitive, highly concentrated sector.

Once the deal is completed, Alaska and Hawaiian will have a combined market share of approximately 8.2%, making it the fifth-largest U.S. airline—unless JetBlue Airways succeeds in getting regulatory approval to acquire rival low-cost carrier Spirit Airlines. More on that later.

Alaska’ offer to purchase Hawaiian for $18 per share—today it’s trading around $13—includes taking on $900 million in debt, but the potential advantages are substantial. The Washington State-based carrier not only gains a significant foothold in the lucrative, $18 billion Hawaii market but also achieves several strategic benefits:

The announcement sent Hawaiian’s parent company shares soaring 193% last Monday, reflecting the market’s optimistic view of the deal. This positive reaction underscores a broader trend in the airline industry, where smaller players seek mergers to stay competitive against larger rivals.

Parallel to the Alaska-Hawaiian deal, JetBlue officially wrapped its case in federal court last week to acquire Spirit for $3.8 billion. If approved, the deal would reshape the U.S. airline industry, potentially challenging the dominance of the four major carriers and marking the most significant instance of airline consolidation since the American-US Airways merger in 2013.

According to Evercore ISI’s Duane Pfennigwerth, who was present for closing arguments on Wednesday, the judge’s line of questioning “read favorably for a settlement,” and JetBlue appeared to have “a more cohesive argument [than the Justice Department], which required less clarification by the judge.”

Among the most compelling arguments made by JetBlue attorneys is that the New York-based carrier requires scale to grow and compete against the Big Four airlines. Smaller competitors are expected to fill the gaps created by an outgoing Spirit, which JetBlue insists can’t make it alone in the current marketplace anyway.

The Justice Department is not so sure. The agency claimed that a JetBlue-Spirit merger would wipe out half of all ultra-low-cost carrier (ULLC) capacity in the U.S., depended on by many price-conscious Americans. Further, “Spirit anchors pricing in larger markets and is an innovator, with self-service bag drops an example of a recent innovation,” writes Pfennigwerth, summarizing the Justice Department’s line of reasoning.

A decision is expected as early as this week.

Domestic airline stocks rallied last week on the positive news, with the NYSE Arca Airlines Index closing up nearly 13% from the previous Friday. This represents the largest weekly gain for the group since November 2020.

Taking time from its court case in Boston, JetBlue raised its financial outlook for 2023, with expected annual revenue growth of 4% to 5%, up from earlier guidance of 3% to 5%, and a smaller-than-anticipated adjusted loss. This uplift is buoyed by strong bookings and operational performance.

Delta Air Lines reported robust holiday travel demand and increasing corporate bookings, projecting a bright end to 2023 and solid beginning to 2024. Speaking at the Morgan Stanley Global Consumer & Retail Conference, Delta CEO Ed Bastian doubled down on the carrier’s positive 2023 guidance, citing record revenues for the Thanksgiving holiday. Christmas bookings look to be “very, very strong,” Bastian said.

During his presentation, Bastian shared an interesting chart that shows that air travel as a percent of gross domestic product (GDP) has returned to the long-term average. Since 1980, soon after deregulation, commercial air travel expenditure has historically averaged around 1.3% of the U.S. economy, with notable deviations occurring as a result of 9/11 and the 2009 financial crisis. However, the most significant disruption was during the pandemic, resulting in approximately $300 billion of lost demand from 2020 to 2022.

The recent travel boom, Bastian pointed out, is a response to pent-up demand, though it’s only brought the industry back to the 1.3% average without addressing the missing $300 billion gap. Bastian expects to recoup this amount over the next few years as demand remains near or above present levels.

On a final, encouraging note, the International Air Transport Association (IATA) forecasts net profits of $25.7 billion for the global airline industry in 2024, with operating profits reaching a record $49.3 billion. North American carriers, which were first to return to profitability in 2022, are set to collect a combined $14.4 billion in profits, the IATA says.

This projection, coupled with an expected surge in passenger traffic, paints a picture of an industry on the cusp of a historic rebound.

The airline industry’s journey through the pandemic was fraught with challenges, but its rapid return to profitability is a testament to its resilience and adaptability. As the Alaska-Hawaiian and JetBlue-Spirit deals take shape, it’s clear that the industry is not just recovering but is actively reshaping itself for a new era of growth and competition.

—

Originally Posted December 11, 2023 – Global Airline Industry Forecast To Generate Record Operating Profit In 2024

The NYSE Arca Airline Index is an equal-dollar weighted index of the most highly capitalized companies in the airline industry.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2023): JetBlue Airways Corp., United Airlines Holdings Inc., Alaska Air Group Inc., Hawaiian Holdings Inc., Southwest Airlines Co., American Airlines Group Inc., Delta Air Lines Inc., SkyWest Inc., Frontier Group Holdings Inc.

All opinions expressed and data provided are subject to change without notice. Holdings may change daily.

Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

About U.S. Global Investors, Inc. – U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by clicking here or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from US Global Investors and is being posted with its permission. The views expressed in this material are solely those of the author and/or US Global Investors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!