- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 15, 2023 at 12:15 pm

DBS Group Holdings (“DBS”), Oversea-Chinese Banking Corp (“OCBC”) and United Overseas Bank (“UOB”) have averaged 32% total returns since the end of 2019, bringing their 10-year annualised total returns to 7.5% as of 12 May.

For the 2023 year through to 12 May, the trio averaged 3.0% declines in total return, following 13.1% average total returns in 2022. Since the end of 2019, the trio have ranked fourth, seventh and tenth in current STI constituent highest returns since the end of 2019.

| Company Name | Code | Mkt Cap (S$M) | 12 May Close | Pct Chg MTD % | Pct Chg YTD % | TR YTD % | 5 Year Total Return % | 52W H | 52W L | P/B (x) | Beta |

| DBS Group Holdings | D05 | 79,736 | 30.66 | -6.6 | -9.6 | -5.8 | 33.0 | 36.40 | 29.45 | 1.39 | 1.34 |

| Oversea-Chinese Banking Corporation | O39 | 55,586 | 12.25 | -2.6 | 0.6 | 3.9 | 18.1 | 13.23 | 11.20 | 1.04 | 1.13 |

| United Overseas Bank | U11 | 47,054 | 27.77 | -1.6 | -9.5 | -7.1 | 17.4 | 31.40 | 25.91 | 1.07 | 1.22 |

Source: Refinitiv (Data as of 12 May 2023)

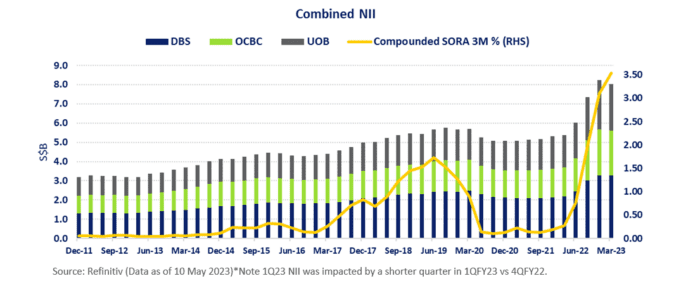

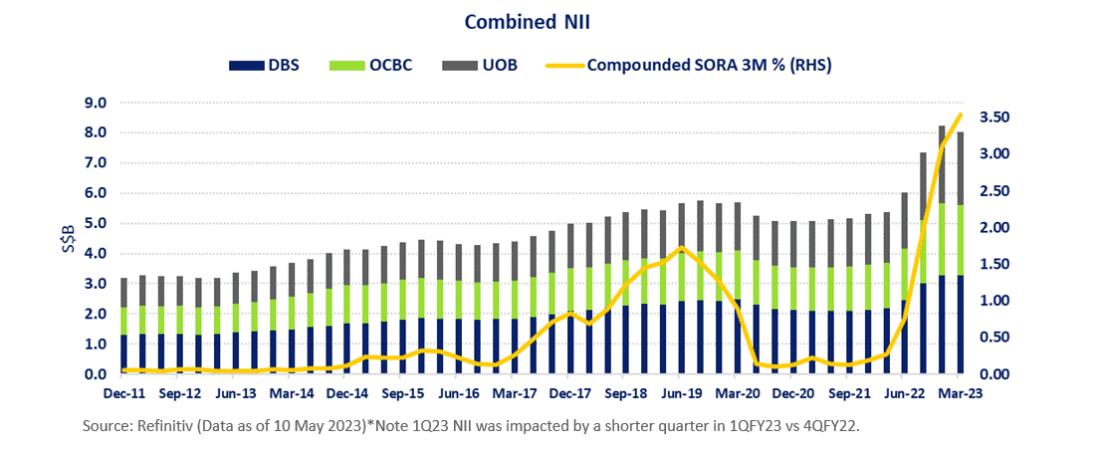

The trio of STI banks reported record quarterly profit for 1QFY23, supported by Net Interest income (“NII”) growth.

At S$11.8 billion, the combined Total Income of the trio was up 36% YoY and up 8% QoQ. As much as 68% of the combined 1QFY23 Total Income of the trio was attributed to NII. Combined NII for the trio in 1QFY23 was S$8.0 billion. This was up from S$5.4 billion in 1QFY22 and down from S$8.2 billion in 4QFY22, and impacted by a short quarter in 1QFY23 vs 4QFY22. As illustrated below, prior to 1QFY23, the three banks had reported nine consecutive quarters of combined QoQ NII growth.

The YoY growth in NII corresponded with rising Net Interest Margins (“NIMs”) which pressed higher with global interest rates. In the results briefing, DBS maintained its NIMs likely peaked in 1QFY23, and looking forward the NIM decline is likely to be gradual, with its FY23 NIM expected at 2.05-2.10%. OCBC maintained its FY23 NIM target was in the region of 2.2%, while UOB’s business update foresaw its margins to hold up, at current levels.

NII is also driven by loan growth. FY23 loan growth guidance is currently 3-5% for DBS, and similarly low-to-mid single percentages for OCBC and UOB. At the same time, Non-Performing Loans (“NPL”) as percentage of total loans improved marginally for OCBC in 1QFY23 to 1.1% from 1.2% in 4QFY22, while remaining at 4QFY22 levels of 1.1% for DBS and 1.6% for UOB.

Loan growth of the trio in FY22 outpaced the 1.4% growth recorded by the Finance & Insurance component of Singapore’s GDP in 2022. As maintained by MAS business loan data, the biggest segment within local business loans is building and construction, while housing loans make up around 70% of overall consumer lending. Earlier this year, DBS maintained it continued to have the lion’s share of CASA deposits in Singapore, with its market share rising 0.7 percentage points in 2022 to slightly more than 53%.

Non-Interest Income (“NOII”) comprised the remaining 32% of the trio’s 1QFY23 combined Total Income. On a QoQ basis, DBS, OCBC and UOB reported respective NOII growth of 27%, 65% and 45%. iFAST Corporation also reported that while its 1QFY23 Assets under Administration (“AUA”) declined 2.6% from 1QFY22, the AUA increased 4.2% from 4QFY22.

OCBC noted that its QoQ rise in Assets Under Management was driven by continued net new money inflows and positive market valuation. DBS noted it expects double digit fee growth and UOB expects high single digit fee growth in FY23, with DBS noting fee income was up YoY in Feb and March, reversing year-long declines with “wealth management and investment banking recovering and the “pace of growth dependent on market conditions”. UOB also noted that QoQ, wealth management fees rebounded strongly from improved investor sentiments.

The percent of total income segmented to Singapore in FY22 was 65% for DBS, 58% for OCBC and 57% for UOB. UOB has completed the acquisition of Citi’s Wealth Management business in Thailand, Malaysia, and Vietnam, and expected to complete the Indonesia acquisition by year end.

DBS is targeting a S$1.68 per share dividend for its FY23, barring unforeseen circumstances, after paying S$2.00 per share in FY22. Dividends distributions for FY22 translated to S$5.1 billion for DBS, S$3.1 billion for OCBC and S$2.3 billion for UOB.

According to Bloomberg data, the trio of DBS, OCBC and UOB maintain annualised Return on Common Equity ratios above the median ROE for the top quartile of global banks by market value.

For 1QFY23, UOB maintained a 14.9% core ROE with OCBC’s ROE at 14.7% while DBS highlighted that its ROE for 1Q23 was a record high at 18.6%. DBS has previously noted its high ROE is on the back of digital transformation, after laying out a “thesis that digitalisation would enable it to increase wallet share with lower marginal cost” in 2017.

As DBS announced on 5 May, MAS supervisory action following the recent digital disruption requires DBS to set aside additional capital amounting to 1.8x of its risk weighted assets (RWA) for operational risk. This brings its Common Equity Tier CET–1 ratio down from 14.4% to 14.1%, which is still above its 12.5% to 13.5% target range. DBS also noted in the 1QFY23 media briefing that a special board committee has been established to oversee the investigation on the digital outage in March, and DBS has also engaged external experts with deep experience in overseeing large-scale IT systems and operations to work with the committee.

As relayed in the FY22 Annual Report, DBS is focused on leveraging digital technology to reimagine banking to provide its customers a full range of services in consumer banking, wealth management and institutional banking.

From 9 March through to 12 May, the trio of DBS, OCBC and UOB averaged a 2.2% decline in total return, which was significantly more defensive that the 8% decline for the Dow Jones US Large Cap Banks Index, which in turn was also significantly more defensive than the 24% decline for the S&P Bank Select Industry Index and 32% total decline S&P Regional Banks Select industry Index. Performances of US stocks have a significant impact on the performance of the global stock market, with the US accounting for close to 60% of the weight of the FTSE All-World Index.

March FOMC Minutes revealed that that it was US regional banks with unusually large reliance on uninsured deposits and holdings of securities with significant unrealised mark-to-market losses that had experienced larger declines in stock prices. The May FOMC Minutes due are 25 May.

As the DBS CEO noted in the 1QFY23 media briefing dollar liquidity is still quite ample, adding that he saw the fundamental challenges of the US banking crisis relating to interest rate risk management, such as long durations of bond books.

While the most recent FOMC saw the Fed Chair signal that a pause to the US rate cycle was imminent, he could not signal cuts nor could he afford to signal a peak as the “persistent” aspect of the US inflation gauges remain a key concern for the FOMC, with the US PCE Core Deflator rangebound between 4.3% and 5.3% for the past 18 months and coming in at 4.6% for March. Expectations for a pause at the upcoming 14 June FOMC are at now around 90%.

The focus on interest rates has seen the trio of DBS, OCBC and UOB make up between 25 to 30 cents in every dollar that has gone to work in the Singapore stock market each day in 2022 and the 2023 year to 10 May, up from 20 cents in the dollar in 2021 and 2020.

The trio also maintain a combined 4% weightage in the FTSE Developed Asia Pacific ex Japan Index, with the weightage increasing by more than 2.5 times to 10% in the FTSE Developed Asia Pacific ex Japan Sustainable Yield Index. The FTSE Global Sustainable Yield Index Series excludes extreme yielding stocks and examines the financial and operating strength of prospective constituents (including profitability, capital structure and operation efficiency, with specific emphasis on companies with strong balance sheets and the ability to generate cash flow.

Shorter-term trading activity also increased in relevant portfolio products in recent months. Daily Leverage Certificates (“DLCs”) and Structured Warrants are financial instruments issued by a third-party financial institution, usually investment banks, and are traded in the SGX securities market. The combined turnover for DLCs based on UOB and OCBC was on average 37% higher in April as compared to January, with the majority of the trading activity in Long DLCs as the share prices of both stocks spent half the month consolidating in comparatively tight trading ranges. Combined turnover for Structured Warrants on the trio of banks also reached close to S$50 million over the first four months of the year, up 24% for the first four months of 2022, with DBS and UOB ranking among the top-traded Structured Warrants on companies from February through April. Note individual investors need to be Specified Investment Products (SIP) qualified to trade DLCs and Structured Warrants.

—

Originally Posted May 15, 2023 – DBS, OCBC & UOB Report Record Quarterly Net Profits

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Singapore Exchange and is being posted with its permission. The views expressed in this material are solely those of the author and/or Singapore Exchange and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!