- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 18, 2024 at 11:15 am

Yesterday, we made an assertion that protective puts are relatively cheap right now. Today we intend to prove it.

Specifically, we wrote the following for those who are concerned that the current momentum-driven rally is getting long in the tooth:

One strategy involves a barbell – keep buying the tech-heavy indices but utilizing put options as insurance. Remember, when we buy insurance, we don’t WANT it to pay off. And considering that volatility is relatively low right now, the insurance is relatively cheap.

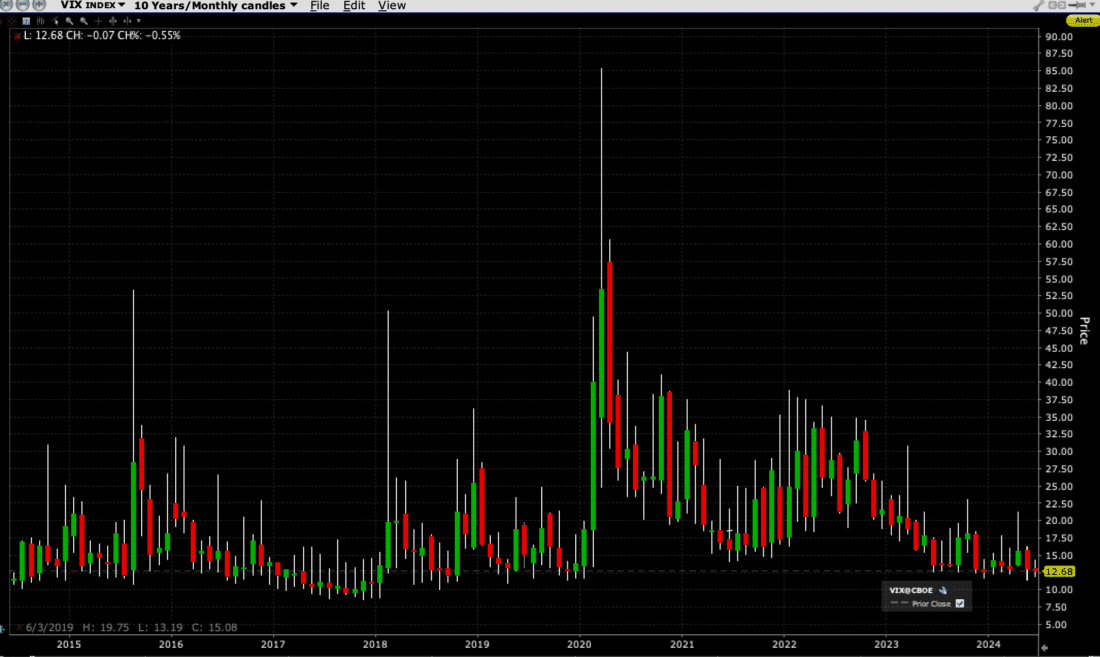

An obvious way to back up that assertion is to point out that the Cboe Volatility Index (VIX) is near multi-year lows, as evidenced by the chart below:

Source: Interactive Brokers

We see that VIX has not been consistently this low since before 2020’s covid crisis. Remember that even as the virus was spreading around the world, US markets were slow to react. On February 14th of that year, when VIX closed at 13.68, we wrote a piece entitled Confessions of a Market Nihilist. The theme was that traders were so enamored of the Federal Reserve’s expanding balance sheet, triggered by a repo funding crisis the prior autumn, that they were willfully blind to the rising risks around them. Although we are not facing anything close to that sort of existential crisis – at least not as far as I can see – I do find the agglomeration of important market divergences to be a source of concern.

And heck, VIX is not in the single digits, as it was before the “Volmageddon” of February 2018…

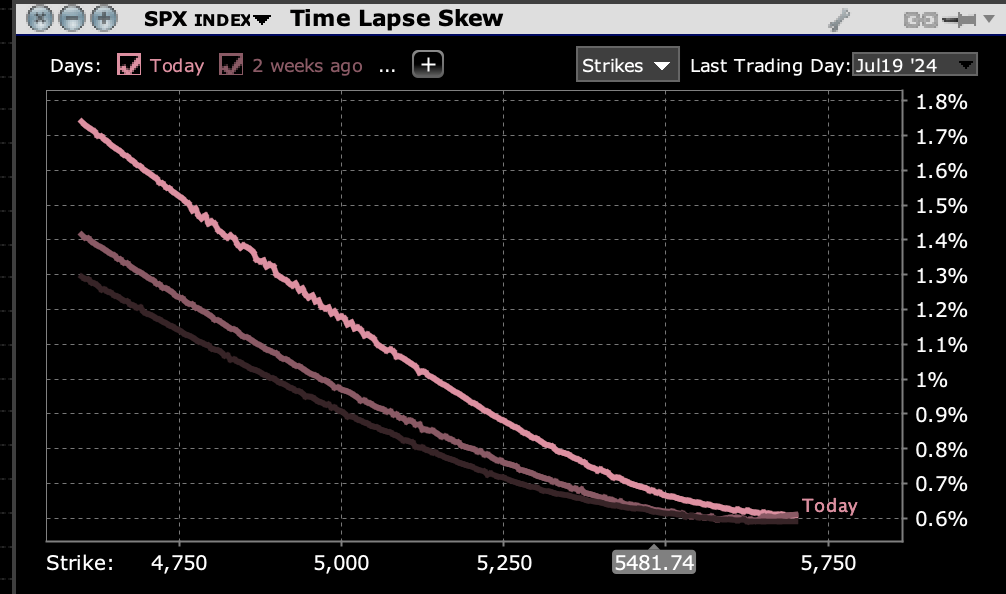

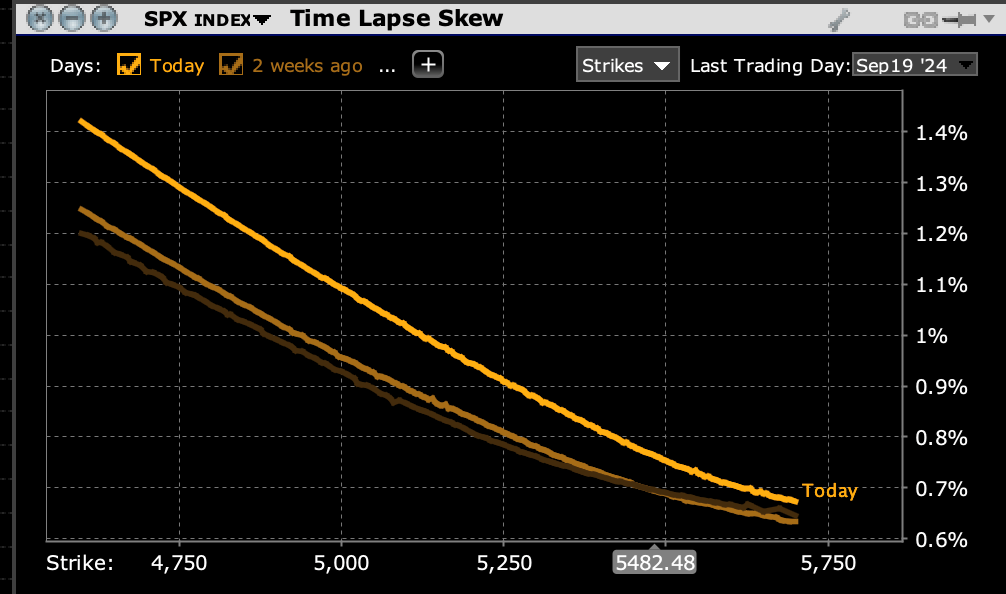

But VIX is a bit of a blunt instrument. Its calculation utilizes all S&P 500 (SPX) index options with 23 to 37 days to expiration with non-zero bids. That means that options above AND below the current market are included. But when we’re hedging downside, only below-market options are relevant.

When we look at SPX skews for options expiring in one and three months over the past four weeks, it does appear that at least some options traders are becoming more concerned with hedging the current advance:

Source: Interactive Brokers

Source: Interactive Brokers

We can see that implied volatilities across the curves have risen in recent days, but the rise is most pronounced in below market options. Someone has been bidding for puts.

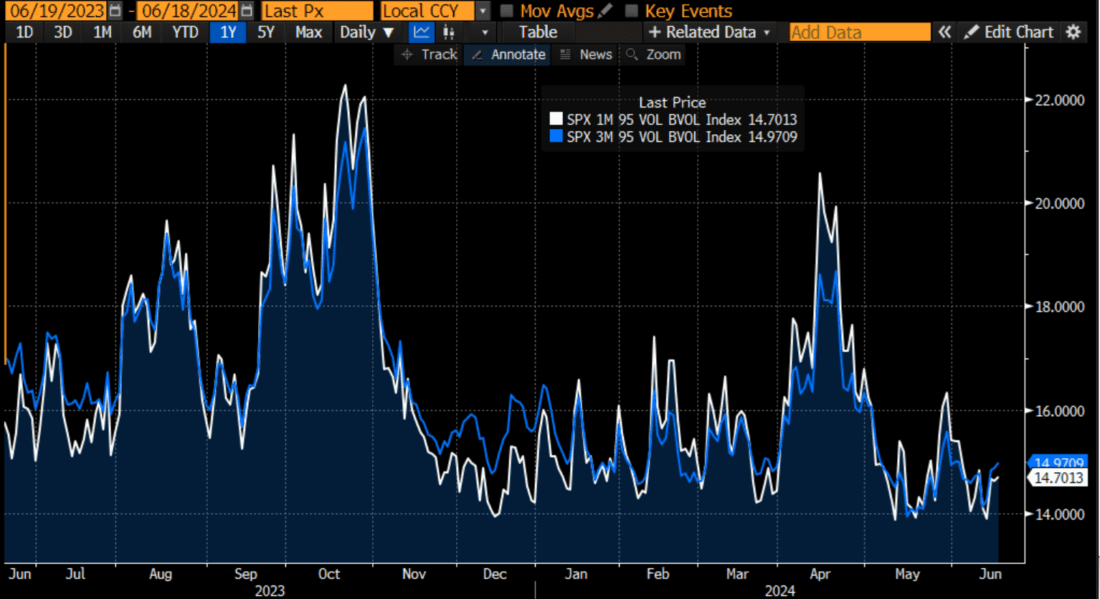

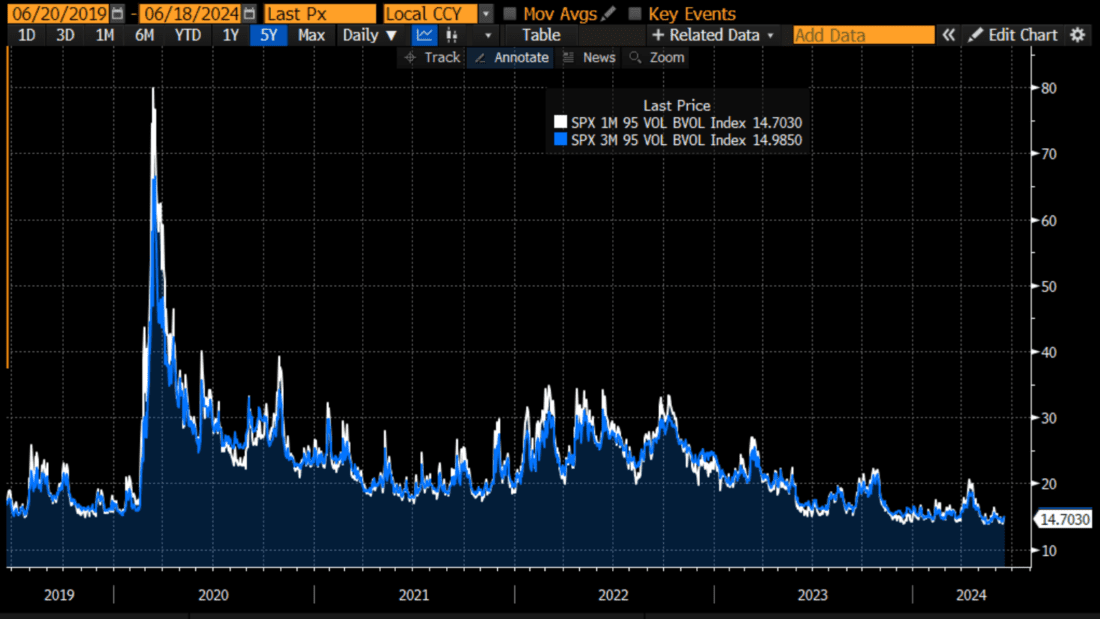

That said, when we look at specific options from a moneyness viewpoint, the rise is relatively minor. Below are charts for 1-month and 3-month SPX options with constant 95% and 90% moneyness (meaning 5% and 10% below the then-current index level). We chose those levels because they are reasonable ways to hedge a pullback or a correction. While they could protect against a sharper decline, these are not “disaster” puts.

Source: Bloomberg

Source: Bloomberg

While these implied volatilities are off their lows, they are still among the lowest levels we’ve seen over the past year. When we look over a five-year horizon, we see that these are also among the post-covid lows:

Source: Bloomberg

Source: Bloomberg

Hedge the current rally if you’d like. Or not. It’s up to you. But if you do choose to hedge, it’s clearly not a historically expensive time to do so.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

This is great, and I’m an experienced option trader for 20 years, but unless I missed it you didn’t exactly say what to do. Presumably, buy SPX or SPY puts out 3 months, or long the VIX.

Yeah I took this as “it’s cheap to pick up index puts right now”.

Hello Preston, IBKR does not provide investment advice.