- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 22, 2025 at 10:15 am

Power generation demand from artificial intelligence (AI) and data center computing could benefit the midstream sector.

Major companies are making substantial investments to meet the rising demand for natural gas needed for power generation.

Natural gas demand visibility can help midstream companies plan better and reduce risk and enhance project execution.

Natural gas demand growth is now potentially approaching 25%–34% by 2030.1 That means that our previous expectations about natural gas demand appear conservative. (Read: Midstream Energy to Fuel Growth in AI.). Driven by the expected increase in demand for power generation from artificial intelligence (AI) and data center computing, the growing demand for natural gas could benefit the midstream sector. Plus, there are other tailwinds for the sector. Supportive macro trends combined with continued capital discipline have benefited project returns within the midstream sector, meaning that capital spending today may benefit investors more now than in the past.

Estimates for natural gas demand growth have been increasing. For example, Bernstein now forecasts data center-linked natural gas demand growth of 12 billion cubic feet per day (bcf/d) over that same timeframe.2,3

These robust estimates are starting to match with real-world action.

While it is still too early to confidently predict how large data center-linked natural gas demand will be, it appears clear to us that the volume will be material. This emerging source of demand is in addition to the significant and predictable demand growth underway from the completion of numerous liquified natural gas (LNG) export facilities and continued industrial demand growth.

In total, these trends could lead to 28–37 bcf/d of additional demand by 2030, which is a 25%–34% increase.1 While natural gas demand has experienced steady growth historically, rarely have the drivers of demand been as visible.

This visibility is significant for the midstream sector, in our view. It allows midstream companies to plan to meet this demand with greater certainty and foresight. That’s why we believe today’s projects can be more efficiently executed and carry fundamentally less risk.

The midstream infrastructure buildout that supported the emergence of the US shale basins over the previous two decades was colossal. Thousands of miles of pipelines, as well as enormous processing, treating, fractionation, and storage capacity additions, were built. Recent and future capacity expansions are often able to leverage existing assets in a more efficient manner. For example, annual capital expenditure (capex) for the 29 largest midstream companies in 2026 is expected to be roughly equal to the amount spent in 2023.8 In 2023, data center-driven demand had not yet been recognized, and earnings before interest, taxes, depreciation, or amortization (EBITDA) for those same 29 companies was 32% lower.

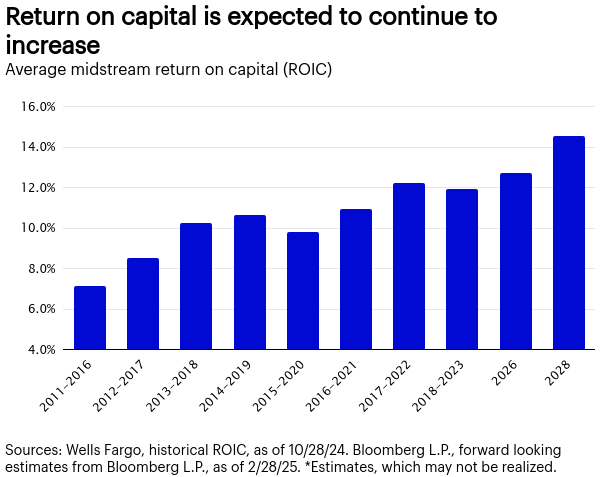

One measure of capital efficiency is return on invested capital (ROIC), which is calculated as EBITDA or net operating profit after tax (NOPAT) divided by total capital invested. From 2015 through 2023, the average ROIC for the midstream sector rose from 9.8% to 11.9%.9 This trend is expected to continue with average ROIC expected to rise to 12.7% in 2026 and 14.5% in 2028.8 This improvement in capital efficiency, combined with the sector’s ability to largely fund growth projects through internally generated cash flows and without issuing new dilutive equity, means that investors may benefit more from today’s capital investments than in past periods.

The midstream sector offers investors an attractive distribution yield and an improving outlook for cash flow and distribution growth, in our view. These fundamentals are supported by significant and predictable natural gas volume growth and improving returns on invested capital. Roughly 75% of the sector is natural gas production focused.8 With natural gas demand potentially growing 25%–34% by the end of the decade, increasing capital efficiency, and healthy balance sheets, we believe the midstream sector is a compelling asset class with macro driven tailwinds.1

—

Originally Posted on April 21, 2025

Midstream growth outlook: Increasing natural gas demand by Invesco US

Footnotes

The Alerian MLP Index is a capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority oftheir cash flow from midstream activities involving energy commodities.

An investment cannot be made into an index. Past performance does not guarantee future results.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions, there can beno assurance that actual results will not differ materially from expectations.

Most MLPs operate in the energy sector and are subject to the risks generally applicable to companies in that sector, including commodity pricing risk, supply and demand risk, depletion risk and exploration risk. MLPs are also subject the risk that regulatory or legislative changes could eliminate the tax benefits enjoyed by MLPs which could have a negative impact on the after-tax income available for distribution by the MLPs and/or the value of the portfolio’s investments. Although the characteristics of MLPs closely resemble a traditional limited partnership, a major difference is that MLPs may trade on a public exchange or in the over-the-counter market. Although this provides a certainamount of liquidity, MLP interests may be less liquid and subject to more abrupt or erratic price movements than conventional publicly traded securities. The risks of investing in an MLP are similar tothose of investing in a partnership and include more flexible governance structures, which could result in less protection for investors than investments in a corporation. MLPs are generally considered interest-rate sensitiveinvestments. During periods of interest rate volatility, these investments may not provide attractive returns.

Energy infrastructure MLPs are subject to a variety of industry specific risk factors that may adversely affect their business or operations, including those due to commodity production, volumes, commodity prices, weather conditions, terrorist attacks, etc. They are also subject to significant federal, state and local government regulation.

The opinions referenced above are those of the author as of March 24, 2025. These comments should not be construed asrecommendations, but as an illustration of broader themes. The opinions are based on current market conditions and are subject to change. They may differ from these of other Invesco investment professionals.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED

MAY LOSE VALUE

NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds. Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2024 Invesco Ltd. All rights reserved.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Invesco US and is being posted with its permission. The views expressed in this material are solely those of the author and/or Invesco US and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!