- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 26, 2021 at 11:45 am

With the Turkish lira reaching new historic lows, we assess the possible policy solutions to stabilise the currency.

The plight of the Turkish lira is back in the headlines this week. The currency sank by 15% against the US dollar at one point on Tuesday to reach a fresh historic low of almost 13.50 to the US dollar. Despite a modest rebound since, the lira has depreciated by close to 40% so far this year, as at 24 November, leaving it firmly at the bottom of the performance charts.

Market participants in Turkey are well accustomed to periodic sharp sell-offs in the currency. The country has effectively been playing a long-running game of cat and mouse between its structurally poor balance of payments, political pressure to lower interest rates, and investors’ willingness to fund deficits. Indeed, the markets went through a similar experience earlier this year after central bank governor Naci Agbal was sacked and replaced with government-ally, Şahap Kavcıoğlu.

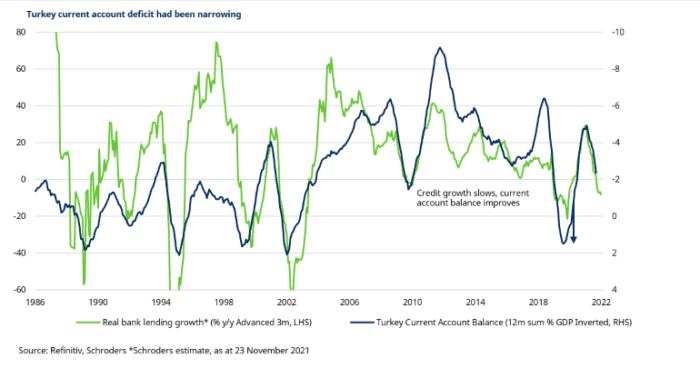

The lira’s fundamentals had actually been looking relatively ok. Monthly current account readings had been springing positive surprises while a deceleration in real credit growth suggested that the trend would continue for a while longer.

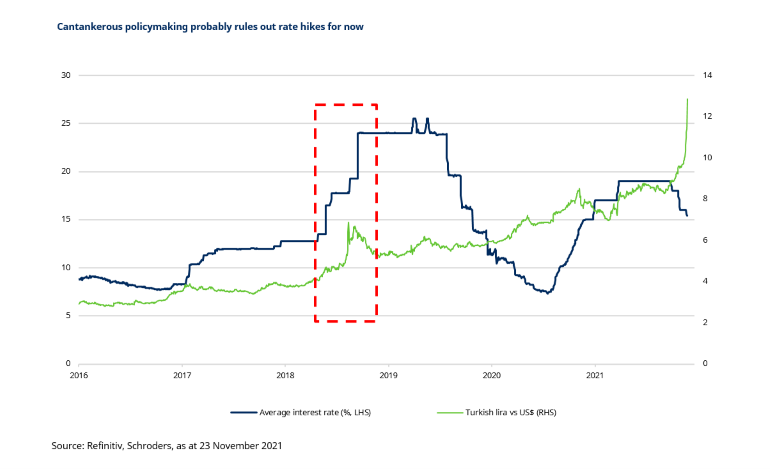

However, all of that was thrown out of the window once political pressure ultimately forced the central bank to begin lowering interest rates in September. The policy rate has already been cut by a total of 400bps, taking it negative in real terms, while President Erdogan’s declaration on Tuesday of an “economic war of independence” implied that more unorthodox policy is on the way.

Such exponential sell-offs have in the past often required aggressive interest rate hikes in order to protect the capital account, stem outflows, and stabilise the currency.

For example, in 2018 a succession of rate hikes totalling more than 1000bps were ultimately required to bring a similar sell-off to an end.

However, President Erdogan’s comments appear to rule out what would amount to a major U-turn in central bank policy. At least, until or unless market conditions get even worse. Further pressure on the currency may well materialise. Even so, very large interest rate hikes in excess of those seen in 2018 would probably be required for the market to gloss over the latest heavy blow to the central bank’s credibility.

For the time being, that leaves two options: let the currency go, or impose capital controls to prevent further depreciation. Much will probably depend on just how much more pressure the currency and local banks’ holdings of foreign exchange come under.

There have now been at least a couple of periods, in 2018 and during the Covid crisis last year, where question marks have been raised about the convertibility of the lira. The authorities imposed restrictions on access for foreign banks to the lira market, and the ability of locals to exchange lira for foreign exchange.

We would not be surprised to see these measures imposed again as the government attempts to ride out the storm. And while outright capital controls would be self-defeating in the long run, and therefore unlikely, the steady deterioration in policymaking makes the threat greater than in the past.

In short, no.

The current problems in Turkey are very much self-inflicted, as opposed to a sign of structural problems elsewhere. Indeed, virtually all other EM central banks are busy hiking rates to rein in inflation, potentially setting up opportunities next year.

—

Originally Posted on November 25, 2021 – What Is Needed to Support The Turkish Lira?

The views and opinions contained herein are those of Schroders’ investment teams and/or Economics Group, and do not necessarily represent Schroder Investment Management North America Inc.’s house views. These views are subject to change. This information is intended to be for information purposes only and it is not intended as promotional material in any respect.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Spot currencies are not available at IBKR Singapore.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!