- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 24, 2024 at 11:00 am

Equities are rebounding from yesterday’s selloff with this morning’s downwardly revised inflation expectations from the University of Michigan supporting investor optimism. Headline consumer sentiment for this month, meanwhile, was revised upward, which together with lighter price pressure projections is providing fuel to the soft-landing trade. Additionally, durable goods figures, released earlier in the morning, provided yet another signal of the manufacturing sector’s comeback following yesterday’s sizable PMI beats.

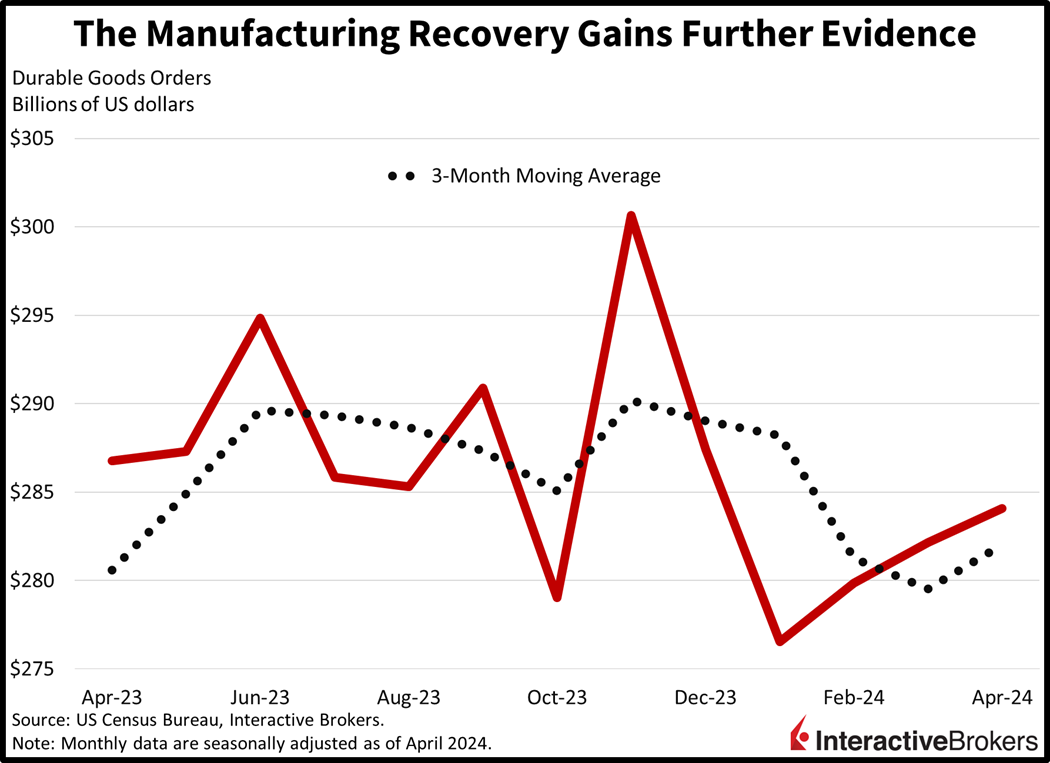

Durable goods orders grew for the third consecutive month in April, according to this morning’s US Census Bureau publication. Last month’s durable goods purchases rose 0.7% month-over-month (m/m) despite forecasters anticipating a decline of 0.8%. April’s growth decelerated slightly from 0.8% in March, however. In April, transactions were supported by most segments with computers, communications equipment, defense aircraft, automobiles and primary metals sporting m/m progress of 3.9%, 3.3%, 2.5%, 1.5% and 1.3%. The electric equipment, machinery and fabricated metal products categories saw softer momentum, with sales rising less than 1% m/m. Dampening some of the gains were the passenger aircraft and other segments, with declines of 8% and 0.2%. Nondefense capital goods excluding aircraft, an indicator of corporate capital expenditures, increased 0.3% m/m, recovering from March’s 0.1% decline.

In a separate University of Michigan report, this month’s consumer sentiment headline figure was revised from the 67.1 level reported on May 10 to 69.1, while 1- and 5-year inflation expectations were adjusted downward from 3.5% and 3.1%, respectively, to 3.3% and 3%.

During the recent quarter, strong footwear brands produced encouraging results for Decker Brands and off-price retailing supported revenue of Ross Stores. A slowdown in hiring, however, is weighing on the performance of Workday, while weak box office sales were a headwind for Lionsgate. The following are highlights from the companies’ recent earnings reports:

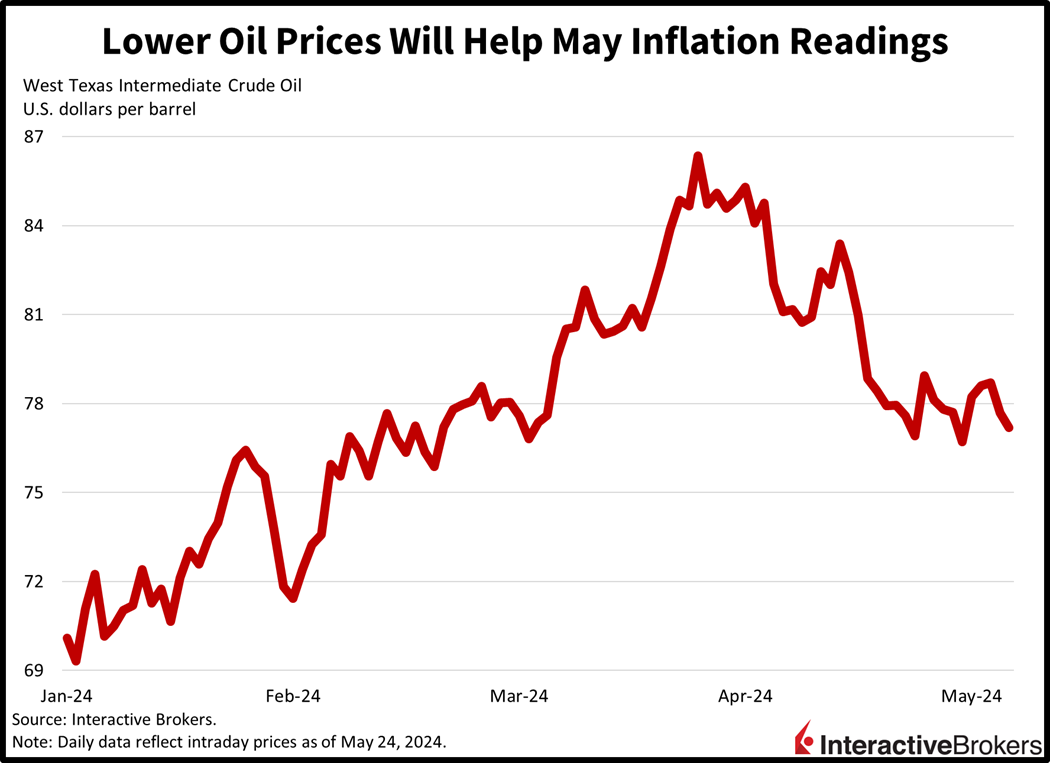

Stocks are recuperating from yesterday’s bruising while the dollar travels south and yields are near the flatline. All major US equity indices are higher with the Russell 2000 and Nasdaq Composite benchmarks leading; they’re up 1.2% and 1%. The S&P 500 and Dow Jones Industrial gauges are increasing at more tempered rates of 0.8% and 0.4%. Sectoral breadth is green—every sector is up. Communication services, utilities and consumer discretionary are leading the pack; they’re up 1.4%, 1.4% and 1.2%. The 2- and 10-year Treasury maturities are changing hands at 4.94% and 4.47% while the Dollar Index depreciates by 34 basis points. The greenback is losing ground relative to the euro, pound sterling, franc and Aussie and Canadian dollars. It is up versus the yen and yuan, however. Things are relatively quiet in commodity land, with gold up 0.3%, copper unchanged and crude oil bouncing off a 3-month low with WTI trading at $77.09 per barrel, 0.5%, or $0.35 loftier in trading so far.

Market trading volumes are light today as we gear up for the long weekend and the unofficial start of summer. Across the country, civic leaders and organizations will hold events to honor and remember those brave individuals who were lost in military conflicts. In closing, we hope the three-day weekend will be a restful respite from the daily grind of work and more importantly, a time for meaningful reflection regarding fellow Americans lost in battle.

Visit Traders’ Academy to Learn More About Durable Goods and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Hard to consider favorable consumer sentiment when real companies such as Starbucks, targets, dicks, VF, home Depot, McDonald’s, and all those other retailers, all have reported poor numbers. Add in the rise and gasoline even though oil has fallen. Where do you get a consumer that’s happy?

Could not agree more, savings at 30-40 year lows, credit card debt at historic highs, defaults and delinquencies increasing, joe getting ready to raid the strategic oil reserves again, can’t buy a house or a car because of interest rates. I do not believe the revised economic data, ever. Additionally, reports of employment always fail to report that openings are part time and continuing claims are high.