- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 24, 2024 at 11:30 am

The new day has brought fresh probabilities for this year’s presidential election, which are strikingly different from yesterday’s prospects, as several polls reflect near coin-flip odds for the two top candidates. At first glance, many would have expected the Harris trade to gain steam, but as big-tech earnings hit the tape, we’re getting quite the opposite. Risk-off sentiments are indeed dominating Wall Street, with investors dumping high-growth tech stocks and almost everything else in favor of Treasury bills, gold bars and Swiss francs. Rates are certainly plunging with weak new home sales stateside and softer-than-expected flash PMIs on both ends of the Atlantic weighing on the economic outlook.

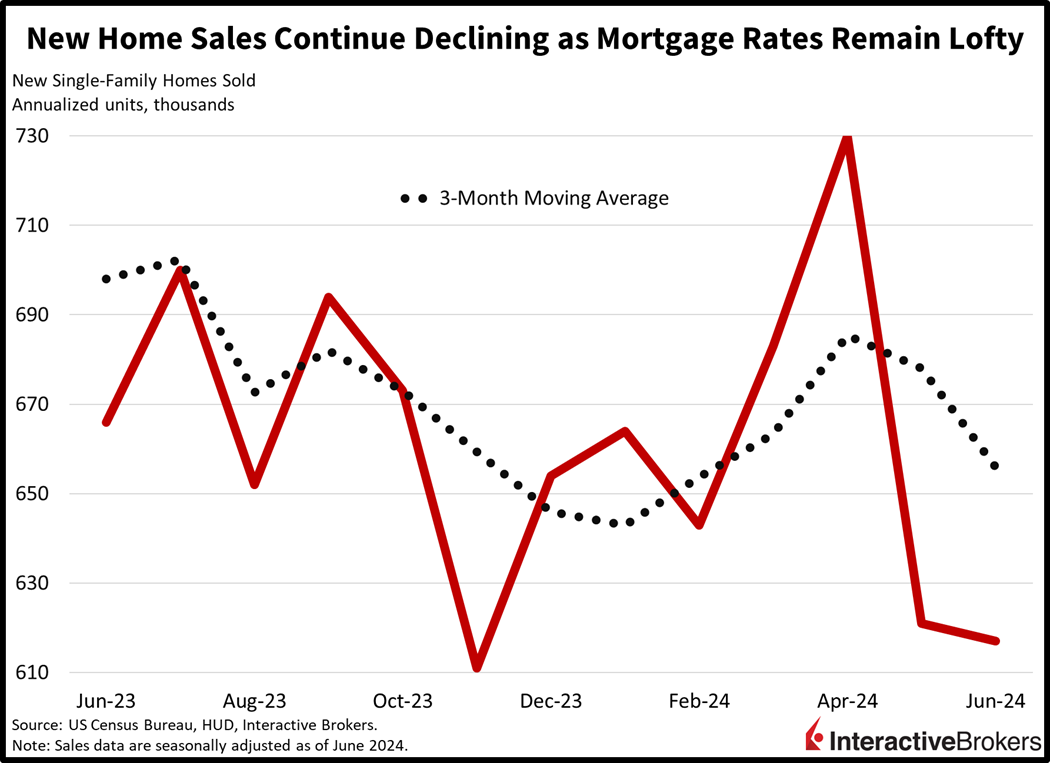

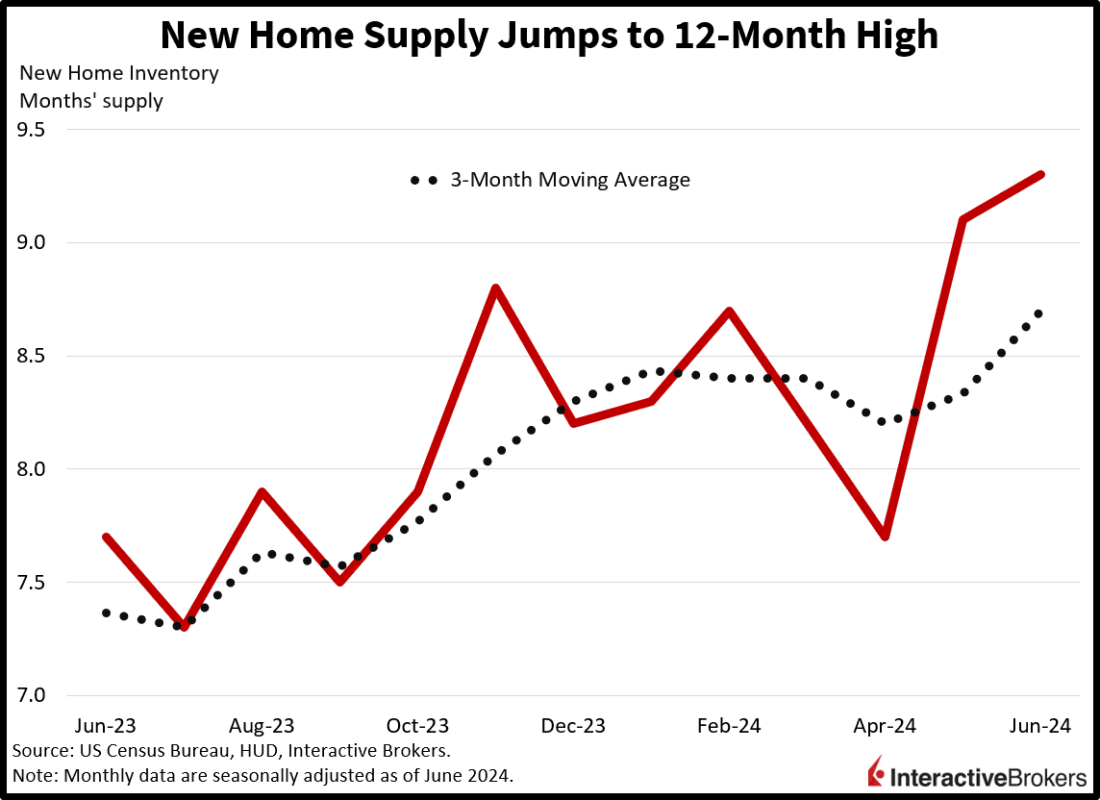

This morning’s new home sales data offered the same insight as yesterday’s report on existing housing: fresh year-to-date lows in transaction volumes paired with a new high in inventory. Stretched housing affordability led to a decline in the pace of new homes being snatched up by buyers, with last month’s reading slipping 0.6% month over month (m/m) to 617,000 seasonally adjusted annualized units, beneath projections calling for 640,00 and the previous month’s 621,000. Sharp m/m declines in the Northeast and Midwest of 7.7% and 6.9% overwhelmed the modest 1.4% and 0.3% increases in the West and South. Inventory, indicated by the amount of supply relative to the rate of current monthly sales, rose to a 20-month peak of 9.3, levels consistent with the great financial crisis of 2008. The ratio hit 12.2, an all-time high, in January 2009.

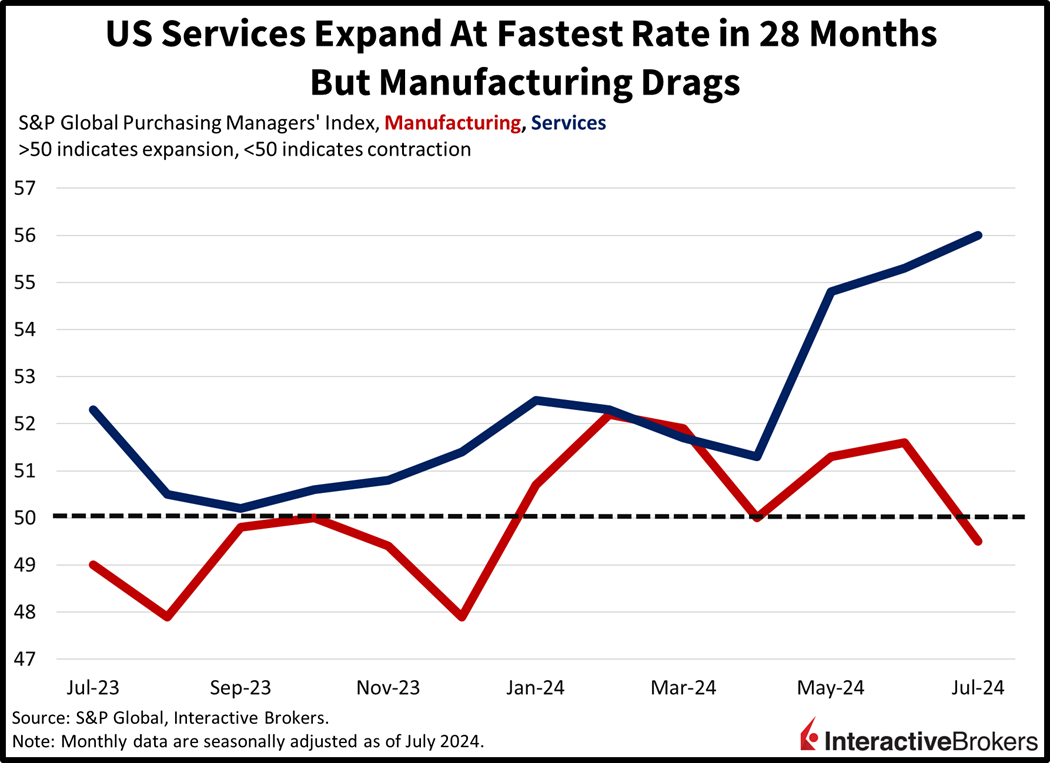

US economic activity started off strong in the third quarter, according to this morning’s Flash Purchasing Managers’ Indices (PMI) from S&P Global. Services momentum accelerated, with July’s score rising to a 28-month high of 56, above both the anticipated 55 and June’s result of 55.3. Manufacturing dragged down results, however, falling into contraction territory with a score of 49.5, below the median estimate of 51.7 and the prior period’s 51.6. Overall, inflationary pressures slipped during the month, but input costs remained hefty, pointing to firms becoming increasingly unable to pass on loftier costs to consumers. These margin pressures have also become more prevalent on earnings calls, as budget-conscious shoppers trade down amidst erratic purchasing patterns, which are weighing on bottom lines.

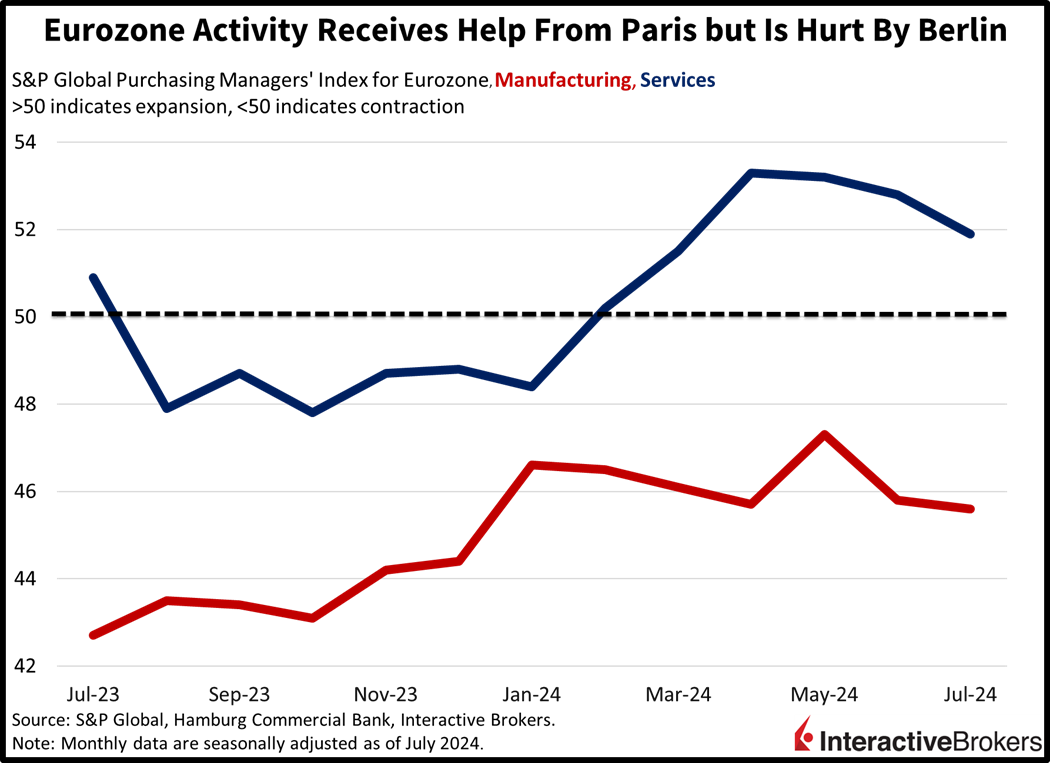

Conditions were bleak across the Atlantic in the eurozone, with business confidence and a lack of hiring weighing on overall performance. Similarly, though, the services sector expanded while the manufacturing sector contracted. Services and manufacturing PMIs came in at 51.9 and 45.6, missing the estimated 53 and 46.1. In comparison, June’s figures were 52.8 and 45.8. Also weighing on the outlook were rising inflationary pressures, contracting productivity and manufacturing orders. The French Olympics did serve to boost the services sector and offset German sluggishness, however. The combination of rising prices and deteriorating productivity may challenge the European Central Bank’s ability to dish out a rate reduction in September.

The first two members of the elite Magnificent Seven posted disappointing results, while Visa payment processing volumes grew slower than expected, pointing to weakness in spending by lower-income consumers. Meanwhile, commercial real estate issues weighed on results for Germany’s Deutsche Bank, which tabled a second planned share buyback this morning. Those are a few points from the following earnings highlights:

Markets are getting punished as investors sell risk assets and pick up safe havens while drifting into hibernation. For stocks, nothing is working, not Harris or Trump, with all major US equity benchmarks in the red. The Nasdaq Composite, S&P 500, Dow Jones Industrial and Russell 2000 baskets are travelling south by 2.6%, 1.6%, 0.8% and 0.3%. Sectoral breadth isn’t as bad as one would think, with 4 out of 11 sectors gaining on the session. Lower interest rates are pushing folks into real estate stocks, loftier oil prices are helping energy, and defensive positioning is motivating purchases of utilities and health care names. But consumer discretionary, technology and communication services are taking a beating; they’re down 3.1%, 2.8% and 2%. Rates are plunging with this morning’s reduction by the Bank of Canada propping up the odds of a Fed cut in September. The 2- and 10-year Treasury maturities are shifting in bull-steepening fashion, changing hands at 4.39% and 4.23%, 11 and 3 bps lighter on the session. The dollar is dancing in lockstep, sinking 25 bps as the greenback depreciates relative to the yen, franc and pound sterling. The US currency is appreciating versus the euro, yuan and Aussie and Canadian dollars, however. Commodities are mixed, with copper and lumber lower by 0.9% and 0.4% on manufacturing and real estate weakness, while gold, crude oil and silver gain alongside volatility protection as market participants hedge against a potential downturn. WTI crude oil is trading at $78.65, benefiting from oversold technical factors as well as dwindling stateside inventories.

Despite recent selling, the S&P 500 is still trading close to 22 times earnings amidst quarterly results that aren’t impressing investors in aggregate. In addition, the benchmark is still up 15% year to date, which is terrific considering it isn’t even August. Yesterday we wrote that a 10% to 15% correction was in the cards this quarter, which is historically the worst period of the year. This quarter, the valuation concerns are being paired with front-loaded gains, irrational exuberance, a high bar for earnings estimates and a presidential election that may very well fundamentally change the technology sector for the worse from an earnings standpoint. Finally, a critical component is found in the narrowing spread between the 2- and 10-year yields, which now stands at 16 bps. When the two instruments have reached rate parity in the past after inversions, violent equity market corrections have occurred. This time isn’t different.

Visit Traders’ Academy to Learn More About Existing Home Sales and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!