- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 23, 2024 at 10:30 am

Yesterday it was the Harris Trade but today it’s the Trump trade as stocks attempt to bounce back from last week’s selloff by using any lever they can pull. But from a probability perspective, election odds haven’t changed much, with Trump still expected to handily become 47. The latest bout of optimism among democrats appears to be stemming from a burst of fresh air resulting from Kamala Harris heading the party’s presidential ticket. Still, it’s highly unlikely that she can claim victory in key battleground states that President Biden captured with his manufacturing heavy, working-class, Scranton background. Harris, in contrast, is a California native and is presumably much more comfortable in Silicon Valley than in the Rust Belt, her former running mate’s stronghold. Against the backdrop, corporate earnings depict a cautious consumer while the economic calendar offers no light at the end of the tunnel for struggling realtors.

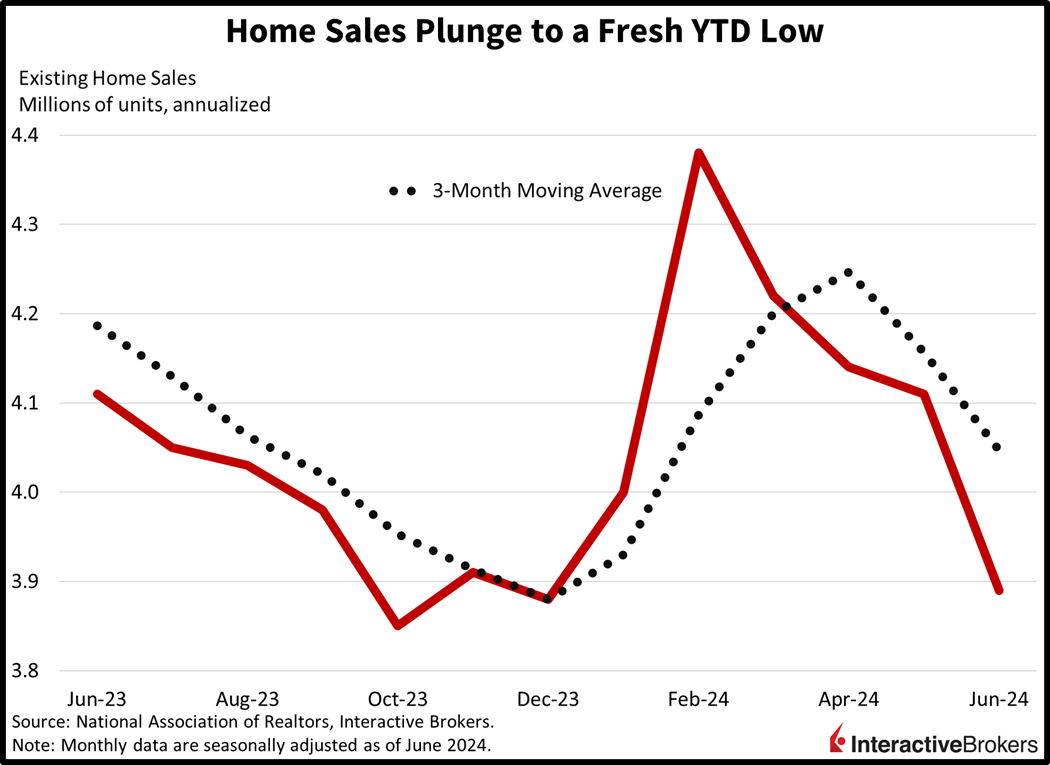

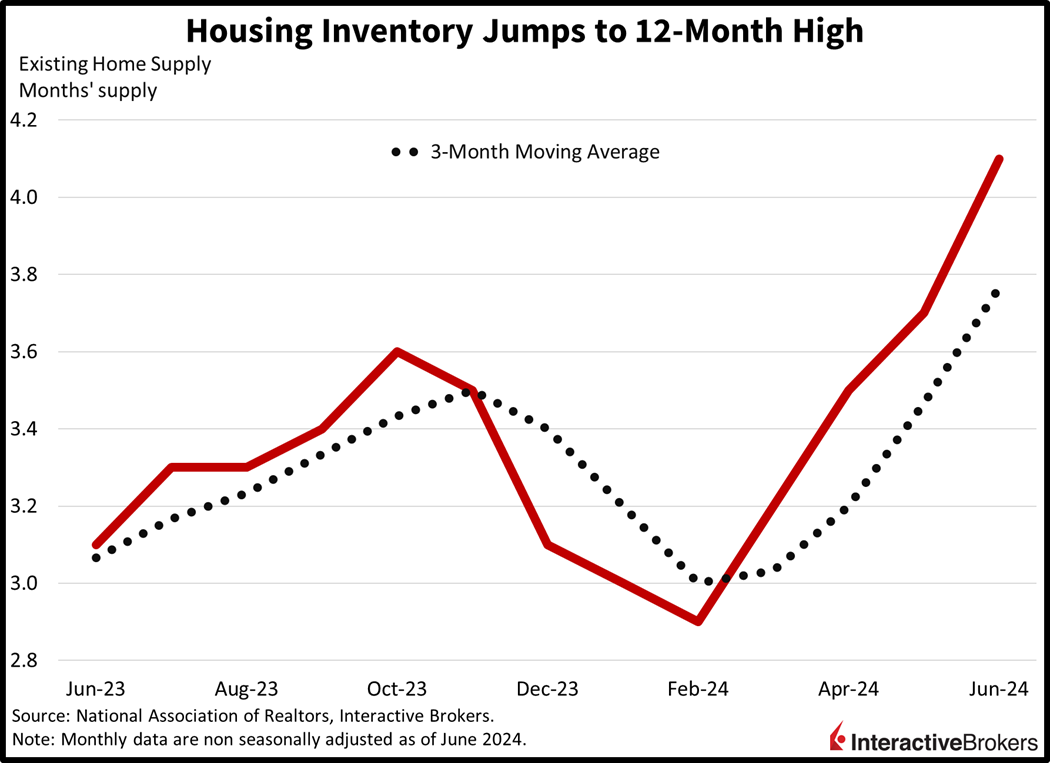

Supply conditions improved significantly in the residential real estate sector last month as sellers grew impatient, but the one-two punch of all-time high prices and elevated mortgage rates overwhelmed the positive effects of loftier inventory. Indeed, the pace of existing home transactions plunged further south to levels that were among the lowest since the great financial crisis. June existing home sales slipped to 3.89 million seasonally adjusted annualized units, a 5.4% month-over-month (m/m) decline, even as inventory rose 3.1% m/m to 1.32 million. Furthermore, inventory as measured by the ratio of the months’ supply and the rate of current monthly sales levitated from 3.7 to 4.1 m/m and from 3.1 months during the same period a year ago.

Despite all four regions posting weakness, the median home sale price rose to $426,900, the tallest level ever recorded. Additionally, condominium and cooperative sales weighed on the headline, with the segment’s 7.1% m/m decline in the pace of transactions underperforming the single-family component’s 5.1% drop. Across the nation, the pace of sales sunk in the Midwest, South, West and Northeast by 8%, 5.9%, 2.6% and 2.1% m/m.

Consumer spending strength appears to be somewhat mixed, with a strong increase in debt service costs curtailing purchases of certain big-ticket items while entertainment spending, at least at theme parks, is moderating, and beverage sales are declining. Shipping volumes are also sagging. On the other hand, air travel is expected to remain strong in the coming months, which has contributed to GE Aerospace posting stronger-than-expected second-quarter results. These earnings insights come as consumers struggle with a 50% year-over-year (y/y) increase in consumer debt payments and a 14% jump in mortgage interest costs, according to the Wall Street Journal and the Bureau of Economic Analysis. Consider the following earnings highlights:

Markets are cautiously bullish as investors await earnings from two magnificent seven members after the close. All major US equity indices are in the green, with the Russell 2000, Nasdaq Composite, S&P 500 and Dow Jones Industrial benchmarks traveling north by 1%, 0.6%, 0.3% and 0.1%. Sector breadth is positive with 7 out of 11 sectors gaining. Piloting the bulls are technology, consumer discretionary and financials, which are up 0.4%, 0.3% and 0.3%. Energy, utilities and consumer staples are offsetting progress, dropping 1.6%, 0.4% and 0.1%. Energy is plunging on the back of a deep 2% decline in crude oil. WTI is trading at $76.66 per barrel, its lowest level since June as expectations for a Gaza ceasefire grow, effectively reducing the commodity’s geopolitical premium. Most other commodities are losing as well, with lumber, copper and silver lower by 1.9%, 0.6% and 0.1%, but gold is bucking the trend; it’s up 0.4%. Softer inflationary pressure in the short-term is helping bond bulls, with the 2- and 10-year Treasury maturities dropping 2 and 3 basis points each and trading at 4.50% and 4.23%. The dollar is modestly higher, however, despite lower yields, as the greenback appreciates relative to most of its major contemporaries, including the euro, pound sterling, franc, yuan and Aussie and Canadian dollars. The US currency is sharply depreciating versus the yen though.

While tech earnings may allow investors to forget about looming election risks in the short term, the harsh reality is that a Trump Vance administration will almost certainly weigh on revenue and profit growth for the largest-caps. Just listen to the rhetoric about China and Taiwan and the strict penalties that they’re planning on imposing on firms that dance with Beijing. The mag7 certainly has heavy exposures to the Asian nation at various stages of the production and sales processes, opening up the door for downside volatility. Given the firms’ influence on major market indices and investor sentiment, any disappointment in earnings or guidance could lead to a 10% to 15% correction in major benchmarks this quarter.

Visit Traders’ Academy to Learn More About Existing Home Sales and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!