- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 24, 2025 at 12:57 pm

Treasury yields are plunging after a pair of Federal Reserve officials drove optimism about a potential rate cut in the first half of this year. Cleveland Fed leader Beth Hammack alluded to June being a live meeting, warranting a reduction in the central bank’s key benchmark shall growth begin to falter. Then came Governor Christopher Waller, remarking that aggressive tariffs may lead to job losses, justifying a step down the institution’s monetary policy stairs. Also bolstering animal spirits is President Trump’s recent tempering, as the Commander in Chief has dialed down his combative rhetoric on trade and the Fed for now. Markets are rallying on the news and investors are adopting risk-on positions consisting of non-defensive stocks and cyclical commodities. Furthermore, they’re piling into the June forecast contract reflecting a 25-bp trim in the fed funds rate, which now sports a 56% probability.

Source: ForecastEx

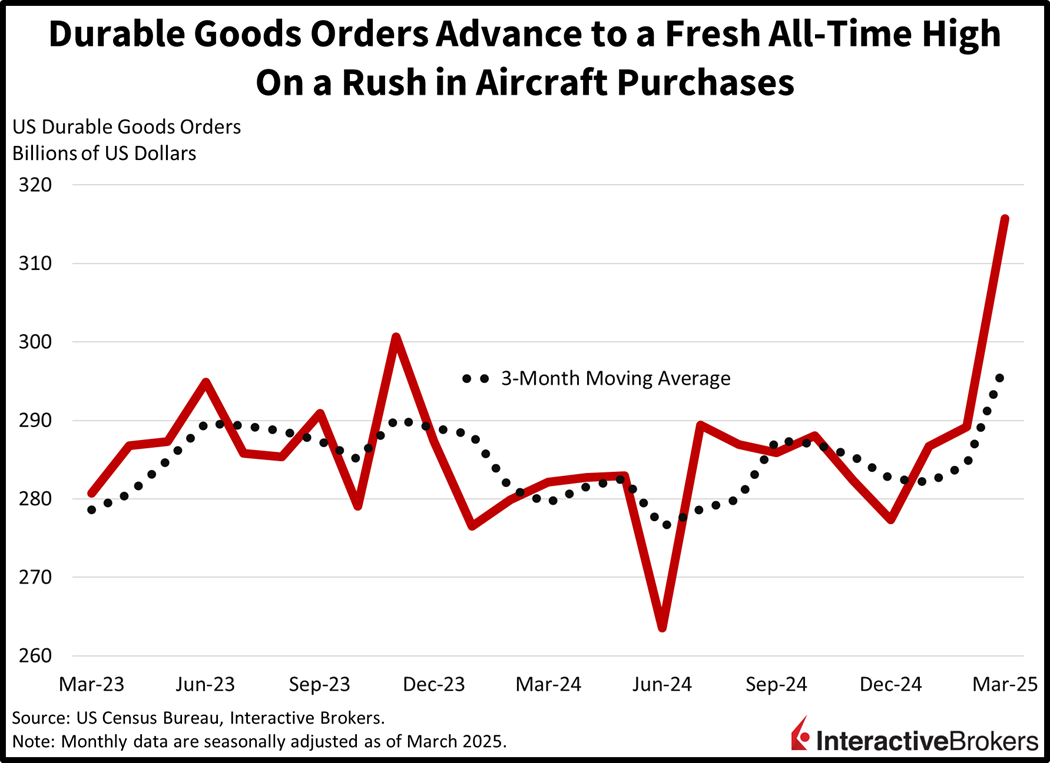

A surge in passenger aircraft purchases ahead of April 2 Trump tariffs sent monthly durable goods orders to a fresh all-time high. The 9.2% month-over-month (m/m) gain exceeded the 2% median estimate and the 0.9% achieved in February, helping to push the headline above its previous peak in November 2023. Driving the big beat was a 139% m/m increase in nondefense airplanes and a 2.3% m/m uptick in the automobile category. The momentum wasn’t broad based with all other major components with increases coming in below 1%. Meanwhile, the computers/electronics and electrical equipment/appliance segments saw declines of 1.2% and 0.5%. Non-defense capital goods excluding aircraft, a critical indicator of business investment rose, just 0.1%, failing to recover from February’s 0.3% decline.

Existing home sales plunged in March despite a significant increase in inventories. Elevated prices, which climbed for the 21st consecutive month on a year ago basis, alongside heavy mortgage rates continue to plague the sector. The pace of transactions fell 5.9% m/m to 4.02 million seasonally adjusted annualized units, beneath the 4.13 million projected and February’s 4.27 million. The single-family segment’s closings dropped 6.4% m/m while the condominium/cooperative component countered some of the weakness, coming in unchanged. The stock of homes for sale rose to 1.33 million units, up a sharp 8.1% m/m and 19.8% year over year (y/y).

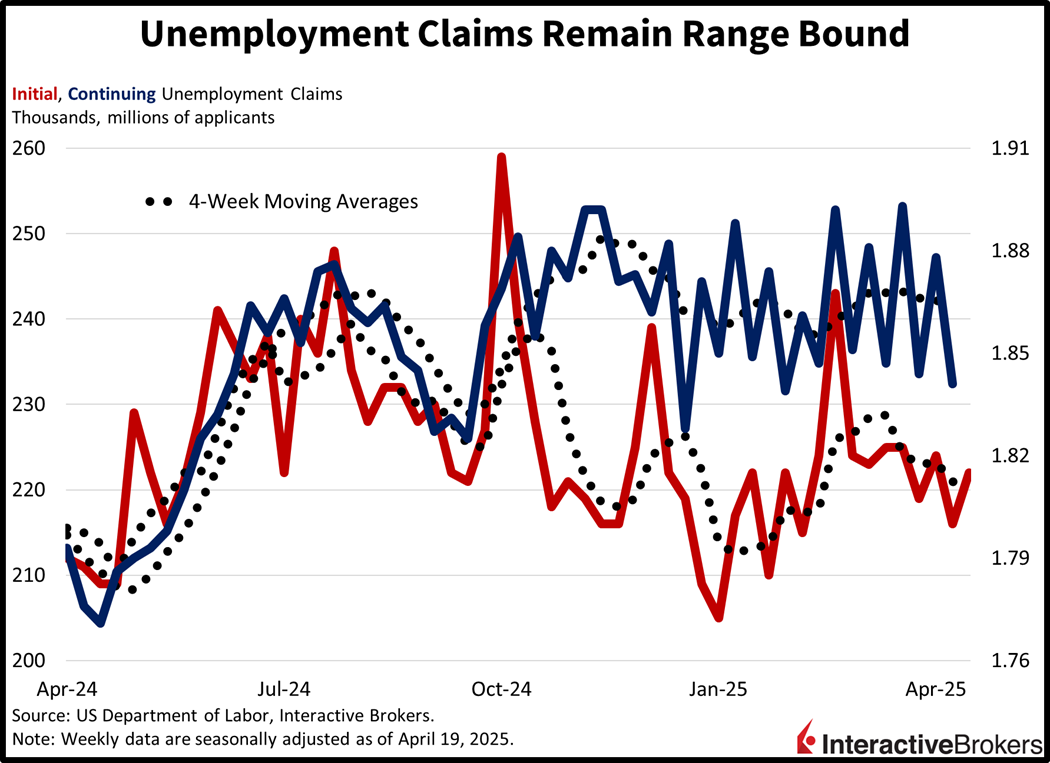

Labor conditions were well anchored throughout the past two weeks as trips to unemployment offices remained tempered. Initial claims rose modestly to 222,000 during the week ended April 19, near expectations and above the 216,000 recorded in the previous period. Continuing claims fell to 1.841 million in the preceding 7-day interval which concluded on April 12, beneath the median estimate of 1.880 million and the 1.878 million from the prior print. Four-week moving average trends moved south on both fronts, from 221,000 and 1.866 million to 220,250 and 1.864 million.

Equity and fixed-income bulls are bringing home the bacon today as a combination of a calmer President Trump and dovish talk from Fed officials send stocks to the nosebleeds and yields to the basement. All stock benchmarks are gaining strongly with the Nasdaq 100, S&P 500, Russell 2000 and Dow Jones Industrial indices up 1.9%, 1.3%, 1.1% and 0.6%. All ex-defensive sectors are participating in the enthusiasm and leadership is comprised of technology, communication services and materials, which are higher by 2.7%, 1.5% and 1.4%. Non-cyclical consumer staples and utilities are the only 2 of the 11 segments lower, trimming 0.9% and 0.1%. Rates are plunging and the 2- and 10-year maturities are changing hands at 4.34% and 3.81%, 5 and 6 basis points (bps) lighter on the session. Softer borrowing costs are weighing on the greenback, however, as it depreciates against the euro, pound sterling, franc, yen and Aussie tender but appreciates versus the yuan and loonie. The US Dollar Index is down 24 bps. Commodities are also taking part in the bullish action as gold, lumber, crude oil and copper advance 1.2%, 1.1%, 0.6% and 0.3% but silver is losing 0.4%.

Stock and bond bulls alike love liquidity and the dovish talk from the Fed’s Hammack and Waller certainly gave animal spirits a lift today. But President Trump’s softening posture is also serving to support earnings expectations, at least in the short term, as it looks increasingly likely that the head of state isn’t looking to plunge the US into recession to achieve his challenging goals of a more even playing field on global trade and reduced deficits. It’s been a good week for markets thus far, but investors are left wondering if the stream of positive developments can turn in the next few sessions. The Commander in Chief may be heading in one direction only to pull an abrupt spin the other way, especially if he perceives that the constituency thinks he is wavering.

South Korea’s prolonged political turmoil and global trade fears have halted the country’s four-year streak of quarterly gross domestic product (GDP) growth with the country’s economy contracting 0.2% and 0.1% quarter over quarter and y/y during the first three months of 2025. The metrics had climbed 0.1% and 1.2% during the fourth quarter of 2024, and they missed the consensus forecasts of 0.1% and 0.2%. In releasing the first-quarter estimates, the Bank of Korea noted that domestic demand and exports had weakened, but the main driver of the contraction was construction falling 12.4% y/y. Korea’s political leadership has been thrown into an upheaval with impeachment trials against former president Yoon Suk Yeol and Prime Minister Han Duck-soo being held during the first quarter.

Japan’s Corporate Services Price Index climbed 0.7% and 3.1% month over month and y/y in March after jumping 0.1% and 3.2%, respectively, in February. The y/y result was slightly hotter than economists’ forecast of 3%. For the m/m result, international air passenger transportation led the overall increase with costs spiking 7.6% followed by domestic air passenger transportation, which moved north 7%.

The Confederation of British Industry (CBI) Industrials Trends Orders Index for April came in at -26, a marginal change from -29 in March and better than the median forecast of -35. While the motor vehicles and transport equipment sector experienced an increase in output, most other categories reported lower volumes. Survey respondents, broadly speaking, expect new orders to decline in the three months to July with weakness in both domestic and export channels. Approximately half of businesses surveyed attributed their negative outlook to political and economic conditions abroad. That was the highest percentage of survey respondents to identify those factors as challenges since April 2021.

UK residents aren’t taking the trade war in stride. Indeed, the British Retail Consortium today reported that households’ views of the economy over the next three months fell from -35 in March to -48 this month, its lowest level on record. Consumers’ views of their financial situations dipped from -10 to -16. Conversely, retail spending in April rose to +3 after a zero reading in March. The consortium attributes the sharp decline to fears about the global trade war increasing prices.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!