- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 31, 2025 at 1:15 pm

As I write this, we’ve made it through about half of the highly consequential data deluge that offered the potential for significant market moves. Chair Powell’s relatively dour press conference led to some modest intraday declines, but those who bought that fleeting dip were feeling vindicated after Microsoft (MSFT) and Meta Platforms (META) earnings were released. This morning’s Core PCE report was taken in stride; will Apple (AAPL) and Amazon (AMZN) continue the earnings party today? And how might tomorrow’s jobs report affect the proceedings?

By the way, it’s also the end of the third very solid month of gains in a row for major indices. July’s roughly 3% gain for the S&P 500 (SPX) comes after a +6.15% May and +4.96% June. The Nasdaq 100 (NDX) has been even more stellar, with this month up about 3.25% after +9.04% and +6.27% in May and June respectively. We saw some late buying yesterday – it would not be surprising to see some window dressing – at least in some of the smaller names that have attracted recent money flow.

We concluded yesterday’s piece with the following:

From a macro viewpoint, much matters whether those cross-currents offset or reinforce each other. If they offset, then the result will be relatively muted volatility. If they reinforce each other, then buckle up.

The “buckle up” comment seemed particularly appropriate when pre-market futures were climbing over 1%. Now, shortly before midday on the East Coast, major indices are only marginally higher, kept afloat only by META’s +12% pop and MSFT’s +4.5% bump. It has been fascinating to watch the early rally fade as breadth trended slightly negative.

Yesterday’s events point to a key pair of crosscurrents that the market will need to reckon with over the coming weeks. On one hand we have the market’s love of all things AI, along with a willingness, if not an eagerness to reward ever-increasing amounts of capital spending on related products. On the other, we have the Powell’s intransigence about cutting rates even amidst withering criticism from the President and growing, but still modest dissent from FOMC members. This comment from early in yesterday’s press conference set the tone:

Q. There is a lot of lean in the markets and not to mention out of the Administration for a rate cut now in September. Is that expectation unrealistic at this point?

CHAIR POWELL. So, as you know, today we decided to leave our policy rate where it’s been, which where I would characterize as modestly restrictive. Inflation is running a bit above 2 percent, as I mentioned, even excluding tariff effects. The labor market’s solid, historically low unemployment. Financial conditions are accommodative, and the economy is not — the economy is not performing as though restrictive policy were holding it back inappropriately. So, it seems to me and to almost the whole committee that the economy is not performing as a restrictive policy is holding it back inappropriately and modestly restrictive policy seems appropriate. [Emphasis mine]

Quite frankly, this is along the lines of what we have been asserting for some time. Clearly, the current level of short-term rates is not deterring stock market speculation, and there is no evidence that companies are having any difficulties accessing financing. But that is not what markets wanted to hear.

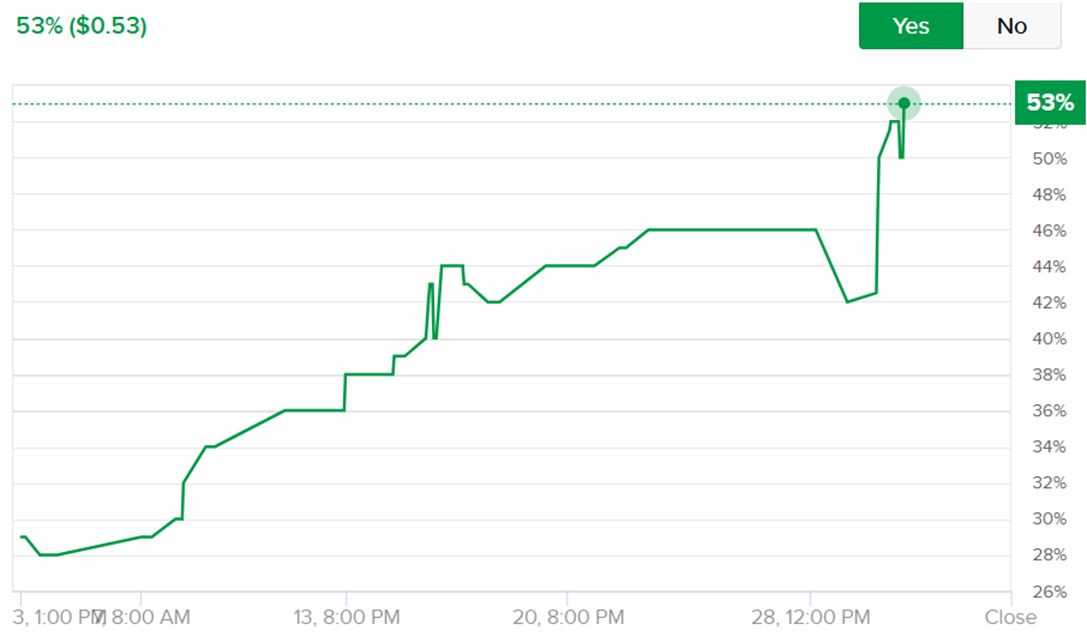

That comment triggered a bit of selling in stocks, a quick spike in VIX over 17, and a modest reassessment of the likelihood of rate cuts over the next few FOMC meetings. As of Tuesday, CME Fed Funds futures showed a roughly 70% chance for a 25 basis point cut in September and an 85% chance for another by December, but they now only show a roughly 40% chance for September and roughly 35% for another in December. This broadly agrees with the markets on ForecastEx, where a “Yes” for rates above 4.125% in September has steadily risen to a current 53%, and a yes for a rate above 3.875% in December is now 47%.

The earnings from AAPL and AMZN raise the stakes for stocks in the short-term, while tomorrow’s Nonfarm Payrolls (+105K consensus) and Unemployment Rate (4.2%) could go a long way to clarifying the need and/or desirability for rate cuts soon. If you’re already bucked in, please keep your seat belts fastened.

Source: ForecastEx

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!