- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 18, 2023 at 11:00 am

Federal Reserve (Fed) tightening cycles, without exception, have been associated with financial crises.

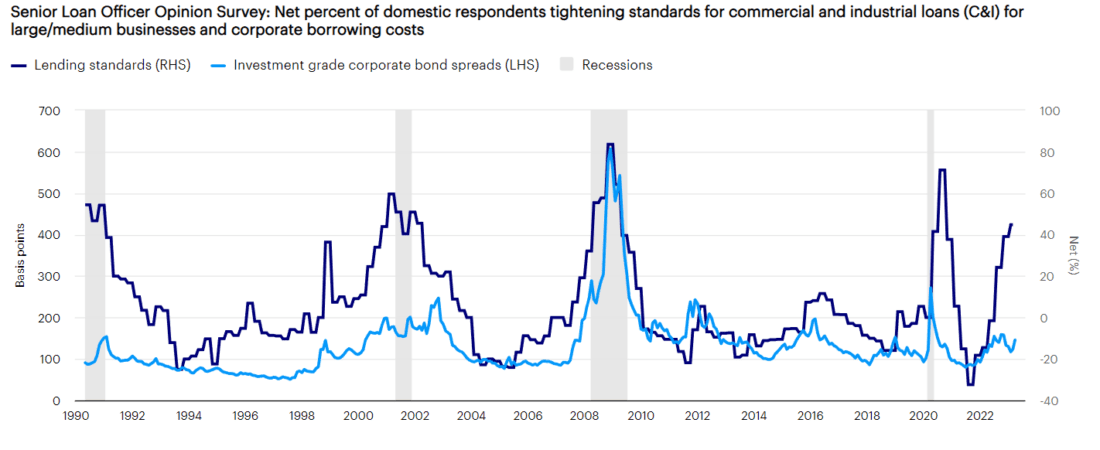

Tightening lending standards, which has historically led to an economic downturn, is raising the likelihood of a recession.

The bank failures may mark the end of market downturns and the beginning of a new market cycle, as they did in the past.

While the failures of Silicon Valley Bank (SVB), Signature Bank, and First Republic, and problems at Credit Suisse were unnerving and led to market volatility, they weren’t necessarily unexpected. Fed tightening cycles, without exception, have been associated with financial crises. Here are a few key things to keep in mind about bank crises past and present. Get more data and charts in our chartbook: Trending Conversations — Bank crisis in perspective.

Source: US Federal Reserve, 3/31/23. The federal funds rate is the rate at which banks lend balances to each other overnight. Quantitative tightening (QT) is a monetary policy used by central banks to normalize balance sheets.

Despite all the “financial accidents” that occurred across each of the Fed tightening cycles, there have only been three instances in modern US history of systemic bank failure — the 1930s, the late 1980s, and the late 2000s, according to the Federal Deposit Insurance Corporation.

The health of bank balance sheets is a fundamental difference between 2008 and today. Bank balance sheets appear to be sound as they are heavily comprised of high-quality and liquid assets, such as US Treasury bonds and cash.1 A central feature of the 2008 Global Financial Crisis was that many of the nation’s largest and most interconnected banks had levered exposure to the US housing market. Assets were worth far less than stated, and the leverage was significantly greater than had been claimed. The banks failed because of bad loans and poor credit underwriting.

Banks were already tightening lending standards prior to the recent bank failures. It’s expected that lending standards will tighten further, which raises the likelihood of a US recession. Historically a tightening in lending standards has led to higher corporate borrowing costs as well as a downturn in US economic activity.

Sources: US Federal Reserve and Bloomberg L.P., 3/23/23. Investment grade corporate bonds are represented by the Bloomberg US Corporate Bond Index. The option-adjusted spread (OAS) is the measurement of the spread of a fixed income security rate and the risk-free rate of return, which is then adjusted to account for an embedded option, such as calling back or redeeming the issue early. The Senior Loan Officer Opinion Survey on Banking Lending Practices is a survey of up to 80 large domestic banks and 24 US branches and agencies of foreign banks. Indexes cannot be purchased directly by investors. Past performance does not guarantee future results.

Bank failures could potentially mark the end of market downturns and the beginning of new market cycles. That was the case in 1984 with the Continental Illinois failure as well as in the early 1990s following the Savings and Loan Crisis. The Global Financial Crisis is an outlier and represents a tail risk to an optimistic view. The 2008 crisis, however, engulfed banks with assets representing roughly 7% of the US gross domestic product (GDP). The current crisis has thus far impacted fewer and smaller banks than in 2008 and may better resemble the crises in 1984 and 1990.

For more charts and perspective, read the complete chartbook: Trending Conversations — Bank crisis in perspective.

Footnotes

—

Originally Posted April 14, 2023

Perspective on the bank crisis by Invesco US

Important information

NA2828927

The S&P 500® Index is a capitalization-weighted index of 500 stocks intended to be a representative sample of leading companies in leading industries within the US economy.

The Bloomberg US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility, and financial issuers.

Indexes are unmanaged and cannot be purchased directly by investors. Index performance is shown for illustrative purposes only and does not predict or depict the performance of any investment. Past performance does not guarantee future results.

All investing involves risk, including the risk of loss.

The opinions referenced above are those of the author as of Mar. 31, 2023. These comments should not be construed as recommendations but as an illustration of broader themes.

Forward-looking statements are not guarantees of future results. They involve risks, uncertainties, and assumptions; there can be no assurance that actual results will not differ materially from expectations.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED

MAY LOSE VALUE

NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds. Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2024 Invesco Ltd. All rights reserved.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Invesco US and is being posted with its permission. The views expressed in this material are solely those of the author and/or Invesco US and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!