- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 22, 2025 at 10:30 am

The release of the November CPI report on Thursday without the data for October made it virtually impossible to form any useful picture of the state of inflation and the inflation outlook. There were no month-over-month percent changes for November or October except for prices for gasoline.

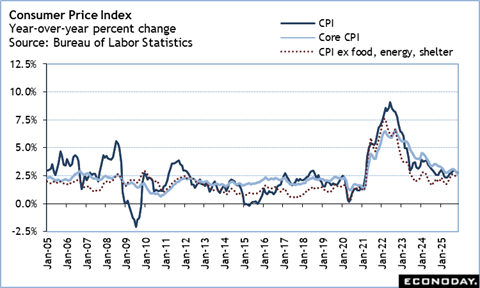

The year-over-year rise in the CPI in November is 2.7 percent, a decline when compared up 3.0 percent in September. The core CPI is up 2.6 percent in November compared to up 3.0 percent in September.

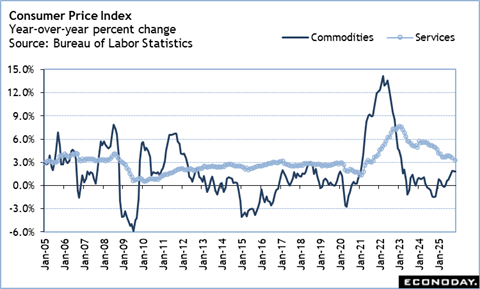

The year-over-year increase in the CPI for commodities remains more elevated at up 1.8 percent in November compared to 1.9 percent in September. Commodities prices have been the main source of price inflation in recent months. The CPI for services continues to reflect deflation, although the 3.2 percent annual increase in November remains what the FOMC would term as elevated. The services CPI for September is up 3.6 percent. Notably, the CPI for shelter costs – which accounts for about 1/3 of the CPI basket – continues to trend lower. The annual increase for the CPI for shelter is 3.0 percent in November compared to 3.6 percent in September.

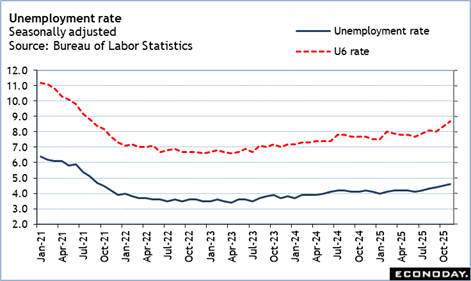

Missing data in October had an impact on the monthly employment report for November. The household survey did not take place for October due to the government shutdown and the BLS did not attempt to collect the data. The national unemployment rate rose to 4.6 percent in November compared to 4.4 percent in September. Making an educated guess, the unemployment rate has been rising about one-tenth a month since 4.1 percent in June. The November rate is the highest since 4.7 percent in September 2021.

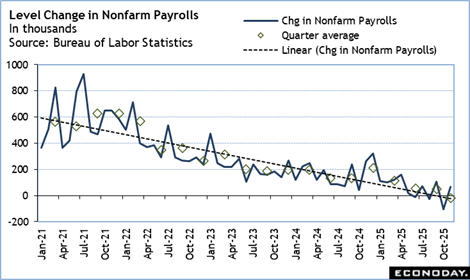

The increase of 64,000 in nonfarm payrolls in November comes after a decline of 105,000 in October – mainly from idled workers during the federal government shutdown – and an increase of 108,000 in September. Looking past the month-to-month variation, hiring is trending lower steadily. Moreover, it is largely confined to a few narrow sectors like construction and healthcare where skilled workers remain in high demand.

The underlying story appears to be that there is less hiring and more job cutting, although outright job losses remain relatively low. The labor market is continuing to rebalance after the massive layoffs in federal employees earlier this year, the rapid adoption of AI technology, consolidation in the retail sector, businesses figuring out how to operate efficiently in the new tariff environment, and the impact of heightened uncertainty on consumers and businesses.

—

Originally Posted December 19, 2025 – Last Week in Review: US CPI Leaves Investors Guessing

Important Legal Notice: Econoday has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Econoday does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time.

© 1998-2022 Econoday, Inc. All Rights Reserved

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Econoday Inc. and is being posted with its permission. The views expressed in this material are solely those of the author and/or Econoday Inc. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!