- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 25, 2024 at 11:00 am

News that US economic growth accelerated at a much faster-than-expected pace in the second quarter has sent market participants on a roller-coaster ride. Indeed, stocks, bonds and the greenback alike have moved quite violently, swinging from sharp losses to notable gains in just the first few hours of trading. Concerns expressed during earnings calls about the health of consumers have also influenced investor behavior, with rate watchers now pricing in three consecutive cuts from the Fed starting in September. Not so fast: ladies and gentlemen, my outlook for July and August inflation reflects price pressures that are rising well above the central bank’s target, enabling the committee to wait until December to reduce the cost of capital.

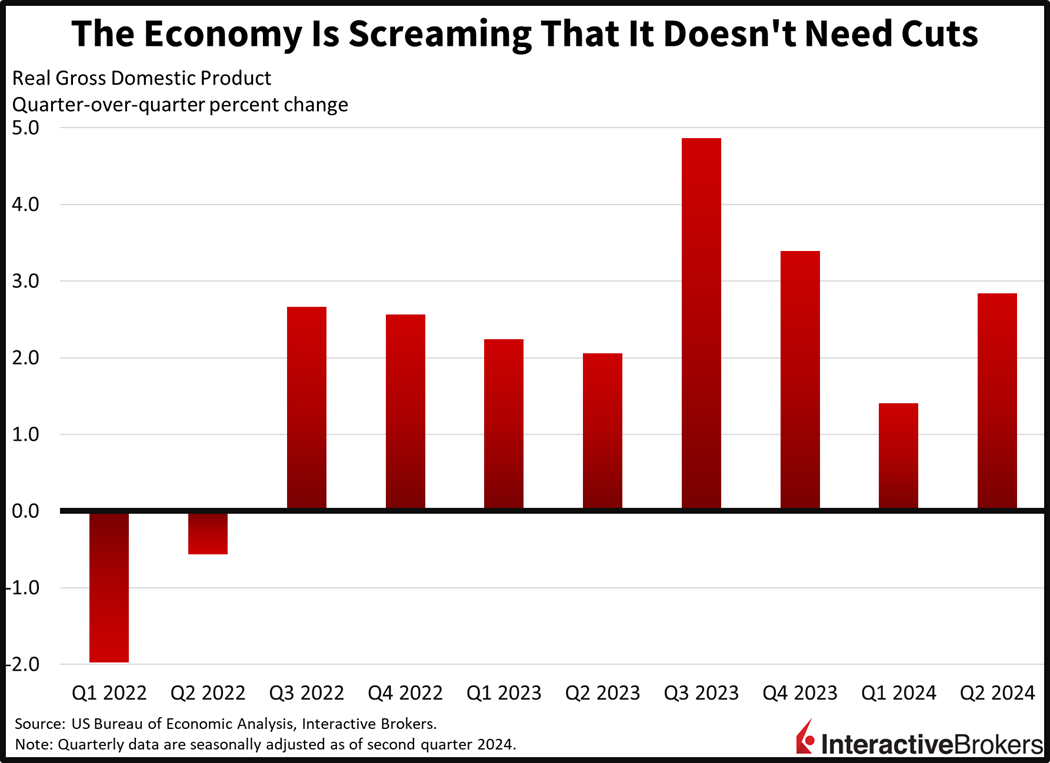

The US economy continues to expand on the back of resilient consumer outlays, strong capital expenditures and unwavering deficit spending. US gross domestic product (GDP) rose 2.8% in real terms on an annualized, seasonally adjusted, quarter-over-quarter (q/q) basis during the second quarter. The figure reflects an acceleration from the first quarter’s 1.4% and arrived ahead of projections calling for 2%. Driving the upside beat were services spending, inventory builds, capital expenditures, goods outlays and government disbursements, which added 1%, 0.8%, 0.7%, 0.6% and 0.5% to the headline. Meanwhile, net exports and residential investments weighed on performance, subtracting 0.7% and 0.1% from growth. The quarterly Personal Consumption Expenditures (PCE) price indices within the print offered consistent progress on inflation, with the overall number up 2.6% while the core result rose 2.9%, lighter than the previous period’s 3.4% and 3.7%. Tomorrow’s PCE data for June will provide further clues on the direction of price pressures and economic growth in the shorter term.

Turning to the durable goods front, a sharp decline in aircraft orders significantly weighed on results. Furthermore, several airlines canceled orders for planes, with the passenger jet category experiencing a whopping 127% month-over-month (m/m) decline. The dismal number led to durable goods purchases tanking to levels not seen since November 2021. If we were to consider the nominally reported figures in real terms, we’d have to go back further. Durable goods orders declined 6.6% m/m, much worse than the 0.3% growth expected and the 0.1% increase in May. There were some bright spots, however, including a 1% m/m increase in business investment as well as 1.6%, 1.3% and 0.8% gains in the smaller machinery, electrical equipment and computer product categories. Finally, backlogs continued to be worked down amidst depressed demand, pointing to no end in sight for the manufacturing recession.

The labor market reflected modest relief in the past two weeks, with both initial and continuing unemployment claims sliding lower. Initial claims fell to 235,000 for the week ended July 20, while continuing claims dropped to 1.851 million for the prior period which ended on July 13. The figures arrived softer than the projected 238,000 and 1.860 million as well as from the previous interval’s 245,000 and 1.860 million. Four-week moving average trends moved the other way for both indicators, however, from 235,250 and 1.849 million to 235,500 and 1.854 million.

Airlines are facing headwinds from excess capacity, while in other economic sectors, consumers are holding off on buying big-ticket items such as washing machines. In other topics from the recent quarterly earnings reports, demand for artificial intelligence is growing strongly at IBM. Those are a few points from the following second quarter earnings reports:

Market participants are surviving the morning selloff and opting for the Trump trade and Treasurys rather than the Harris trade comprising high-flying, Silicon Valley tech stocks. Most major indices are now higher with the Russell 2000, Dow Jones Industrial and S&P 500 leading with gains of 1.8%, 0.8% and 0.3%. The Nasdaq Composite is down 0.2%, however, which is peanuts considering that it sank almost 2% earlier. Equity sector breadth is terrific with 10 out of 11 components gaining on the session. The top contributors are industrials, energy and financials; they’re up 1.4%, 1.3% and 1.2%. Technology is the sole bearish category, dropping 0.2% at the moment. Treasurys are catching a bid with the 2- and 10-year maturities changing hands at 4.41% and 4.23%, 2 and 5 basis points lower during the session. The dollar is near the flat line, however, as it appreciates relative to the pound sterling, yuan, yen and Aussie and Canadian dollars but loses ground versus the euro and franc. Commodity land is mixed, with copper, lumber and crude oil up by 1.4%, 1.2% and 0.6% but silver and gold getting hit by 3.7% and 1.5%.

This year’s inflation reports have arrived in-line with the Fed’s targets 2 out of 6 times, which tells me we need a few more cool ones before we start pricing in significant reductions. Against the backdrop of accelerating economic growth and tight labor conditions, a Fed that begins to accommodate too early will almost certainly deal with a reignition of inflationary pressures. Financial conditions must remain well-anchored for price levels to behave, while the election year features a Treasury that is offsetting monetary policy restriction with excessive fiscal stimulus. The two-sided goals are a troubling combination that has kept financial conditions loose and risk-taking behavior buoyant, countering the efforts to quell price pressures for good. Finally, it’s appropriate for the Fed to reduce its benchmark only once this year after the election, considering the stimulus provided by the Treasury is watering down the central bank’s attempts at 2% inflation.

Visit Traders’ Academy to Learn More About Gross Domestic Product and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!