- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 14, 2025 at 1:04 pm

There were several good reasons for stocks to rally this morning. Since yesterday’s close, we learned that we are likely avoid a government shutdown tonight and we’ve so far had a dearth of new tariff threats. Plus, we seemed due for a bounce amidst the oversold conditions that allowed us to “achieve” the widely reported 10% correction in the S&P 500 (SPX). Thus, I was not at all surprised to see pre-market futures rise. But I am surprised to see indices doubling those gains in mid-morning even after a truly atrocious reading on consumer sentiment.

There is no way to sugarcoat today’s University of Michigan data. Frankly, it stinks.

While the Sentiment reading is the lowest in over two years, the prior low was registered on November 30, 2022. That was also the prior high reading for the 1-Year Inflation reading. By the way, that was a rather opportune time to buy stocks. Expectations, however, haven’t been this low since July 31, 2022, which was in the teeth of that year’s bear market. And 5-10 Year Inflation number has not been this high since 1991!

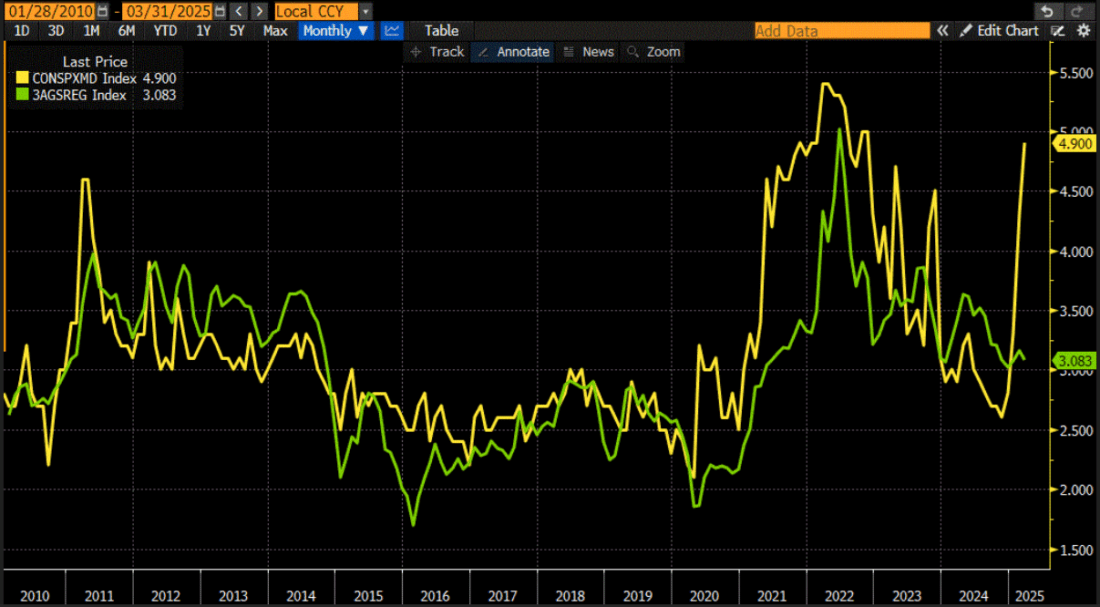

For several weeks, we’ve been discussing how a range of consumer sentiment readings have been deteriorating. On February 7th we noted an unexpected decline in the UMich Sentiment reading, from 71.1 to 67.8, and a head-scratching rise in 1-Year Inflation Expectations to 4.3% from 3.3%. That reading typically follows pump prices for gasoline. But we noted that there was no corresponding increase in gas prices, and the current reading continues to far outpace relatively quiescent pump prices:

Source: Bloomberg

The last time we saw a spike of this magnitude was in 2021, a good year for stocks. But while the prior spike was driven by Covid-era supply shocks and stimulus, which also led to rising gas prices, none of those conditions exist now. Perhaps this spike is being driven by tariff fears, perhaps it is being driven simply by bad vibes. It will be hard for the Federal Reserve to simply shrug off a jump off this magnitude at next week’s meeting.

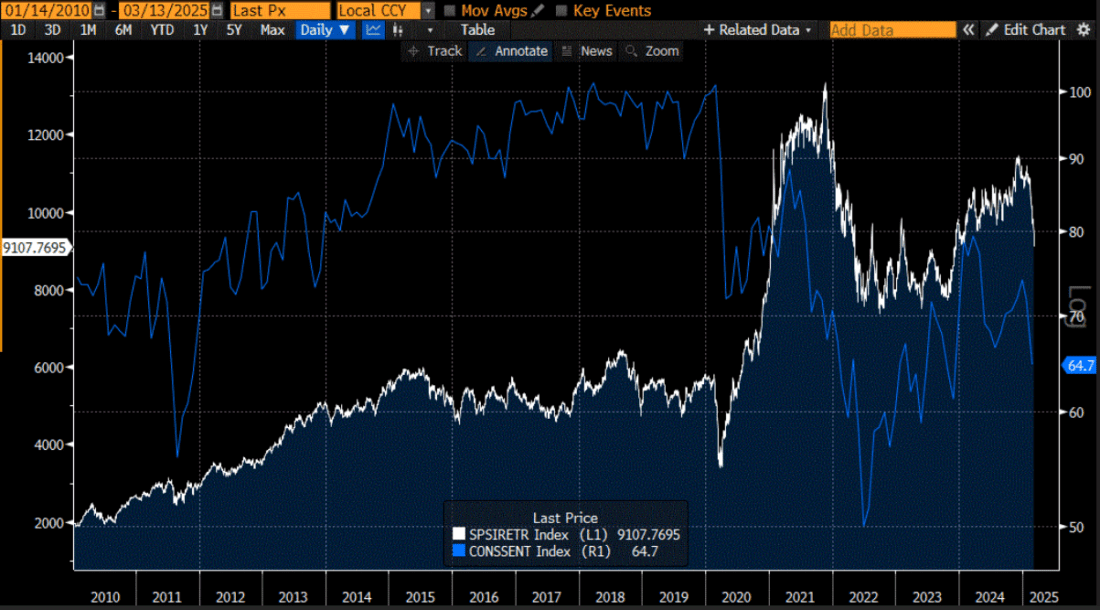

The plummeting sentiment certainly is affecting retail stocks. There is an understandably close relationship between consumer sentiment and the S&P Retail Select Industry Index, the one that underlies the popular XRT ETF. The relationship held through most of the 2010s, then switched to a new plateau when stocks took a leap after Covid:

Source: Bloomberg

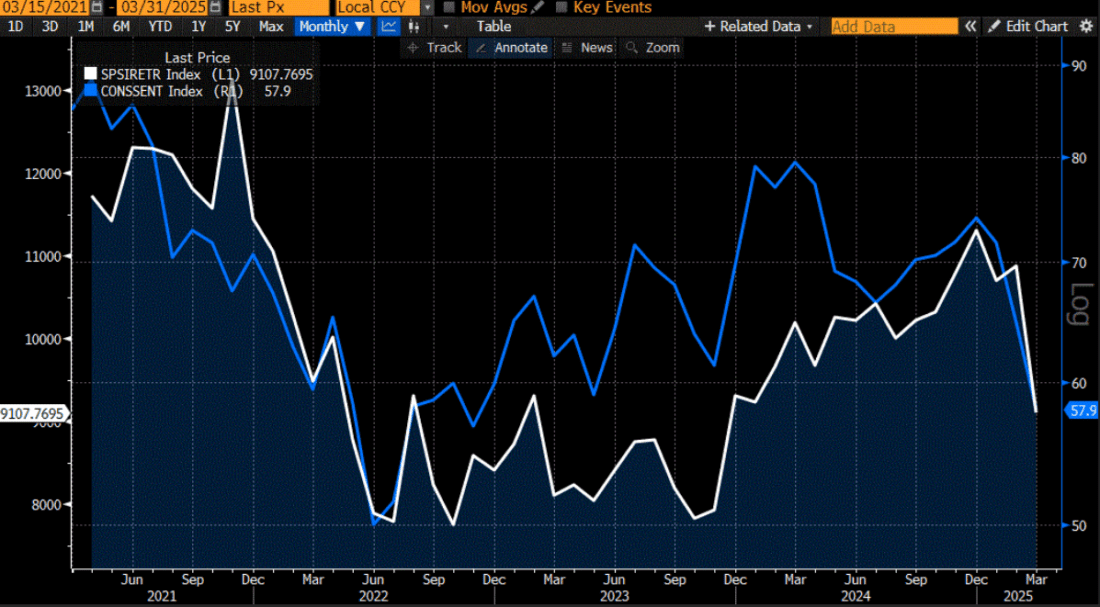

The relationship has been especially close over the past four years:

Source: Bloomberg

So, why are stock traders so sanguine today. It could be that they too recognize that some of the parlous UMich numbers last touched these levels just as the market bottomed in 2022, but I’ve frankly heard no commentary to that effect. Instead, I think it’s human nature. Many traders despise missing a rally, regardless of rationale. FOMO can outpace actual fear, which is one reason why bear market rallies can be among the most powerful of all. This is not to suggest that the recent decline is anything more than a basic correction so far, but the rationale behind the latter part of today’s bounce seems to have that character. (As noted, there were solid reasons for the initial move higher.) That it is occurring on a Friday, when we have over 600 expiring options classes that can be pushed through strikes, probably adds to the rally’s ferocity. The final test will be to see how many of these sanguine traders feel like taking long positions home with them over the weekend.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

How about the fact that expectations were so bad to begin with it is not of a surprise that people are feeling downbeat?

You forgot to mention that Sentiment sank mostly among democrats (and a few independents), not among republicans. It explains a lot.

The economy certainly appears to be deteriorating. Less demand could prevent a resurgence of inflation should companies decide to sacrifice margins to move products. I agree market activity appears to be a bounce rather than the beginning of a new move higher. Selling rallies is probably the prudent action until tariffs are permanently gone or stocks are dramatically lower.

It is difficult to know these days whether a sell off or a subsequent rally is driven by human judgement or mechanical AI based algorithms. So much selling and buying is based works on presets like stop losses, index fund/ETF rebalancing, traders automated buy & sell signals, fibonacci retracement, delta hedging, option assignment, shorting etc. etc.. So many of these functions of daily stock market volume are not driven by animal spirits, FOMO, greed or fear, but by lightening quick preset buy and sell commands as a function of expanding AI. The ripple from one small pebble dropped into a pond can very quickly become a tsunami of water over a very small distance. Navigating this rising wall of water is become harder and harder for the average investor.

Human greed and fear unleash the bots at tipping points

The market was obviously short term very oversold, plus there were probably some buyers for the SPY dividend next Friday. I continue to sell the rallies, so I was actually glad to see a rally, it was looking like there was going to be a crash before any bounce. The S&P 500 market cap stands at over $46 Trillion, down from over $50 Trillion at the peak last month, but still in big bubble territory by most historical metrics. (And $46 Trillion is just the S&P 500, not all stocks.) I have not change my outlook that the S&P is a LOCK to see 4500 again at some point, a view that I have had since months before the election; it could go much lower, but 4500 is my lock number. I think many investors with cash are waiting for lower prices, and they are going to get them.