- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 12, 2024 at 10:15 am

Market surged as the election results favored Republicans, overshadowing the Fed’s rate cut and raising inflation concerns amid anticipated policy shifts.

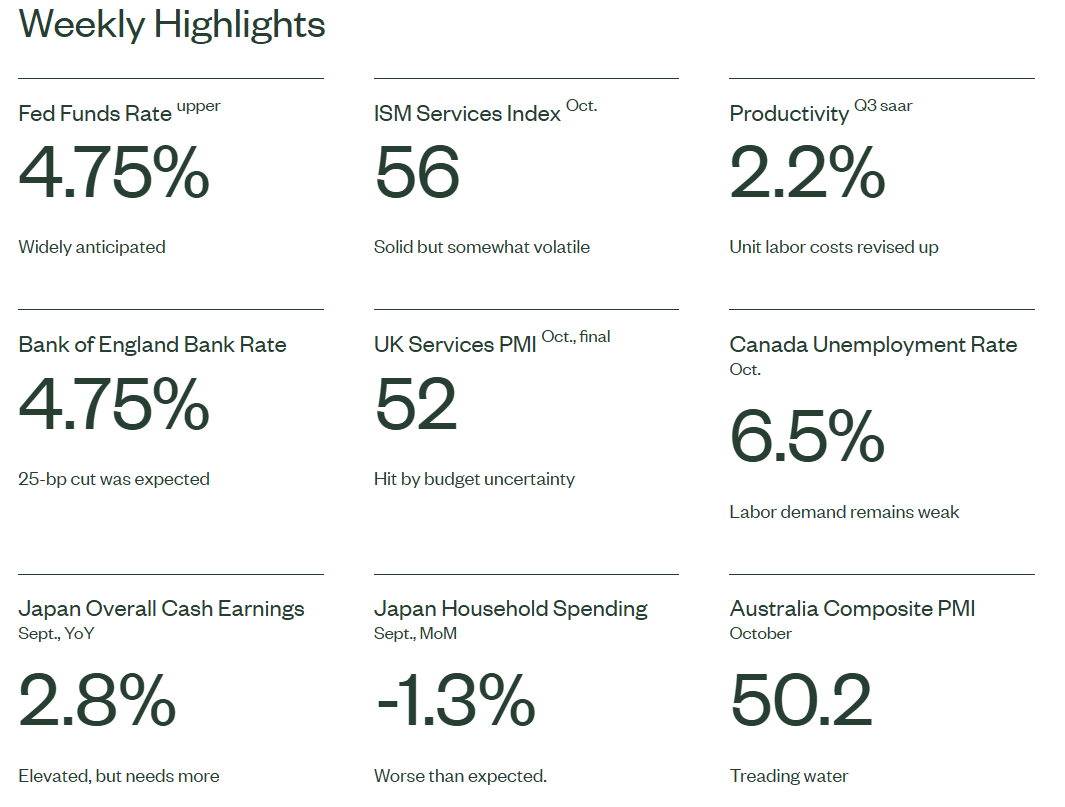

It is rare that a Fed meeting is not the main event during the week of its occurrence. But, when competing with general elections—as it did this round—there is no contest. So, the Fed’s well-anticipated 25-basis point cut had little impact on markets.

The big moves had already occurred in response to Republicans retaking the White House and the Senate and looking likely to eke out a narrow majority in the House of Representatives. Stocks soared and bond yields jumped. It is clear that the second Trump administration will come into office with a very strong mandate given wide margins of victory in both the electoral college and the popular vote. This would suggest a determined pursuit of policy changes in a whole range of areas, with investors particularly focused on trade, immigration, and fiscal policy. Campaign proposals on all these fronts are, without a doubt, directionally inflationary. Tariffs, deportations, and further tax cuts at a time when the budget deficit is already projected to consistently exceed 5% of GDP even on current law, all speak to the same outcome: higher inflation.

What is still very unclear is the magnitude of the inflationary impulse since we do notyet know exactly what policies will be a) proposed and b) approved. Timing matters:early, “all-in” action would be more inflationary, gradual with exceptions, less so.

Moreover, the very same policies can have very different effects depending on themacro context in which they are implemented. Take immigration, for example. Therewas a time in 2022 when the number of job openings exceeded the number ofunemployed by over 6.0 million; as of September, this measure of labor market supply tightness had shrunk to just 0.5 million. Other measures such as average weekly hours and the quits rate suggest the labor market is less tight today that itwas just prior to Covid, a view that Chair Powell expressed as well in the press conference. Deportations equate to a negative labor supply shock. But when they occur in a backdrop of declining labor demand, the ensuing inflationary impact mayprove to be fairly contained. Furthermore, immigration is not only a labor marketfactor. Yes, it raises labor supply, but it also increases demand for a range of items, specifically housing. A positive demand shock here in the context of inelastic supply is inflationary, a negative one could bring some relief. In conclusion: forecasting the ultimate outcome of all these potential policies is a highly uncertain exercise.

When asked about how policies changes may impact the economy and Fed policy,Chair Powell said the following: “we do not guess, we do not speculate, we do notassume” how policies may change. The Fed waits for actual proposals, then models possible scenarios, and decides afterwards if a change of course is needed. Ofcourse, markets are by their very nature going to speculate and seek to gauge the impact of as-yet-uncertain policy shifts. A lot of that has already happened (this is not to say there isn’t more to go). But the economy does not behave that way. And so,we intentionally hold back from making any big changes to the forecast at this time. We do agree that the scope for 2025 Fed easing has narrowed, but we do not believe it to have closed. We still see a 25 bp-cut in December, and at least three more similarly sized cuts in 2025.

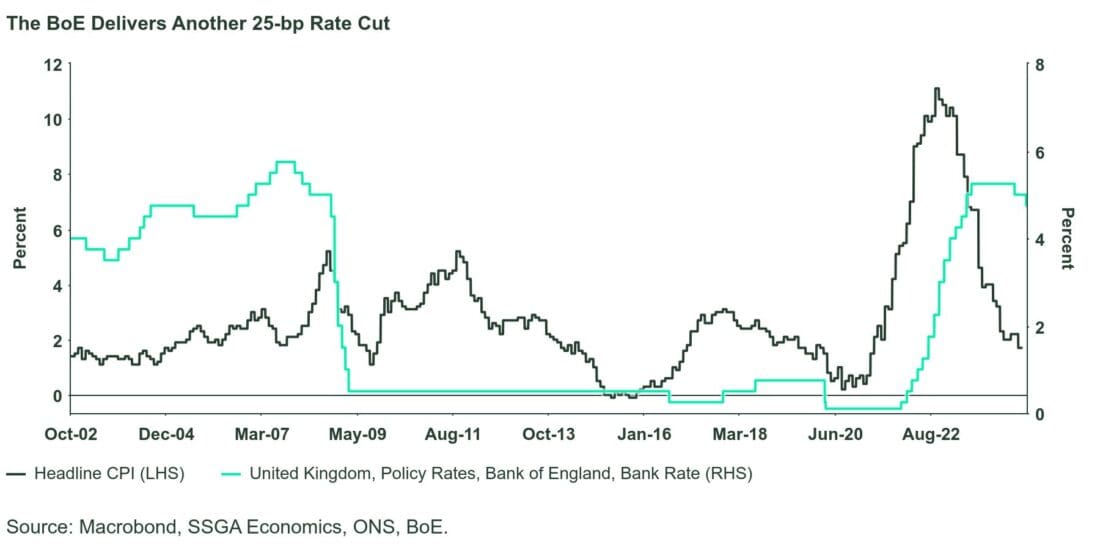

The Bank of England (BoE) lowered the policy rate by 25 bps to 4.75% as widelyexpected. The MPC votes were split 8–1, compared to 5–4 vote for August’s rate cut.The bank also confirmed a “gradual approach” to rate cuts, considering the impact of the latest Budget. None of this was surprising. The November cut was widely expected, and the market already concluded that large spending and front-loaded stimulus from the Budget would limit the scope of the rate cuts.

However, in our view, what was included in the bank’s November statement andmonetary report does not reflect the whole impact of the budget. Indeed, in the accompanying monetary report, the bank expected that the fiscal policy would lift GDP growth by “0.75% at their peak in a year’s time”, relative to August’s projections. CPI inflation was also boosted by “just under 0.5% at its peak” by theBudget. These estimates are based on the usual 15-day average of forward interest rates to 29 October, and completely ignore the yield spike following the Budget Announcement on 30 October. That said, the budget impact would have beenmore modest if the bank’s projections were based on the latest pricing.

The bank’s forecasts also included three scenarios with different degrees of inflationpersistence. The central forecast was based on the second scenario, which presumes the second-round effects of inflation dissipate more slowly than they emerged. The CPI inflation is forecasted to fall back to the 2% target over the medium-term in this scenario, conditioned on market interest rate expectations that bank rate will drop by around 100 bps to 3.75% by the end of next year.

The December rate cut which we previously expected not looks unlikely, but we would not rule it out completely. In addition, if services inflation continues to fall more meaningfully in coming months, rate cuts are still likely to accelerate early next yearand reach 3.5% – 3.75% by next summer.

Click here to read the full article

—

Originally Posted November 11, 2024 – Election Overshadows Fed’s Rate Cut

Disclosure

Marketing Communication

ssga.com

State Street Global Advisors Worldwide Entities

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of SSGA Economics Team through the period ended November 08, 2024 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

© 2024 State Street Corporation. All Rights Reserved.

2537623.262.1.GBL.RTL

Exp. Date: 11/30/2025

Do not reproduce or reprint without the written permission of SSGA.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

State Street Global Advisors and its affiliates (“SSGA”) have not taken into consideration the circumstances of any particular investor in producing this material and are not making an investment recommendation or acting in fiduciary capacity in connection with the provision of the information contained herein.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

COPYRIGHT AND OTHER RIGHTS

Other third party content is the intellectual property of the respective third party and all rights are reserved to them. All rights reserved. No organization or individual is permitted to reproduce, distribute or otherwise use the statistics and information in this report without the written agreement of the copyright owners.

Definition:

Arbitrage: the simultaneous buying and selling of securities, currency, or commodities in different markets or in derivative forms in order to take advantage of differing prices for the same asset.

Fund Objectives:

SPY: The investment seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500® Index. The Trust seeks to achieve its investment objective by holding a portfolio of the common stocks that are included in the index (the “Portfolio”), with the weight of each stock in the Portfolio substantially corresponding to the weight of such stock in the index.

VOO: The investment seeks to track the performance of a benchmark index that measures the investment return of large-capitalization stocks. The fund employs an indexing investment approach designed to track the performance of the Standard & Poor’s 500 Index, a widely recognized benchmark of U.S. stock market performance that is dominated by the stocks of large U.S. companies. The advisor attempts to replicate the target index by investing all, or substantially all, of its assets in the stocks that make up the index, holding each stock in approximately the same proportion as its weighting in the index.

IVV: The investment seeks to track the investment results of the S&P 500 (the “underlying index”), which measures the performance of the large-capitalization sector of the U.S. equity market. The fund generally invests at least 90% of its assets in securities of the underlying index and in depositary receipts representing securities of the underlying index. It may invest the remainder of its assets in certain futures, options and swap contracts, cash and cash equivalents, as well as in securities not included in the underlying index, but which the advisor believes will help the fund track the underlying index.

The funds presented herein have different investment objectives, costs and expenses. Each fund is managed by a different investment firm, and the performance of each fund will necessarily depend on the ability of their respective managers to select portfolio investments. These differences, among others, may result in significant disparity in the funds’ portfolio assets and performance. For further information on the funds, please review their respective prospectuses.

Entity Disclosures:

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

SSGA Funds Management, Inc. serves as the investment advisor to the SPDR ETFs that are registered with the United States Securities and Exchange Commission under the Investment Company Act of 1940. SSGA Funds Management, Inc. is an affiliate of State Street Global Advisors Limited.

Intellectual Property Disclosures:

Standard & Poor’s®, S&P® and SPDR® are registered trademarks of Standard & Poor’s® Financial Services LLC (S&P); Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones); and these trademarks have been licensed for use by S&P Dow Jones Indices LLC (SPDJI) and sublicensed for certain purposes by State Street Corporation. State Street Corporation’s financial products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates and third party licensors and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability in relation thereto, including for any errors, omissions, or interruptions of any index.

BLOOMBERG®, a trademark and service mark of Bloomberg Finance, L.P. and its affiliates, and BARCLAYS®, a trademark and service mark of Barclays Bank Plc., have each been licensed for use in connection with the listing and trading of the SPDR Bloomberg Barclays ETFs.

Distributor: State Street Global Advisors Funds Distributors, LLC, member FINRA, SIPC, an indirect wholly owned subsidiary of State Street Corporation. References to State Street may include State Street Corporation and its affiliates. Certain State Street affiliates provide services and receive fees from the SPDR ETFs.

ALPS Distributors, Inc., member FINRA, is distributor for SPDR® S&P 500®, SPDR® S&P MidCap 400® and SPDR® Dow Jones Industrial Average, all unit investment trusts. ALPS Distributors, Inc. is not affiliated with State Street Global Advisors Funds Distributors, LLC.

Before investing, consider the funds’ investment objectives, risks, charges, and expenses. For SPDR funds, you may obtain a prospectus or summary prospectus containing this and other information by calling 1‐866‐787‐2257 or visiting www.spdrs.com. Please read the prospectus carefully before investing.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from State Street Global Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or State Street Global Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!