- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 25, 2024 at 11:00 am

Markets are struggling for direction today following yesterday’s broadening which featured gains for the Dow and Russell amidst losses for the Nasdaq and S&P. Today’s action is just the opposite, as the technology and communication service trades recover while all other sectors endure losses. Rates and the dollar are rising against the backdrop, thanks to Fed Governor Bowman appearing reluctant to reduce borrowing costs while pushing the door for another hike slightly wider. Furthermore, news that price pressures rose much higher-than-expected north of the border in Canada also supported yields.

Federal Reserve Governor Michelle Bowman didn’t just push back her timeline for rate cuts this morning, rather she told an audience at the Policy Exchange in London that she’d consider lifting the benchmark if inflationary pressures don’t improve. The policymaker had previously said reductions this year would be inappropriate considering the strength of inflation. Bowman said the supply chain has improved and has already contributed to softening goods costs so it’s unlikely the trend will help to further price pressures. More restrictive policies on immigration could also support inflation by preventing additional workers from entering the country and alleviate a labor shortage that has fueled paycheck gains. Immigration is a bit of a mixed bag, however, because additional immigrants could drive up shelter costs with the country having a shortage of affordable housing.

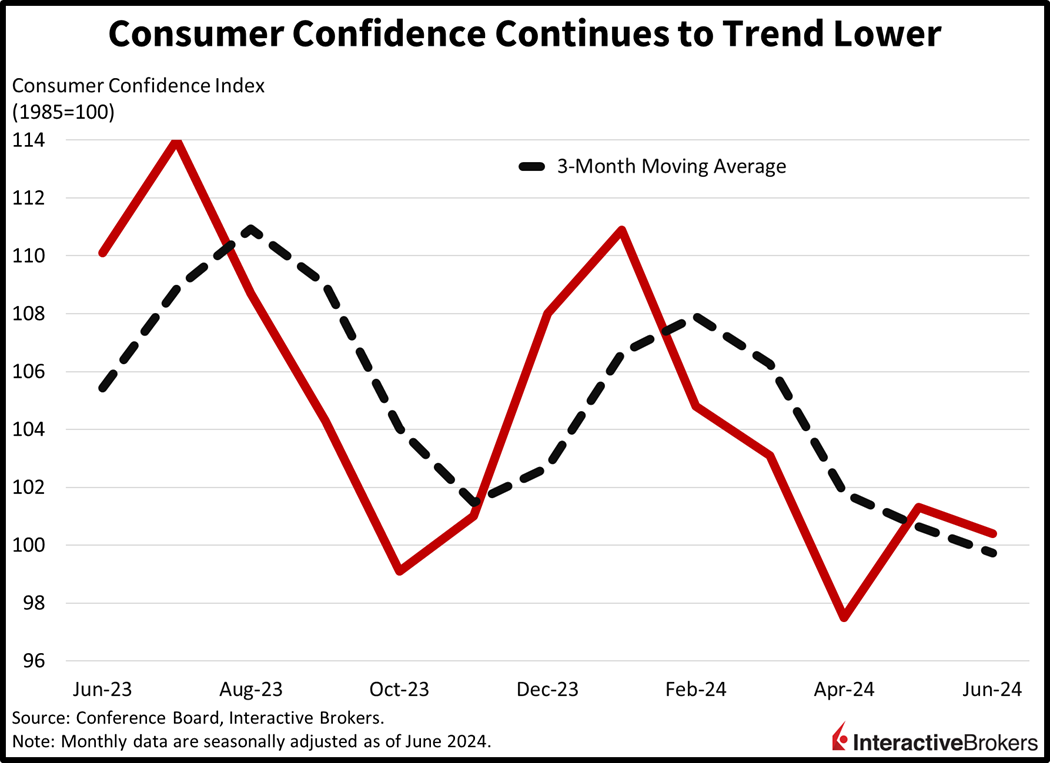

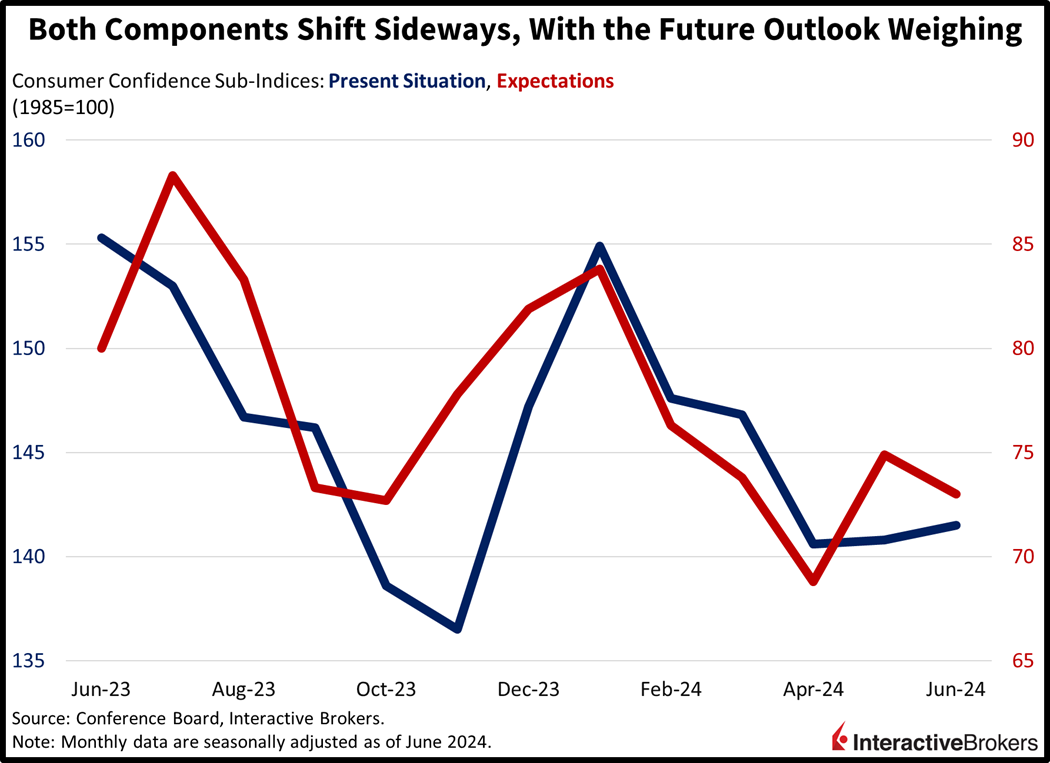

Households are increasingly worried about their future economic fortunes, which is weighing on consumer confidence even as the present situation gauge improves slightly, according to this morning’s Conference Board Consumer Confidence report. The benchmark fell to 100.4 this month from 101.3 in May but arrived higher than projections calling for 100. The Present Situation and Expectations sub-indices shifted in a bifurcated way, moving from 140.8 and 74.9 to 141.5 and 73, respectively. Folks are feeling better about current and future labor conditions but worse concerning present and future business opportunities, income possibilities ahead and their family financial situation now and in the future. Elevated grocery prices amidst stalling big-ticket purchasing plans continued to weigh on sentiment, but inflation expectations ticked modestly lower from 5.4% to 5.3% over the next twelve months. Finally, people were optimistic about the stock market, the path for lower borrowing costs and their vacation plans into year-end.

In an unexpected setback, Canada’s annual inflation jumped from 2.7% in April to 2.9% in May, causing investors to lower their expectations for a July rate cut to just 50%. Analysts expected the rate of price pressures to decline to 2.6%. On a month-over-month (m/m) basis, prices climbed 0.6%, twice the rate of the analyst forecast. Prices for rent, travel tours, air transportation and cellular communication services were the largest contributors to the headline number.

US home prices based on S&P CoreLogic set all-time records in April, but the pace of price increases moderated from the preceding month. Prices also climbed according to data from the Federal Housing Finance Agency (FHFA). On a year-over-year (y/y) basis, the 20-city S&P CoreLogic Case-Shiller house price index climbed 7.2% compared to the 7.5% increase for March. On a seasonally adjusted m/m basis, prices climbed 0.4%. Analysts expected a y/y increase of 7.0% and a 0.3% m/m increase. The national index also climbed substantially, jumping 6.3% y/y and 0.3% m/m. The national index gain also decelerated, having increased 6.5% as of March. Also this morning, the FHFA reported that home prices increased 6.3% y/y as of April and 0.2% m/m, which missed expectations for a m/m increase of 0.3%.

Markets are tilted bearishly with nothing working outside of the popular technology and communication services sectors. Yields and the dollar are bumping higher, effectively tightening financial conditions, while commodity majors are down across the board. Leading the charge lower are the Dow Jones Industrial and Russell 2000 benchmarks; they’re down 0.7% and 0.5%, respectively. The tech-heavy Nasdaq Composite and S&P 500 indices, meanwhile, are higher by 1% and 0.1%. While the technology and communication services sectors are gaining 1.4% and 0.6%, all other nine major segments are lower. Real estate, materials and industrials are taking the most pain, with the baskets down 1.6%, 1.2% and 1.1%. Treasury yields appear to be bottoming, with the 2- and 10-year maturities changing hands at pivotal support levels of 4.75% and 4.25%, 2 basis points (bps) loftier on the session. Rising rates and an incrementally longer journey across the monetary policy bridge are helping the dollar, pushing it up 19 bps as the greenback gains relative to all of its major, developed market counterparts, including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian dollars. Tighter central bank projections are weighing on the commodity space via lighter demand prospects, with silver, lumber, copper, crude oil and gold all pointing south by 1.8%, 1.3%, 1.2%, 0.7% and 0.4%.

The growth trade appears toppy following last Friday’s record options expiration, in which shareholders generally chose to not buy back their short calls, sending Nvidia into correction territory. Against that backdrop, yesterday’s action was quite interesting as folks tried to become motivated about the cyclical and small-cap trades. The issue is, however, that multiple expansion for the non-growth areas of the market carry such a high bar, as the companies truly lack exciting narratives that compel investors to pile in. Finally, with the S&P 500 1% below its record high of 5505, a level that coincides closely with the pivotal midpoint of 5500 and bullish sell-side year-end targets, the odds of a 10% correction to 5000 are rising.

Visit Traders’ Academy to Learn More About Consumer Confidence and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!