- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 17, 2025 at 5:07 am

By Todd Stankiewicz CMT, CFP, ChFC

1/ Uranium’s Next Big Move? The Charts Are Heating Up

2/ A Changing of the Guard? International Equities Show Signs of Leadership

3/ From Narrow to Broad: Is This the Breakup of the Magnificent 7?

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

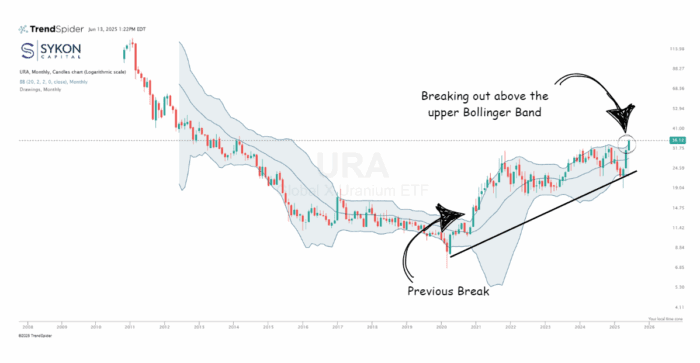

Uranium’s Next Big Move? The Charts Are Heating Up

Uranium may be breaking out from another multi-year consolidation, similar to the setup we saw in late 2020. These periods of price compression, often identified by narrowing Bollinger Bands, tend to precede strong directional moves. When the bands expand, price typically follows the direction of the breakout. Right now, that direction appears to be higher.

The last breakout in the Global X Uranium ETF (URA) occurred in December 2020 around $14/share and rallied to nearly $27. We’re now seeing a similar technical setup.

But this time, the fundamentals may be even stronger:

Put simply, the backdrop is more favorable than it was in 2020. If the breakout holds, uranium could be setting up for a move that’s not just technical, but structural.

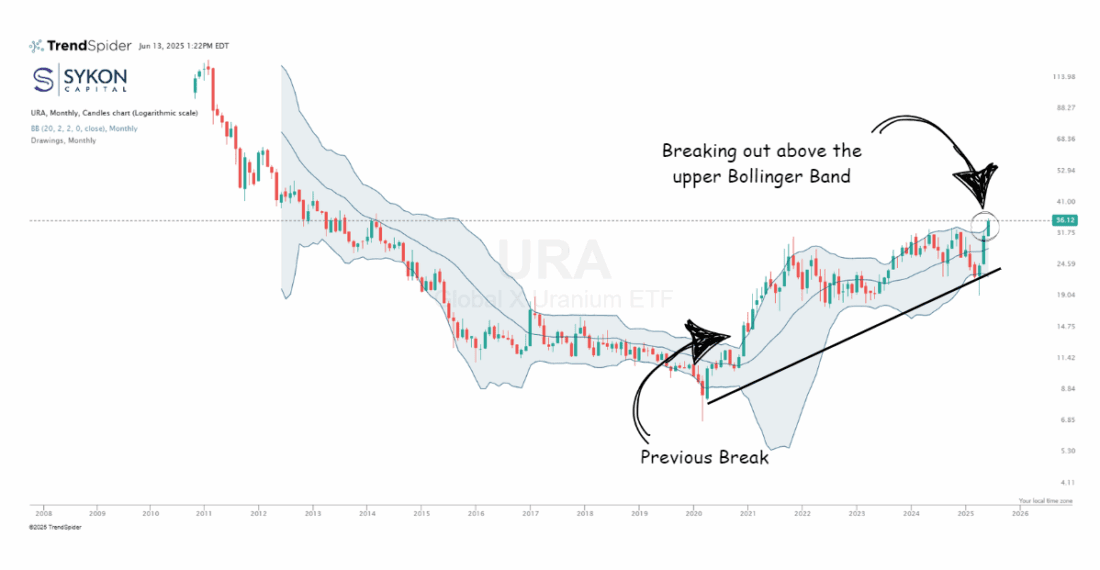

A Changing of the Guard? International Equities Show Signs of Leadership

Continuing our focus on structural market shifts, international equities may be quietly reclaiming a leadership role. A review of the monthly chart shows relative strength beginning to tilt away from U.S. equities, marking a possible inflection point after more than a decade of U.S. outperformance.

Since the end of the 2008 financial crisis, U.S. stocks have dominated global returns, driven by tech concentration, aggressive monetary policy, and the strength of the dollar. But those tailwinds are now turning into headwinds:

These aren’t just cyclical blips, there are likely signs of longer-term shifts. Leadership transitions like this typically play out over years, not quarters.

So it’s worth asking:

What if the next decade looks more like the early 2000s than the 2010s?

U.S. exposure may have been the right answer for the last cycle, but cycles change. And home bias is not a strategy.

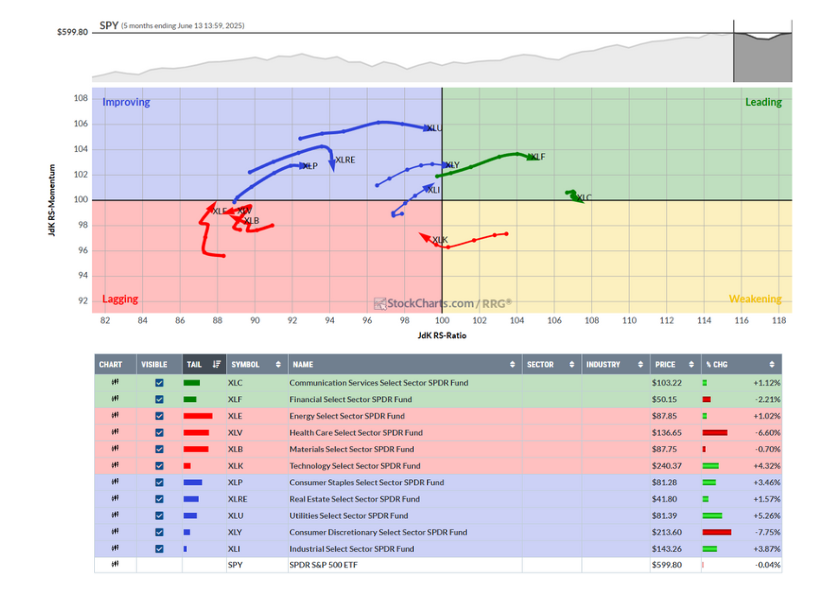

From Narrow to Broad: Is This the Breakup of the Magnificent 7?

For much of 2023 and 2024, markets were led almost exclusively by mega-cap technology stocks. But leadership driven by a narrow group is rarely sustainable. Earlier this year, I noted that after periods of extreme performance divergence, equal-weighted indices often begin to outperform their market-cap-weighted counterparts.

Now, we’re seeing early signs that this shift may already be underway.

Using Relative Rotation Graphs (RRGs), we can visualize how sectors cycle through phases of leadership. Stocks typically rotate clockwise through the four RRG quadrants: from green (Leading), to yellow (Weakening), red (Lagging), and eventually blue (Improving).

At the moment, we’re beginning to see a broad rotation.

This rotation suggests a meaningful broadening of market leadership, a departure from the concentrated tech-driven rallies we’ve become accustomed to. If this trend continues, more diversified strategies and equal-weighted exposures may take the lead from here.

What could be fueling this?

One potential driver: deregulatory tailwinds. Sectors with high regulatory burden, like financials, energy, and industrials, stand to benefit disproportionately from regulatory rollbacks, especially if policy continues to shift toward pro-business reform.

This isn’t just a technical development. It’s another potential structural shift in how markets allocate capital and where the next cycle of leadership may emerge.

Disclaimer: Advisory Services offered through Sykon Capital, LLC, a registered investment advisor with the U.S. Securities and Exchange Commission. This material is intended for informational purposes only. It should not be construed as legal or tax advice and is not intended to replace the advice of a qualified attorney or tax advisor. The information contained in this presentation has been compiled from third party sources and is believed to be reliable as of the date of this report. Past performance is not indicative of future returns and diversification neither assures a profit nor guarantees against loss in a declining market. Investments involve risk and are not guaranteed.

—

Originally posted 16th June 2025

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!