- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 1, 2024 at 9:26 am

1/ The Market Leads the Fed

2/ This Will Impact Credit Markets

3/ This Will Impact Equity Rotation

4/ Equity Sectors Saw this Coming

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

For full disclosure, I am writing this before the FOMC press conference today. I feel comfortable doing so because the odds the FOMC moves rates on July 31 are very close to zero. The FOMC does not like to surprise the markets. There are, however, strong odds the FOMC will cut in September and that is what the market will focus on in the press conference.

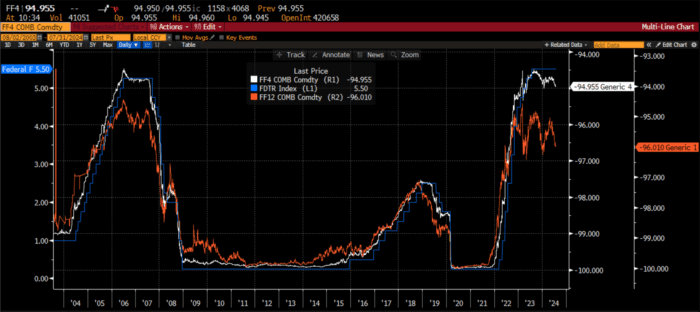

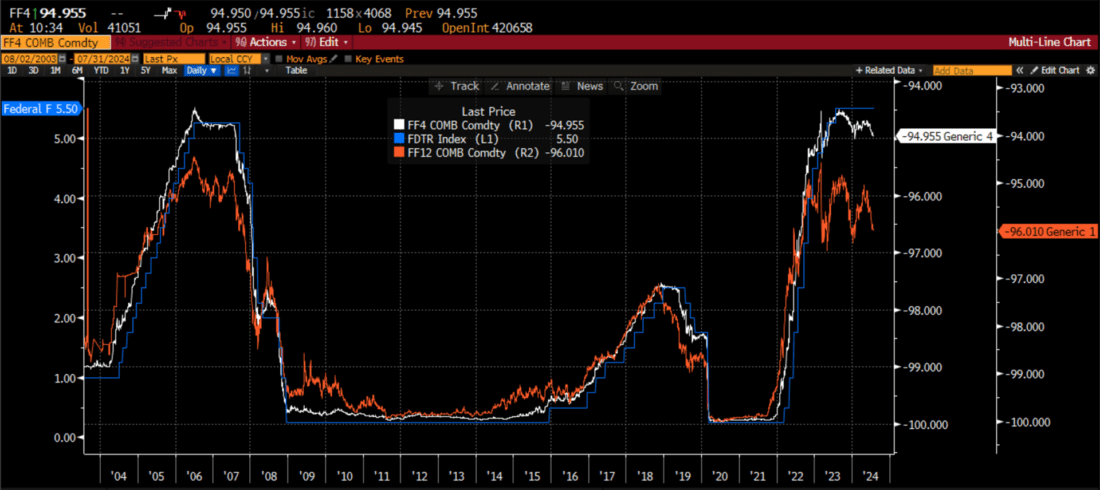

Source: StayVigilant.Substack.com, Bloomberg

However, we already know what the FOMC will say and what it will do. Why? Because while many people think the market reacts to the FOMC, the reality may be more that the FOMC reacts to the market instead. In the first chart I show you three lines: Fed Funds in blue, 4-month ahead Fed Funds Futures in white, and 12-month ahead Fed Funds Futures in orange.

As we look at it, we can see the Fed Funds Futures market has led the short-term Fed Funds and the Fed Funds Target rate for the last 20 years. Even the shorter term 4-month future leads the Target rate for the Fed. Both futures (inverted here as it is price and not yield) are telling us where the Fed Funds will be: in 4 months at 5.05% vs. 5.5% for the Target now and in 12 months at 3.99% vs. 5.5% currently (100-price is yield). That is some dovishness.

We can then use the 12-month ahead Fed Funds Future to see if different market components similarly respond to this market pricing mechanism. The first market I look at is the credit market, comparing the HYG high yield ETF to the LQD investment grade ETF. Throughout my career, I have learned that the credit markets lead the equity markets so I always pay attention.

Source: StayVigilant.Substack.com, Bloomberg

As rates have moved higher (inverted white price line of Fed Funds Futures moving up), one may think that the riskier credit – high yield – would underperform the safer credit – investment grade. This makes perfect sense until one realizes that when looking at these two ETFs there are two other forces that overwhelm that influence. First, the duration of the HYG ETF is much shorter than for LQD by nature of the shorter-term issuance that HY companies do. Second, a smaller impact being the sector composition as HYG has a lot of media and energy and LQD has banks and telecom.

We can see that as this inverted futures price line has fallen i.e. yields have fallen, investors have preferred LQD over HYG, extending out the duration of their portfolio. When yields have risen (price has fallen), investors have preferred shorter duration. Will investors move more permanently into longer duration?

Duration is something that not only credit markets have but equity markets have as well. If you think about it, it makes sense. Duration is the sensitivity to interest rates. Any asset that generates cash flow has less sensitivity. Assets where the value is placed more on the future of cash flows, will have a longer duration. This is true for companies, sectors and countries.

Source: StayVigilant.Substack.com, Bloomberg

The next comparison for Fed Funds Futures is the outperformance of the US vs. the rest of the world. Believe it or not, the US market is seen as the defensive market across the globe. I know that is hard to think of in a market driven by AI. However, the US market has a much lower correlation to the economy than others around the globe. In addition, the cash flow, especially of the largest companies, is much higher. Thus the US has a shorter duration.

We see this in the performance. As rates have moved higher, investors have sought the safety of the US. When rates are anticipated to move lower, the rest of the world starts to outperform. If we are about to see a long Fed easing cycle, is it finally time for the rest of the world to outperform the US? Will US investors start to move their money offshore?

Finally, rate expectations also have an influence on sector allocation. The duration argument is certainly at play here as is the preference and performance of the individual companies within the sector. The example I show here is the XLP Consumer Staples ETF compared to the XLY Consumer Discretionary ETF. This can be thought of as defensive vs. cyclical or safe vs. risky.

Source: StayVigilant.Substack.com, Bloomberg

There is a large idiosyncratic component, though, too. The XLP ETF is heavily weighted toward Proctor & Gamble, Costco, and Walmart. The XLY ETF is weighted toward Amazon and Tesla. Thus, when rates first started to rise back in 2022, we can see the investor preference for defensive vs. cyclical stocks as XLP materially outperformed XLY.

However, in the late summer rally of 2023 that has continued throughout 2024, we see the investor preference for the Mag & names with Amazon and Tesla leading the way. Rates moved higher but these sector ETFs did not respond in kind. Thus, we need to be careful if we think that XLY will naturally outperform on lower rates because a lot of that relative move may have already happened.

We are predisposed to think that Fed policy impacts the markets, however, the empirical evidence suggests more that the FOMC may follow the market, and the internal relative performance of the market may give us a better insight into investor forward views than the headline indices do. Stay Vigilant!

About This Week’s Author

Rich Excell, CFA, CMT is a 30-year hedge fund and proprietary trading veteran who has lived and worked in Asia and Europe in addition to the United States. He has run investment businesses spanning equities, fixed income, commodities and foreign exchange. Rich is now a Clinical Assistant Professor of Finance at the Gies College of Business, University of Illinois, Urbana-Champaign. He also is the host of the Investment Exchange Forum and Macro Matters podcasts for the CFA Society Chicago and writes a bi-weekly options trading blog ‘Excell with Options’ for the CME Group. Finally, he writes a weekly Substack blog called ‘Stay Vigilant’ which aims to demystifinance for the average investor.

—————————————-

Originally posted on August 1st, 2024

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Municipal Bonds are only available from Interactive Brokers for IBKR LLC, IBKR Canada, IBKR Hong Kong, IBKR Australia and IBKR Singapore entities.

Related Articles

for Daily Seasonal Data")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!