- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 7, 2026 at 9:10 am

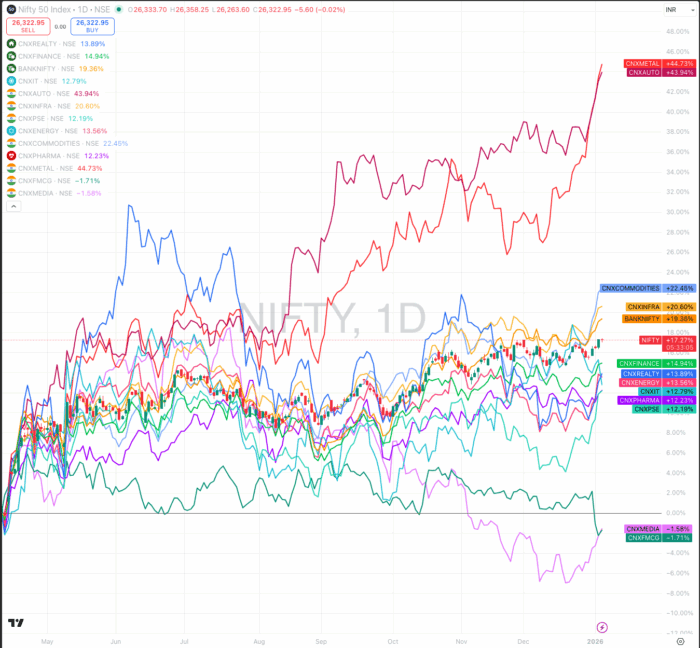

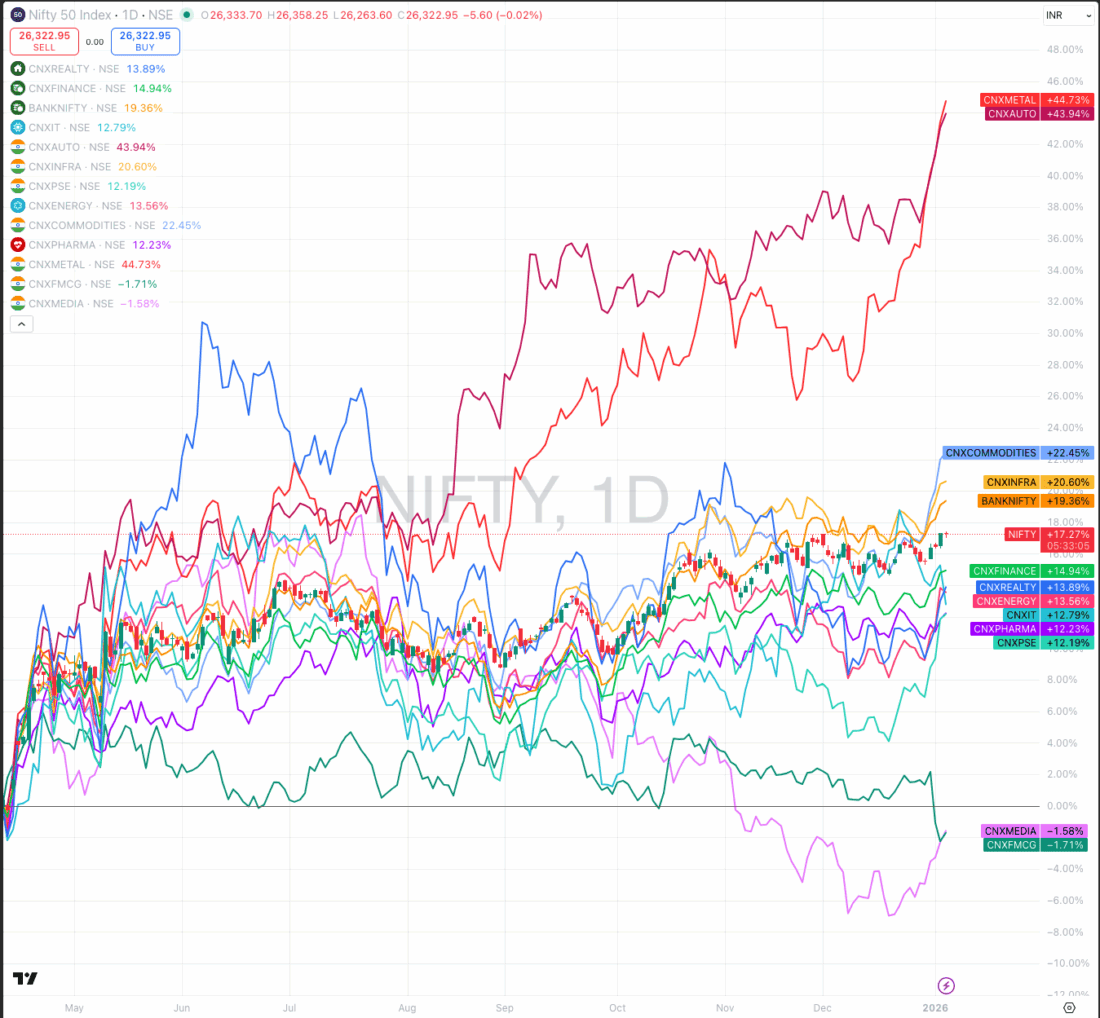

1/ The 9-Month Leaders: Holding the Line

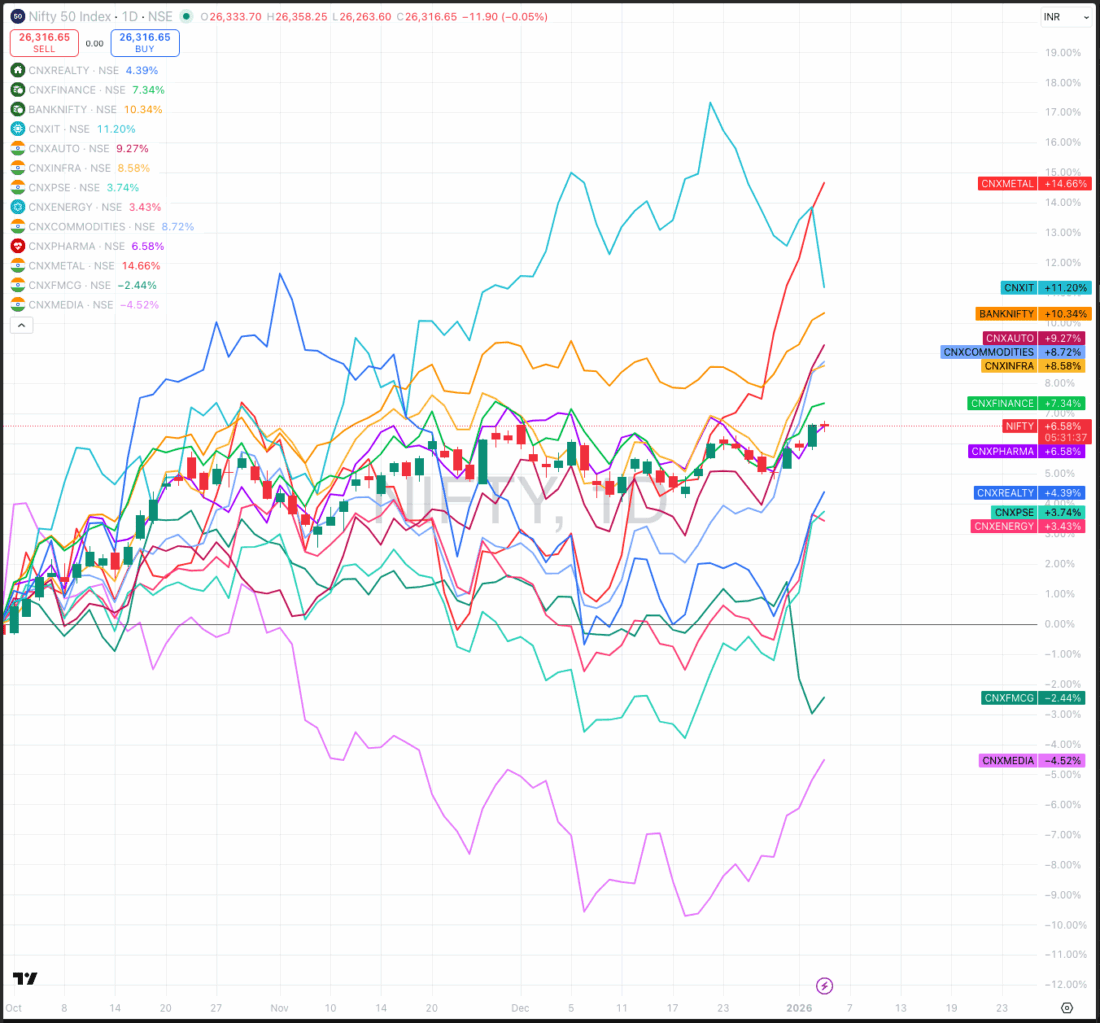

2/ The 3-Month Turnaround

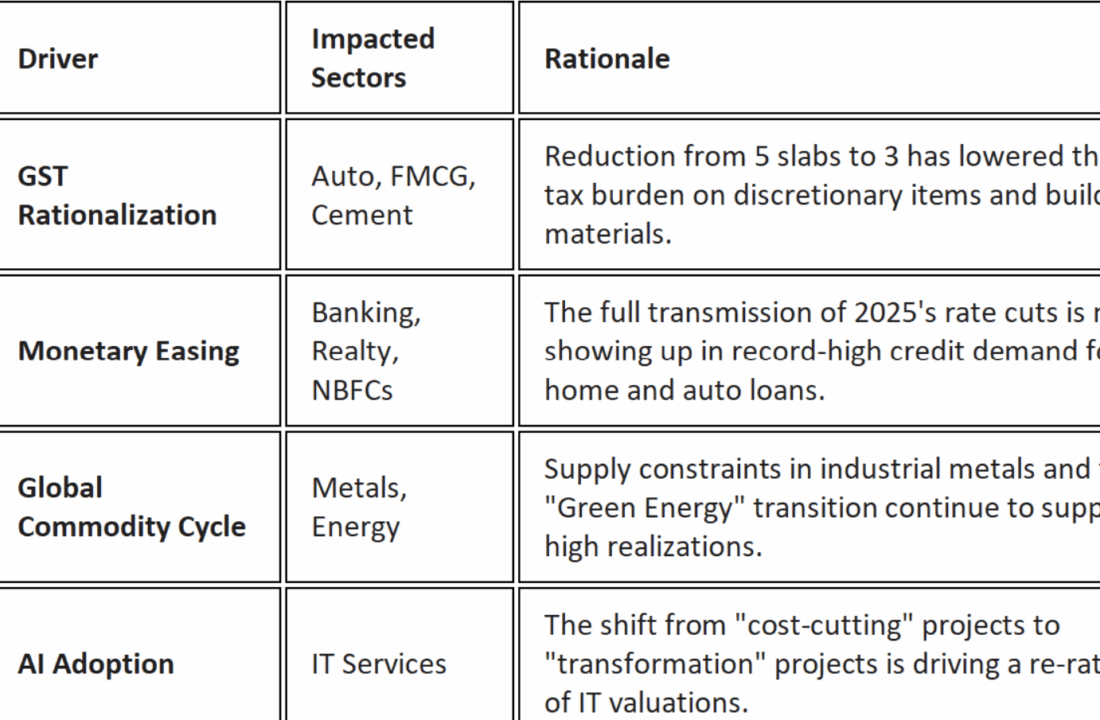

3/ Key Drivers for the Next 3–6 Month

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

In a top-down approach for the Indian markets, identifying sectors poised to outperform the index over the next 3–6 months is critical. While 2025 was defined by volatility, early 2026 shows clear signs of sector rotation as capital moves from overheated segments into turnaround stories.

The 9-Month Leaders: Holding the Line

Looking at the 9-month Relative Strength charts, the heavy lifting for the index has been driven by two primary pillars:

While Bank Nifty (19%) and Infrastructure (20%) have outperformed the benchmark, their growth has been more measured as the market prices in the 125 bps cumulative repo rate cuts seen throughout 2025.

The 3-Month Turnaround

The New Drivers

The most significant shift is visible on the 3-month charts, where capital is rotating into previously “beaten-down” sectors:

The Laggards

Key Drivers for the Next 3–6 Month

Conclusion

The “easy money” phase of the index rally is transitioning into a phase where alpha will be generated by identifying the outperforming stocks within these turnaround themes.

The Playbook: Focus on quality leaders in IT and Banking that show improving Net Interest Margins (NIMs), and stay overweight on Metals as long as global industrial demand remains resilient. For the discretionary theme, look at Auto Ancillaries which are benefiting from both the GST cuts and the localized manufacturing push.

—

Originally posted 07 January 2026

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!