- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 28, 2025 at 12:40 pm

Stocks are recovering from yesterday’s AI induced debacle on the back of a continued surge in business investment following election day. And as investors witness momentum with capital expenditures, they’re also carefully analyzing fourth-quarter earnings and patiently awaiting results from mag7 members later this week as well as an update from the Federal Reserve tomorrow afternoon. Meanwhile, Treasurys are paring much of yesterday’s gains on a heightening in President Trump’s tariff rhetoric, which is sending the greenback, commodities and inflation expectations north. Furthermore, this morning’s consumer confidence figure posted a miss, as employment uncertainty, elevated costs and mounting price pressure projections weighed on household optimism.

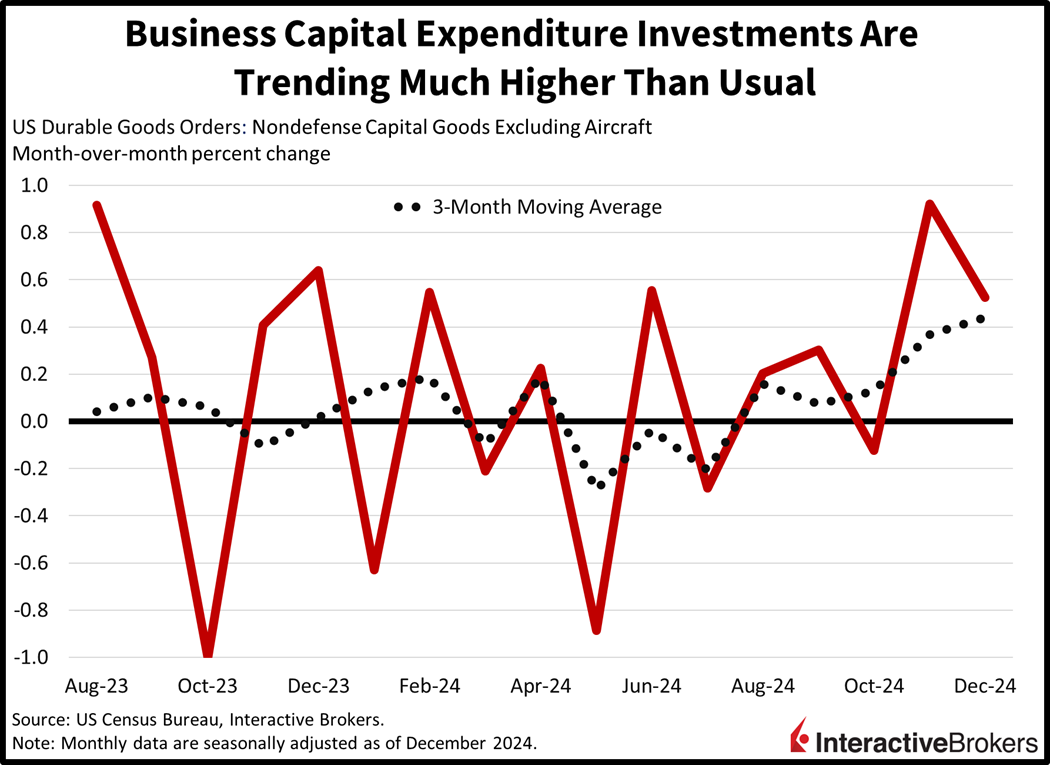

November’s surge in capital expenditures continued last month with the 3-month moving average rising at the fastest pace in over two years, marking a 28-month high. Nondefense capital goods orders excluding aircraft, a proxy for business investment provided in the monthly durable goods report from the US Census Bureau, rose 0.5% month over month (m/m) in December, exceeding the 0.3% median estimate but decelerating from the prior month’s 0.9% jump. From a broader perspective, however, overall durable goods purchases took a dive, dropping 2.2% m/m and missing the 0.6% projection while accelerating south from November’s 2% decline. The weakness stemmed from passenger airplane orders contracting 45.7% m/m amidst more modest decreases as follows:

Other categories that strengthened and the amount of their expansion included the following:

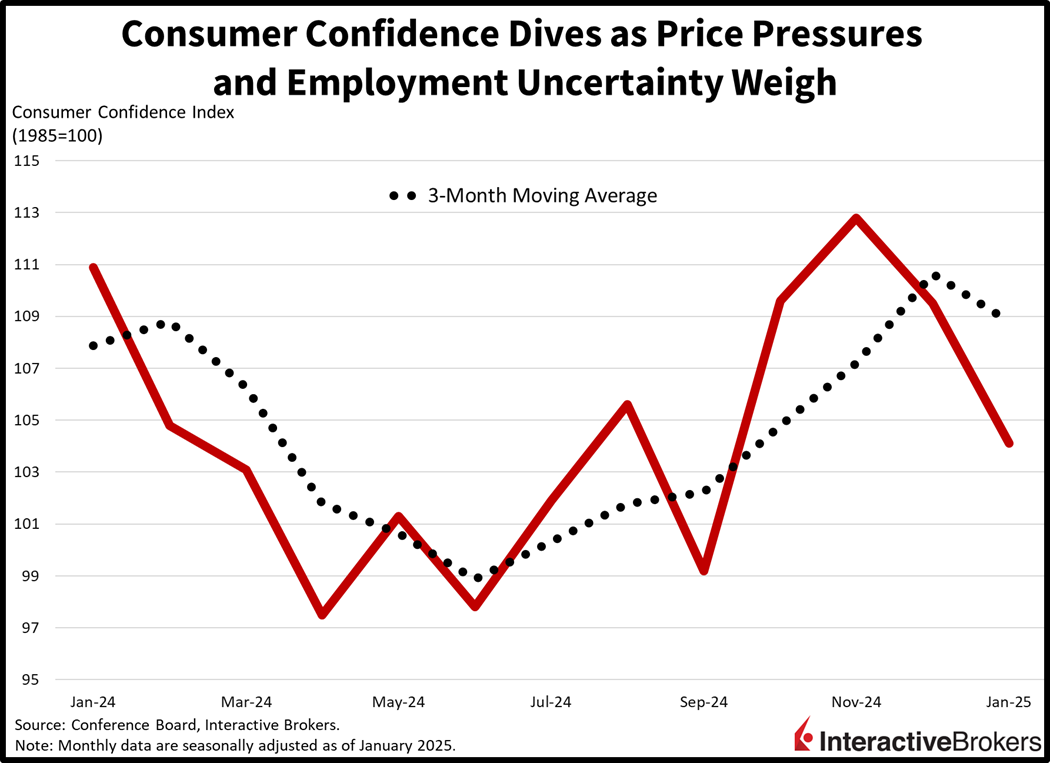

Business optimism and investment are trending upward, but household sentiments have moved the other way, albeit modestly, with this morning’s consumer confidence print adding further evidence to the bifurcation. Elevated prices and rising pessimism about employment and business conditions led to a miss in this morning’s report, as this month’s Conference Board’s Consumer Confidence Index retreated to 104.1, arriving beneath the anticipated 105.6 as well as the prior period’s 109.5. The present situation and expectations indices both contributed to the decline, decreasing from 144 and 83.9 to 134.3 and 86.5 m/m. An uptick in 12-month inflation expectations from 5.1% to 5.3% also led to a drop in folks believing that interest rates would descend. Moreover, not one of the five major components of the survey improved.

A pair of regional Fed surveys pointed to a slower contraction in manufacturing conditions within the central bank’s Richmond district and a deceleration in services momentum for the Dallas district. The former gauge rose from -10 in December to -4 this month, but weaknesses in new orders, shipments and backlogs were countered by buoyant expectations about the future. For the latter indicator, lighter consumption, slower hiring and tall prices weighed on the headline. It fell from 10.8 to 7.4. Similarly, however, business optimism countered some of the sluggishness in other areas.

The strength of earnings reports this morning varied within manufacturing and consumer-focused segments as illustrated by the following fourth-quarter highlights:

Australian businesses strengthened their views of economic conditions in December and sentiment has almost returned to the long-term average as depicted by data from the National Australia Bank (NAB). The uptick was an improvement from the decline in November. During 2024’s final month, the bank’s conditions gauge climbed 3 points to +6. Improvements occurred in most sectors with the retail group entering positive territory but still trailing other categories. It was the first positive reading for the retail category since November 2023. Conversely, conditions are the strongest in the service sector. Also in December, business confidence climbed 1 point to -2, well below the long-term average. Confidence in the retail sector exhibited the largest gain while mining and construction experienced the most significant declines.

Singapore’s producer prices for goods reversed a four-month y/y decline in December and recorded a 2.3% y/y increase, according to the Singapore Manufactured Product Price Index (SMPPI). In November, the benchmark fell 4.0% y/y. On a m/m basis, the SMPPI climbed 5.8% during the last month of 2024 after having advanced 1.6% in November. The m/m gain was driven by a 6.8% increase in non-oil items with the petroleum category dipping 0.1%. Price gains were led by the machinery and transport category with higher prices for electrical equipment. In a related matter, import prices fell 3.6% y/y but climbed 1% m/m. Export prices descended 3.1% y/y while strengthening 0.6% m/m.

Equities are taking back roughly half of yesterday’s losses as market participants look ahead to critical corporate earnings results, the Fed meeting and incoming economic data later this week, including GDP, the Employment Cost Index and the central bank’s preferred inflation gauge. But a return to aggressive rhetoric on the trade front from President Trump is weighing on Treasurys while propping up commodities and the greenback.

All major domestic stock benchmarks are trading north with the Nasdaq 100, S&P 500, Dow Jones Industrial and Russell 2000 indices up 1%, 0.7%, 0.5% and 0.1%. Sector breadth is tilted to the downside, however, with just 4 segments moving higher and led by technology, communication services and financials; they’re up 1.5%, 0.5% and 0.2%. Utilities, real estate and energy represent today’s laggards; they’re losing 2%, 0.8% and 0.8%. Turning to fixed-income, currencies and commodities, a lift in tariff concerns is weighing on bond performance, with the 2- and 10-year Treasury maturities changing hands at 4.22% and 4.58%, 3 and 4 basis points (bps) heavier on the session. There is a $44 billion offering of 7-year notes this afternoon, by the way. Pricier borrowing costs are helping the US tender, with the Dollar Index up 48 bps as the greenback appreciates versus all of its major counterparts, including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian contemporaries. Increasingly fearful of disruptions to global commerce, commodity investors are bullish, resulting in gold, crude oil, silver and copper gaining 0.6%, 0.4%, 0.4% and 0.2%.

Today’s bifurcated market action reflects how Trump bumps can affect different asset classes in distinct ways. Recent increases in Trump’s tariff threats include imposing meaningful across-the-board levies well in excess of 2.5%, with some anecdotal evidence pointing to 20% as the potential number. Meanwhile, Mexico and Canada may be served with import duties of 25% as soon as this Saturday. Against this backdrop, nervousness has been building in Latin America following President Trump’s quarrel with Colombia’s President Gustavo Petro, as the latter acquiesced to receiving deportees after being dealt with a 50% tariff warning. Finally, an increase in international agreements with Washington will serve to ease borrowing costs, stabilize the greenback and provide a supportive environment for equities. More clashes, on the other hand, will offer just the opposite, dealing investors with Trump bumps.

Chief Strategist Steve Sosnick and Senior Economist José Torres like the “Yes” Forecast Contract for final fourth quarter US GDP growth coming in above 1.9%. While we will receive a preliminary view of the result this Thursday, this contract settles on March 27 when the final figures are released. The “Yes,” currently priced at $0.67, pays out a dollar if correct.

Source: ForecastEx

To learn more about ForecastEx, view our Traders’ Academy video here

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

for Daily Seasonal Data")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!