- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 6, 2024 at 12:22 pm

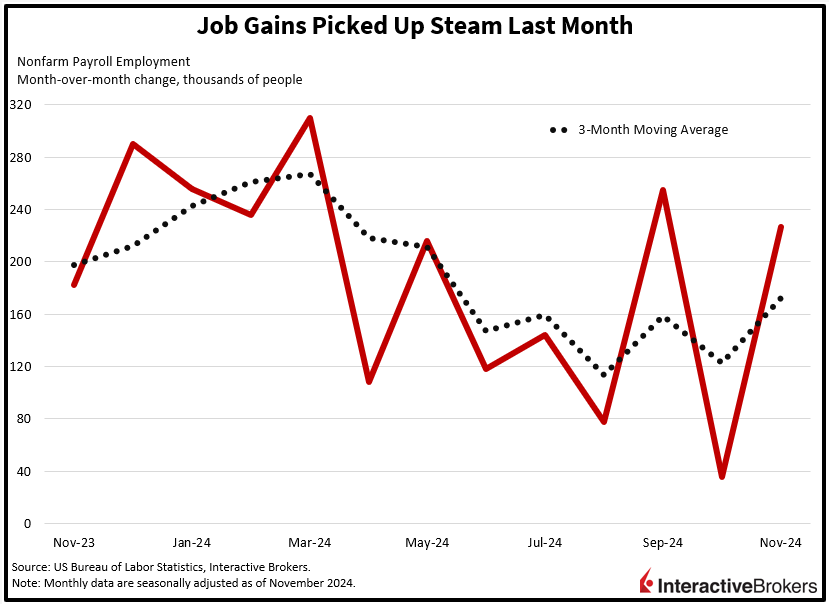

This morning’s Jobs Report depicted a labor market that recovered strongly from the adverse effects of two hurricanes and the Boeing labor strike in October. But while roster expansions and paycheck levels arrived ahead of expectations, rate watchers are focusing on the unemployment rate ticking northward and are dialing up the probability of a 25-bp cut by the Fed in less than two weeks. In response, the IBKR ForecastTrader market carries odds of 84% of a rate reduction. Meanwhile, a faster walk down the monetary policy stairs is music to the ears of equity and fixed-income investors, who are stepping up to the plate to do some buying. The enthusiasm is justified by a solid economy that can continue to support earnings growth alongside a central bank that appears satisfied with current inflation trends. Furthermore, a stronger-than-expected Consumer Sentiment print is also propelling confidence.

Source: ForecastEx

Payroll additions last month climbed significantly from October, when hurricanes and the Boeing union strike depressed hiring. in a related matter, wages continued to grow while an increase in the unemployment rate is sustaining optimism for a Federal Reserve rate cut during the central bank’s December 18 meeting. Last month, payrolls rose by 227,000, a large increase from the upwardly revised 36,000 in October, according to the Bureau of Labor Statistics’ Employment Situation Report. Analysts anticipated an increase of 214,000. In recent months, non-cyclical sectors and services have led job creation and November was no exception. The private education and health services category, with 79,000 new workers, was the strongest contributor to payroll additions, followed by leisure and hospitality at 53,000 and government at 33,000. Conversely, retail trade surrendered 28,000 positions. The motor vehicles and parts category, non-durable goods group, and utilities sector also lost jobs, but to lesser degrees. However, after losing jobs in September and October, manufacturing bounced back, adding 26,000 positions as the Boeing strike wound down. The gain occurred despite the weakness in the manufacturing group’s nondurable goods and motor vehicles categories.

After increasing 0.4% month over month (m/m) in October, wages in November grew at the same pace and exceeded the expected 0.3% rate. Paycheck gains on a year-over-year (y/y) basis were also unchanged at 4.0% and were 10 basis points (bps) hotter than estimates. In another matter, the labor participation rate declined marginally from 62.6% in October to 62.5%, falling below the forecast of 62.7%. In November, 368,000 individuals left the workforce. The decline caused the unemployment rate to increase from 4.1% to 4.2%. Meanwhile, the November average hourly work week increased from 34.2 hours in October to 34.3, matching the analyst forecast.

The University of Michigan Consumer Sentiment Index for December hit 74.0, up from 71.8 in the preceding month and above the 73.1 expected by analysts. While the gauge of consumer expectations fell from 76.9 to 71.6, the current conditions benchmark jumped from 63.9 to 77.7. Consumers increased their outlook for inflation during the next 12 months from 2.6% to 2.9%, surpassing the 2.7% estimate. For the five-year period, consumers expect inflation to be 3.1%, matching the analyst outlook and down from 3.2% in November.

DocuSign (DOCU), which provides digital contract technology, grew its billings 9% year-over-year in the third quarter, an increase from the 2% rate in the preceding reporting period. For the recent quarter, both revenue and earnings surpassed Wall Street forecasts. CEO Allan Thygesen says client acceptance of the company’s artificial intelligence-enabled Intelligent Agreement Management platform was stronger than anticipated. The company’s full-year guidance exceeded analyst expectations and DocuSign shares jumped approximately 15% following the earnings release. AI also drove results for HP Enterprise (HPE). The company reported a 32% y/y increase in server revenue, with sales results driven by AI spending. More broadly, its adjusted earnings per share climbed 15.6% y/y. In the recent quarter, earnings and revenue came in above analyst forecasts. HP Enterprise anticipates earnings per share to range from $0.47 and $0.52 on an adjusted basis for the current quarter. Analysts anticipated guidance of $0.48.

In the retail sector, Lululemon’s (LULU) earnings and revenue exceeded expectations, with the impact of slowing sales in the Americas being offset by acceleration abroad. The company’s international sales soared 33% but increased only 2% in the Americas. CEO Calvin McDonald said the company is pleased with the start of the holiday shopping season and provided fourth-quarter sales and revenue guidance with upper ranges that surpassed analyst outlooks. Shares of Lululemon jumped roughly 9% following the earnings announcement. Petco Health + Wellness (WOOF) trimmed its loss per share from $0.05 to $0.02. Analyst anticipated a loss per share of $0.04. Revenue also exceeded the consensus estimate. Its shares climbed 5% in pre-market trading.

The rise in consumer sentiment and a solid labor market, as illustrated by today’s reports, point to favorable conditions for equity investors. With consumption representing more than 70% of GDP, the improving sentiment and expanding payrolls could help sustain corporate earnings. At the same time, optimism for the Fed to ease further on December 18 is providing another tailwind for equities.

To learn more about ForecastEx, view our Traders’ Academy video here

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

AS pointed out you hespecially after ave STRONG growing economy, labor market, and consumer confidence- where is the need/justication for a rate cut, especially after the uncalled-for Biden .50 cut in Sept? The only real factor holding inflation back has been the low energy/oil which Poweel always ignores when it has moved against him. Watch him cite that now as a factor.