- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 30, 2025 at 9:45 am

Investors have been told to worry if Kevin Hassett becomes Fed chair, but the market doesn’t appear concerned.

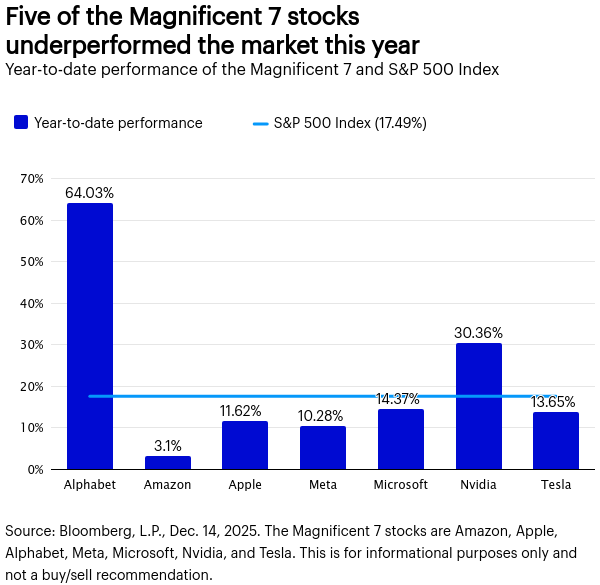

Many assume that the market’s success hinges on the Magnificent 7 stocks, but five lagged the S&P 500 so far this year.

Will rate cuts lower mortgage rates? The US 10-year Treasury, fed funds, and mortgage rates suggest that they may stay over 6%.

“I love when they drop the ball in Times Square. It’s a nice reminder that we all dropped the ball at some point this year.”1 Hopefully, Above the Noise didn’t drop it too often. In fact, we spent some time looking back to see what we focused on most throughout the year.

Here’s what rose to the top, and what we said about each theme along the way:

Macro signals, including tight credit spreads2 and loose lending standards,3 point to low near‑term recession risk.

A moderating US dollar4 and shifting global cycles favor diversification into non‑US assets, with Europe and emerging markets offering relative value.5

Tariffs and policy uncertainty could create a one‑time price shock and dampen sentiment and business investment, but are unlikely to trigger a recession in our view. Trade policy clarity plus US Federal Reserve (Fed) easing may be the remedy.

Anchored inflation expectations6 and the Fed’s easing bias provide a supportive backdrop for risk assets.

Should we pause for a long-distance dedication?

Finally, the biggest focus for Above the Noise in 2025 (drum roll):

Artificial intelligence (AI) spending is substantial, in our view, but not a dot‑com replay;7 valuations are elevated, yet poor timing tools,8 and market breadth is broadening beyond megacaps.9

Not bad. To paraphrase Casey Kasem, we’ll keep our feet on the ground and keep reaching for the stars.

…the market doesn’t appear particularly concerned about the next Fed chair. Investors have been told to worry about Kevin Hassett stepping into the role. After all, he would be the first to come directly from a senior White House position without prior service as a Fed governor. That sounds unprecedented, but remember that Ben Bernanke and Janet Yellen both chaired the Council of Economic Advisers before serving as Fed governors and then chairs.

So, is the market worried? Stocks are near record highs.10 Inflation expectations have remained contained.11 The dollar stabilized months ago.12 In short, there’s not much anxiety.

Why?

This isn’t to say that Fed independence isn’t critical. It is. But this may end up being little more than a tempest in a teapot.

Much has been made of a recent MIT study claiming AI can replace 12% of US jobs.14 Sounds terrifying, right? But it doesn’t mean AI is about to wipe out 12% of the workforce tomorrow. What it really means is that AI has the capability to perform roughly 12% of the tasks in your job. That’s not doom and gloom. That’s efficiency. AI can help me write paragraphs, edit my work, and even run analysis. But it doesn’t share my opinions or replicate my incredible wit (my mom swears I have it). It doesn’t hop on planes to meet clients. It certainly doesn’t flash my dazzling smile on TV (again, mom’s words). So, does AI have the skills to do 12% of my job? Sure. But that headline was way scarier than reality.

Investors often view the Magnificent 7 stocks as a single, unified force, assuming they move in lockstep and that the broader market’s success depends on their leadership. This perception is understandable given their outsized weight in major indexes,15 but it oversimplifies reality. In fact, the narrative doesn’t match the numbers. Most of these stocks are underperforming the S&P 500 this year.16 Meanwhile, the Bloomberg S&P 500 ex-Magnificent 7 Index has gained more than 16%,17 underscoring that market strength has been far broader than the story suggests.

“The word ‘affordability’ is a con job by the Democrats.”18

– President Donald Trump

“A lot of that is not the current rate of inflation. A lot of that is just embedded higher costs due to higher inflation in 2022 and ’23”19

– Fed Chairman Jerome Powell

I think they’re saying the same thing. President Trump would be right to remind voters that inflation spiked during the Biden administration, though in fairness, both parties contributed by pumping money into the system during and after the pandemic. Powell is also correct that inflation peaked in 2022.20 It’s the embedded higher costs that are the crux of the issue.

Policymakers focus on the inflation rate, while American consumers tend to focus on actual prices. And prices have remained elevated, about 10% higher than when inflation peaked.21 That translates to roughly 3% a year, which the nation’s central bankers are considering, for the most part, to be price stability. The challenge for politicians is that driving prices lower can’t be the goal. Deflation would be disastrous, triggering falling wages, collapsing demand, and further declines in prices. That’s a vicious cycle. Instead, what we need is for wages to keep pace. The data suggests they have, at least in aggregate,22 but many Americans clearly don’t feel it.

A: The demand for AI intelligence is accelerating at an unprecedented pace. Consider this: ChatGPT reached 100 million users in just two months, far faster than platforms like Facebook, which took four and a half years to hit that milestone.23

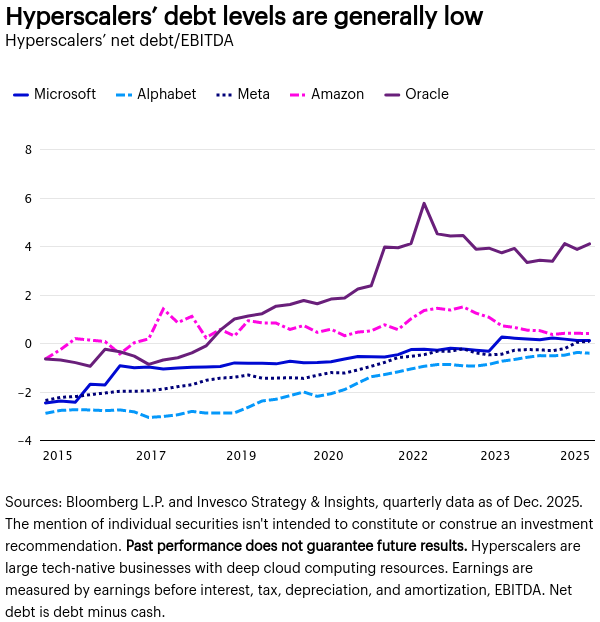

Businesses, including hyperscalers such as Amazon, Alphabet, and Meta, are pouring capital into building the computing power needed to fuel AI innovation. Fortunately, most of these companies, Oracle being a notable exception, maintain net debt (cash minus debt) to EBITDA ratios close to zero.24 In short, they have the capacity to borrow to fund investment.

The challenge, over time, will be balancing massive capital expenditure against the uncertain timing of revenue. That challenge will likely be even greater for businesses without the cash reserves hyperscalers enjoy. Timing will matter. Ultimately, it’s a race to command the most computing power.

A: Unfortunately, I wouldn’t count on it. Let’s do the math.

That math still puts mortgage rates north of 6%, give or take a few basis points. And be careful about wishing for the fed funds rate and 10-year US Treasury rate to plunge, because that would likely suggest a significantly worse economic outcome than is currently expected.

How concerned should investors be about the amount borrowed by US businesses? I posed the question to Matt Brill, Head of US Investment Grade Credit at Invesco. His response:

“We’re starting from a position of strength. Banks remain fundamentally sound and continue to improve their balance sheets,29 and the US economy is on a solid footing.30 That’s an encouraging backdrop. Most businesses in the post-COVID-19 period have been cautious. They’ve been holding back on borrowing amid waves of uncertainty, including the pandemic, the inflation surge, and higher rates in 2022, the Silicon Valley Bank failure in 2023, and tariffs in 2025. In each case, recession fears never truly materialized, but prudence prevailed. Today, companies are feeling more confident. Some are even increasing leverage to pursue acquisitions and strategic growth. Still, a general sense of caution persists when it comes to borrowing.”

Above the Noise is heading about 1,250 miles south, where it’s about 60 degrees warmer, to celebrate the holidays. Wishing you all a joyful season, and here’s to a healthy, happy, and prosperous 2026!

—

Originally Posted on December 23, 2025

Above the Noise: Rethinking 2025 narratives by Invesco US

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED

MAY LOSE VALUE

NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds. Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2024 Invesco Ltd. All rights reserved.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Invesco US and is being posted with its permission. The views expressed in this material are solely those of the author and/or Invesco US and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!