- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 11, 2024 at 11:00 am

What’s that I hear? It sounds as though hopes for a 50-basis point rate cut next week are taking a tumble.

This morning’s CPI had the potential to be a bit of an afterthought after Friday’s jobs report. We all know that the Core PCE Deflator is the Fed’s preferred inflation measure, and besides, it’s no longer all about inflation for the Fed. During his recent speech at Jackson Hole, Chair Powell reminded listeners that after years of focusing on the “stable prices” half of the Federal Reserve’s dual mandate, the central bank would now be taking the other half, “maximum employment” into greater consideration. A rate cut at next week’s FOMC meeting was all but assured.

In their usual pattern, traders were understandably hopeful that could bring about more aggressive cuts than the Fed was hinting. Remember, we begin the year with expectations for six to seven cuts. And once again, events conspired to dash most of those hopes.

After last week’s disappointing report, expectations were essentially a coin flip between 25 and 50 bp cuts. In a media appearance, I pushed back on the notion of more aggressive cuts, noting that average hourly earnings rose faster than expected in August (0.4% vs. 0.3% consensus and 0.2% in July). And while markets were understandably focused on CPI Ex-Food and Energy rising by a more-than-expected 0.3% (vs. 0.2% consensus and previous), there was far less attention paid to the fact that Real Average Earnings rose considerably more than last month on both an Hourly and Weekly basis (1.3% and 0.9% respectively, vs last month’s 0.7% and 0.4% respectively).

It is extraordinarily hard to make the case that the labor market is collapsing when wages continue to grow smartly. It also makes it harder to make the case that prices are firmly under control. Throw in the Fed’s typically unwillingness to surprise markets or take actions that could be perceived as overtly political, and we find it hard to believe that anything other than 25 bp is the likely outcome for the upcoming FOMC meeting.

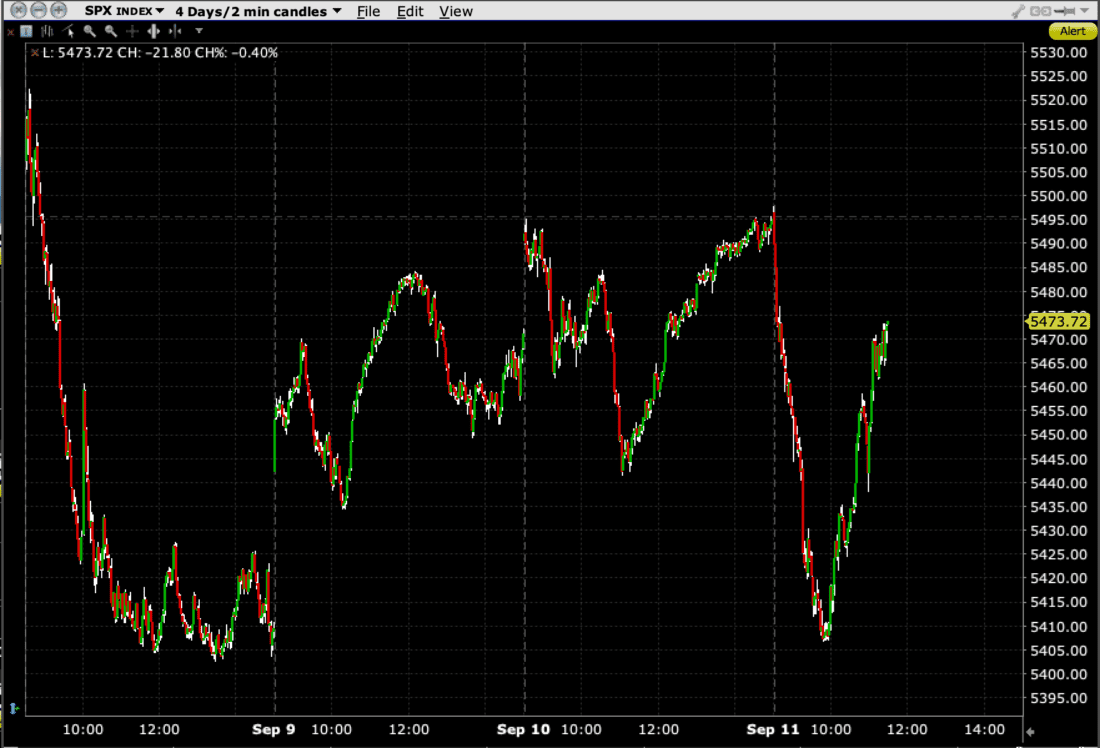

Meanwhile, the intraday volatility continues. After a morning when stocks gave back most of the gains that they recouped this week, the dip buyers returned once again. And once again, once a rally or a bounce starts, people either jump on the bandwagon or sidestep the advance:

Source: Interactive Brokers

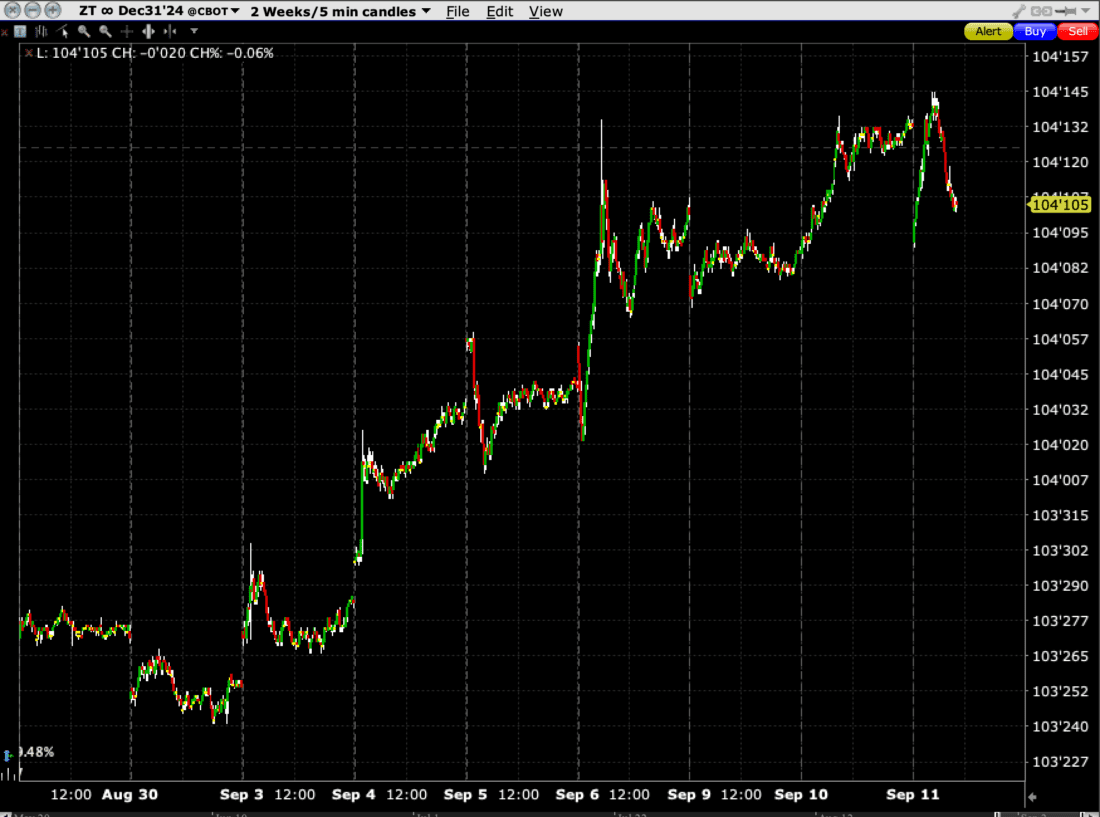

Meanwhile, 2-Year Treasuries also lack direction. Though they have steadily advanced since Jackson Hole, they have demonstrated surprising volatility of their own. Today’s trading is not as jumpy nor is the range as wide as we saw on Friday, but it is still quite volatile, nonetheless. Remember our frequently offered comment: if you can’t price risk-free assets [in this case, Fed Funds or 2-year notes], how can you expect to do so for stocks?

Source: Interactive Brokers

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

NOTHING new here, but as he (w)rote a .50 may easily/surely/beyond a doubt would/will be a fulfilling of promise powell made to biden. to me it’s a playing out of a conspiracy among big/giant shareholders of nvda who will not allow it to fall below 100. just look at the volume in it today. it took the mkt by the short ones and pulled all the tech oriented with it.

In recent history, the biggest falls in the stock market wasn’t because the Feds raised rates. The drop was because big money could earn more on their assets in investments outside of the US stock market. Each .25 drop by the Feds will see more and more US stock market liquidation and possibly a precipitous drop in all the markets.

Time will tell, but finally the time is close.