- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 23, 2026 at 10:15 am

For over a year, the U.S. dollar has been under sustained pressure. Then, in the first week of March, it suddenly found its footing, gaining over 2.5% against both the euro and the yen and then by March 16, 3% against the euro. The question isn’t whether the dollar rallied, but rather how sustainable the move is, and what it means for the broader currency landscape heading into the back half of 2026.

The catalyst was geopolitical. On Saturday, February 28, the United States launched a military offensive on Iran. Markets responded with sharp volatility across asset classes, but the most telling moves came in foreign exchange. The dollar, which had been steadily losing ground, abruptly reversed course. What followed was a chain reaction through energy markets, inflation expectations, Fed policy pricing and ultimately, currency positioning across the globe.

To understand the reversal, it helps to step back and look at the last two years. The euro had surged from $1.02 in early 2025 to $1.21 by January 2026 — an 18% gain driven by expectations of aggressive Fed easing, concerns about U.S. trade policy pushing capital away from American assets and the unwinding of a massive long-dollar positioning from late 2024. The dollar was under sustained selling pressure, and markets were positioning for continued weakness.

Then oil spiked, and everything changed.

Conflict in the Middle East triggered a sharp increase in oil prices. WTI crude oil futures rose from roughly $65 per barrel to over $119 by the March 9 trading session — an 84% gain in just over a week. That kind of upward volatility has implications far beyond the pump.

Two-year inflation breakevens spiked from 2.8% to 3.2% as markets reassessed the inflation outlook. More critically, expectations for Fed easing plummeted. Prior to the conflict, the CME FedWatch tool showed the market pricing roughly 50 basis points of rate cuts by year-end 2026. That number decreased to approximately 0 basis points of cuts by March 23.

The thesis behind this shift seems fairly straightforward: the oil spike was inflationary, and the Fed might not have the runway to ease into a softening labor market without risking a resurgence in price pressures. Higher U.S. rates, or at least the expectation of less accommodation, are a structural tailwind for the dollar. While German yields also moved higher, the differential between U.S. policy rates and those of other major economies widened materially. That’s a key fundamental driver behind the dollar’s recent strength.

So was this a safe-haven bid? The move doesn’t appear to be purely about safe-haven flows. The dollar’s 2.5% gain against both the euro and the yen was significant but not necessarily strong enough to suggest pure panic buying. If safe-haven demand were the dominant force, one might expect a more explosive reaction, particularly from the yen.

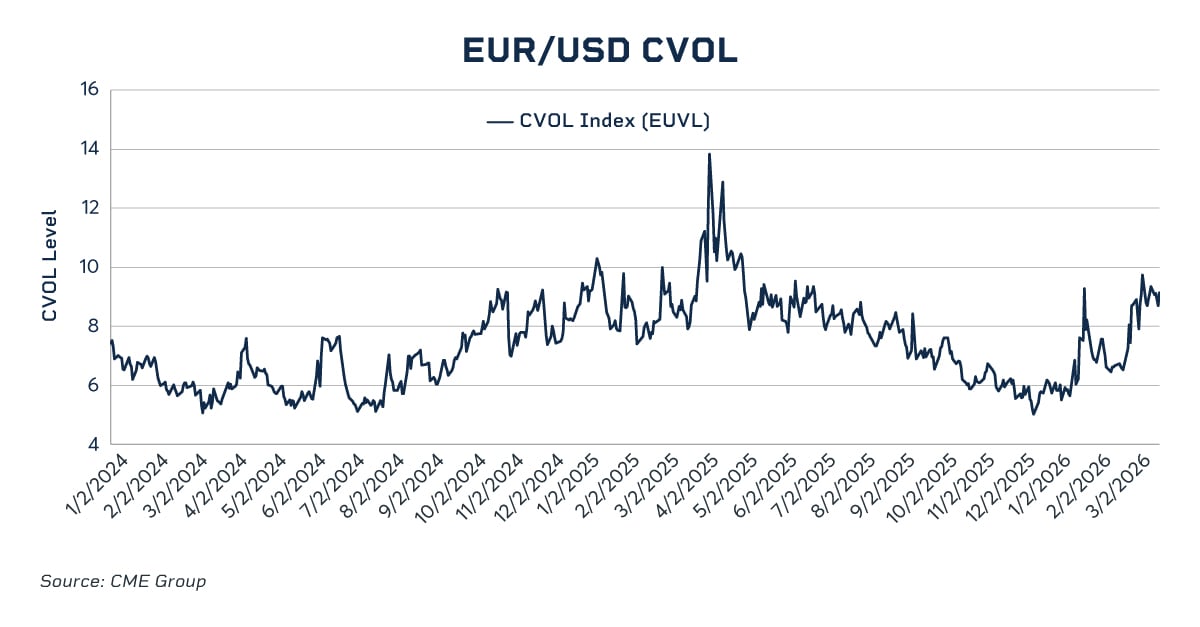

Yet there were signs of heightened risk aversion — Euro currency CVOL, a CME Group index that measures implied volatility in the euro, spiked over 30% after the conflict. While this was a substantial move, it came off of an 18-month low for the index, suggesting measured concern rather than an indication of panic.

The better explanation is a combination: some flight-to-quality demand, layered on top of a rate differential story that was already starting to favor the U.S.

This interpretation is supported by the CME Commitment of Traders (COT) tool, which showed corresponding institutional liquidation of long Euro positions that had been established during the previous period of Euro strength.

The broader dollar story is playing out unevenly across different currency pairs.

The yen’s position is particularly precarious. Japan imports virtually all of its energy, so sustained high crude prices hit its terms of trade directly. The Bank of Japan has kept rates near zero while other central banks have tightened, leaving the yen vulnerable to widening rate differential.

Commodity-linked currencies like the Australian and Canadian dollar have seen some support from higher oil prices, but that’s been offset by risk-off sentiment and concerns about global growth. The Aussie is particularly sensitive to Chinese demand, and with China’s economy still navigating structural headwinds, AUD hasn’t been able to capitalize on the commodity rally.

Emerging market (EM) currencies are another story. Higher U.S. rates and a stronger dollar create pressure for EM central banks, many of which are dealing with their own inflation challenges. If the dollar continues to strengthen, we could see renewed stress in countries with dollar-denominated debt or trade imbalances.

The British pound has been relatively resilient, trading in a narrow range against the dollar. The Bank of England has maintained a cautious stance, and while UK inflation has moderated, it hasn’t collapsed to the degree that would force aggressive easing. The pound’s near-term path will likely track the euro-dollar — if the euro weakens materially, the pound probably follows, though to a lesser degree.

The dollar’s trajectory over the rest of 2026 will likely be shaped by three forces: monetary policy divergence, geopolitical risk and U.S. trade policy. Right now, the first two favor the dollar, while the third cuts against it. Below are three potential scenarios to consider:

Positioning matters too. The massive build-up of euro longs during 2025’s rally hasn’t entirely unwound. If safe-haven buying continues and those positions get squeezed, euro liquidation could accelerate the dollar’s move lower. From a technical perspective, euro-dollar is testing key support around $1.15, with a break below opening the door to $1.10. For dollar-yen, the ¥150 level is psychologically important.

For those looking to hedge currency exposure or express a directional view, CME Group offers efficient tools across multiple pairs. Euro FX futures provide meaningful capital efficiency at nearly 50-to-1 leverage, while Micro contracts (one-tenth the size) allow for tighter risk management. Similar Micro contracts exist for the yen, pound and other major currencies.

The most prudent posture for traders is cautious and nimble. The landscape can shift quickly, and proper position sizing matters more than usual in this environment. The dollar is having a moment — whether it’s a short-term bounce or the beginning of a sustained reversal will depend on how the next few months unfold.

—

Originally Posted April 2026 – Dollar Reasserts Itself as Global Tensions Shift Currency Markets

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Spot currencies are not available at IBKR Singapore.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!