- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 5, 2025 at 10:15 am

US policy is injecting a new level of uncertainty into the global outlook. Volatility is up across all financial assets, and bonds have not escaped. So, how are short term bonds holding up? The “short” answer is: pretty well.

In a world where a news headline or a tweet can shift markets rapidly and significantly, short dated bonds have offered a degree of comparative stability year-to-date.

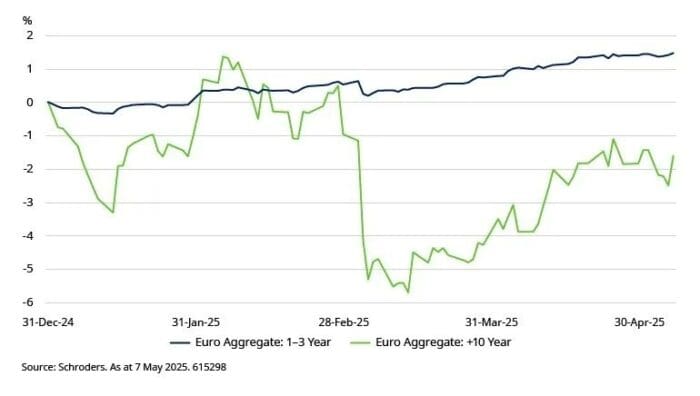

It’s most obvious in eurozone markets, where a more protectionist US has corresponded with a seismic shift in the German fiscal landscape, driving longer dated bond yields higher.

The chart below compares the performance of the Bloomberg Euro Aggregate Index (composed of government bonds, credit and securitised) in the 1-3 year sector with the +10 year sector.

As you can see, the much smoother appreciation of the short dated bond market year-to-date is in contrast to the considerably higher volatility and underperformance of longer maturity bonds.

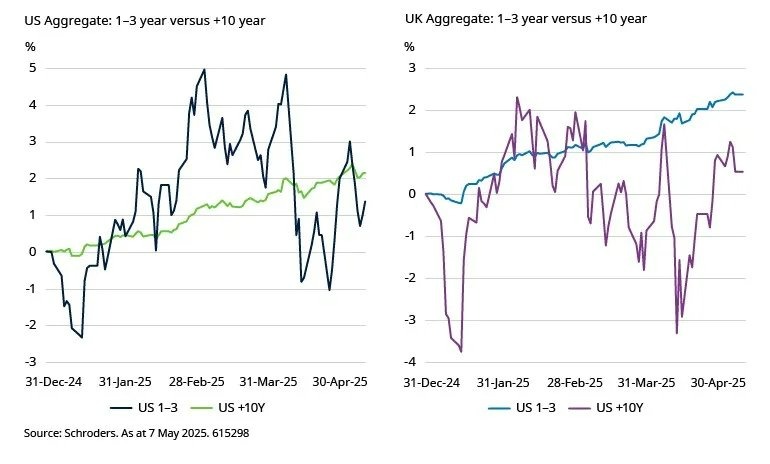

But it’s not just eurozone markets – it’s a similar story in the US and the UK as well. Here too, longer maturity bonds have underperformed and exhibited – as we would expect given the higher level of interest rate risk – greater volatility.

A lot of the outperformance of short dated bonds year-to-date has been attributed to the steepening of yield curves. Yields have fallen in the shorter end of the curve – as central banks maintained their easing bias – and in most cases have risen in the longer end of the curve, as the term premium* has increased.

As we know, yields move inversely to price, so as illustrated below, the year-to-date price return of the 1-3 year sector was positive, with an additional coupon return boosting the overall total return.

In comparison, the +10 year sector saw total return losses as the (albeit higher) coupon return was insufficient to offset the losses from rising yields.

However, despite the recent steepening, curves remain pretty flat from a historical perspective, which means investors gain comparatively attractive yield, for a lot less duration (or interest rate risk).

With the Zero Interest Rate Policy (ZIRP) days now behind us, income has thankfully once again become a more significant part of bond returns. While this is true whichever maturity you’re looking at, the much lower duration associated with short dated bonds means this steady income stream is a greater proportion of this sector’s total return stream.

Put another way, the buffer or protection from capital losses for short dated bonds is greater as the yield per unit of interest rate risk is higher.

This is illustrated in the chart below, which shows the breakeven levels (the move in yield required to wipe out the return from income over a 12 month period) comparing short and long dated eurozone bond markets.

We’re not saying that this section of the curve won’t incur losses, but the higher the breakeven, the more protection you have.

We may be at peak uncertainty – or we may not. What we can say with certainty is that short dated fixed income has a strategic role to play in a broader investment portfolio.

As cash rates fall, short dated fixed income can offer the stepping stone investors are looking for to move out of cash or diversify a broad portfolio of investments in order to reduce the volatility of returns. The consistent level of income now – as it did in the past – helps to limit market volatility, which is particularly useful when the economic outlook has the potential to switch at a moment’s notice.

Given the current environment, it’s important to remember that it’s no longer as simple as just buying bonds and investors need to mindful of curve positioning as well as divergence by geography and asset class. That’s why an actively managed short dated bond fund ticks many of the boxes for investors looking to diversify the risk of their portfolio, particularly one that has the ability to react quickly to a changing and challenging market environment.

* Term premium is this additional return (yield) you receive for taking on the extra risk of locking your money away for, say, ten years compared to reinvesting cash in risk-free securities as they mature multiple times, such as one-month bills for ten years.

The views and opinions contained herein are those of Schroders’ investment teams and/or Economics Group, and do not necessarily represent Schroder Investment Management North America Inc.’s house views. These views are subject to change. This information is intended to be for information purposes only and it is not intended as promotional material in any respect.

—

Originally Posted on June 1, 2025 –

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!