- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 2, 2023 at 10:40 am

By: Kaiko

The best design often goes unnoticed. DeFi lending and borrowing stalwarts Aave and Compound have proven themselves to be great design: critical for day-to-day functioning but largely taken for granted. This becomes apparent when a competitor experiences an exploit, highlighting the reliability of Aave and Compound[1].

When last we checked in on these protocols in December they were in a period of change. Avraham Eisenberg – since charged by the DOJ – had just attempted to exploit Aave by borrowing CRV. This event forced lending and borrowing protocols to rethink their asset policies, ultimately choosing to limit the assets that users could deposit and borrow to only the most liquid, such as ETH, USDC, and USDT.

Aave and Compound had also just started rolling out their V3s on Ethereum, which are significantly different from their previous versions. This week, we’ll examine how Aave and Compound’s V2s have fared since last year, then cover the adoption of their V3s and potential competitors.

The number of unique users for each protocol has declined steadily since May 2022; Compound’s decline in users has been more pronounced. The only months that have bucked this trend were November 2022 (when FTX collapsed) and March 2023 (when USDC depegged).

February 2023 was a particularly slow month, with just over 3,500 monthly users of Aave V2 and 1,000 of Compound V2. For reference, you are more likely to meet an active NFL player than you are to meet someone who used Compound V2 in February.

Meanwhile, monthly deposit volume has been depressed since the bear market. Aave averaged around $8bn in monthly deposits at the beginning of 2022.

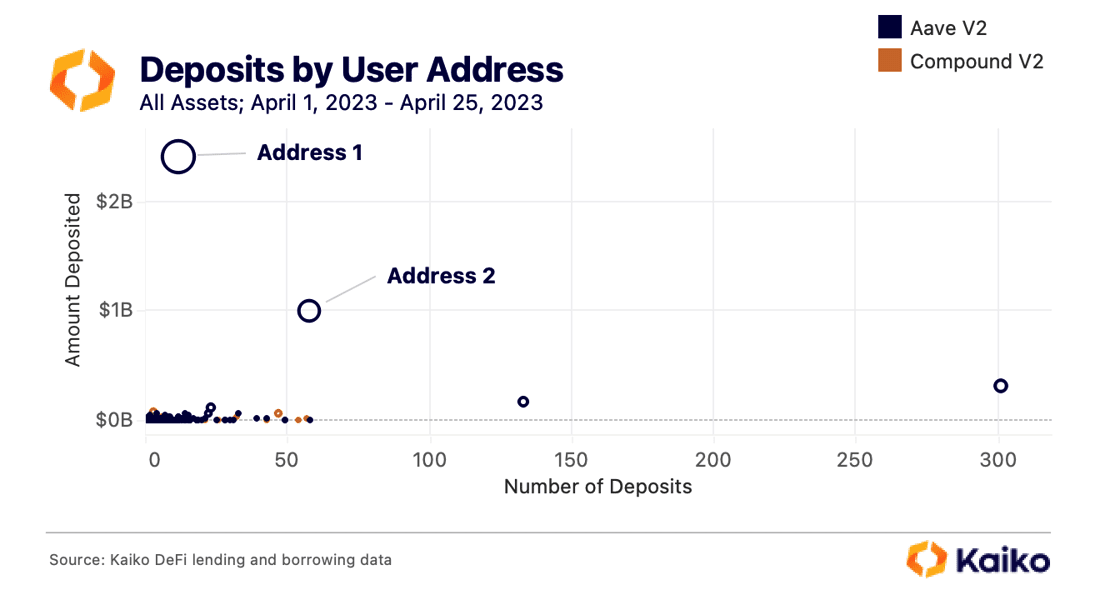

This year’s average has been about half that, approximately $4bn. The obvious exception of March, when flash loans – in which tokens are deposited and withdrawn in the same block – accounted for $10bn of deposits in just three days, which I’ve covered in more detail here. Like many things in DeFi, activity is driven by whales and bots. Since the start of April, just two addresses have been responsible for $3.4bn of Aave’s $5.1bn deposit volume: over 65%.

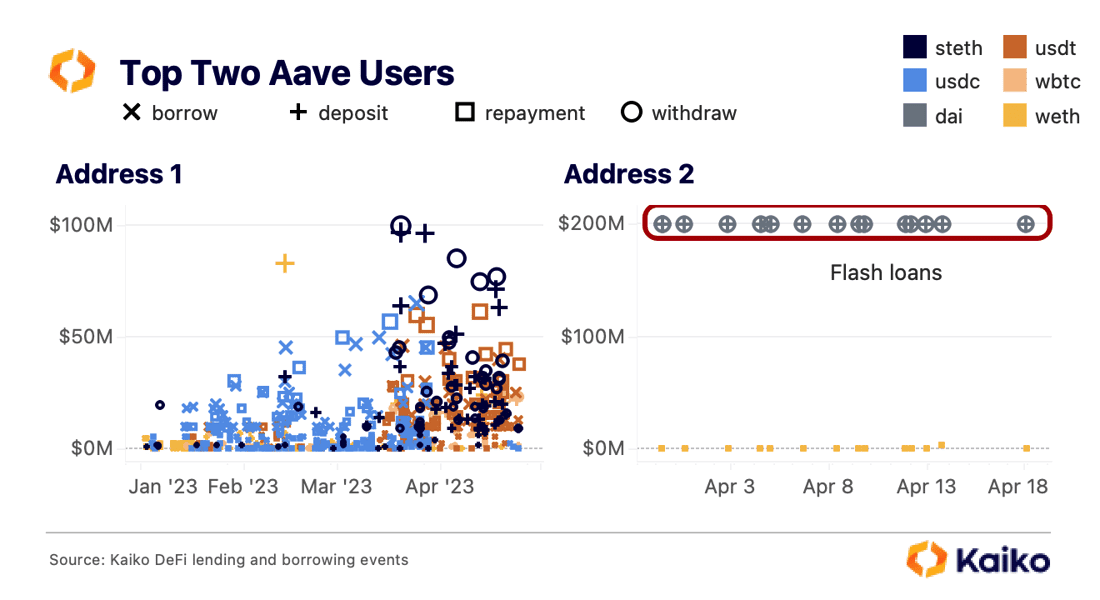

This becomes even more interesting when examining the activity of these two addresses. The recent activity of these two addresses is charted below. Note that the address on the left has been active since April 2022 while the address on the right has been active since March 30, 2023.

I had anticipated that both of these addresses would be bots, but it appears that the most active address is not: the activity looks organic and doesn’t have the simultaneous deposit and withdrawal that is the telltale sign of a flash loan. It’s also interesting to note that this account has largely shifted from borrowing USDC to borrowing USDT since mid-March, right after USDC depegged.

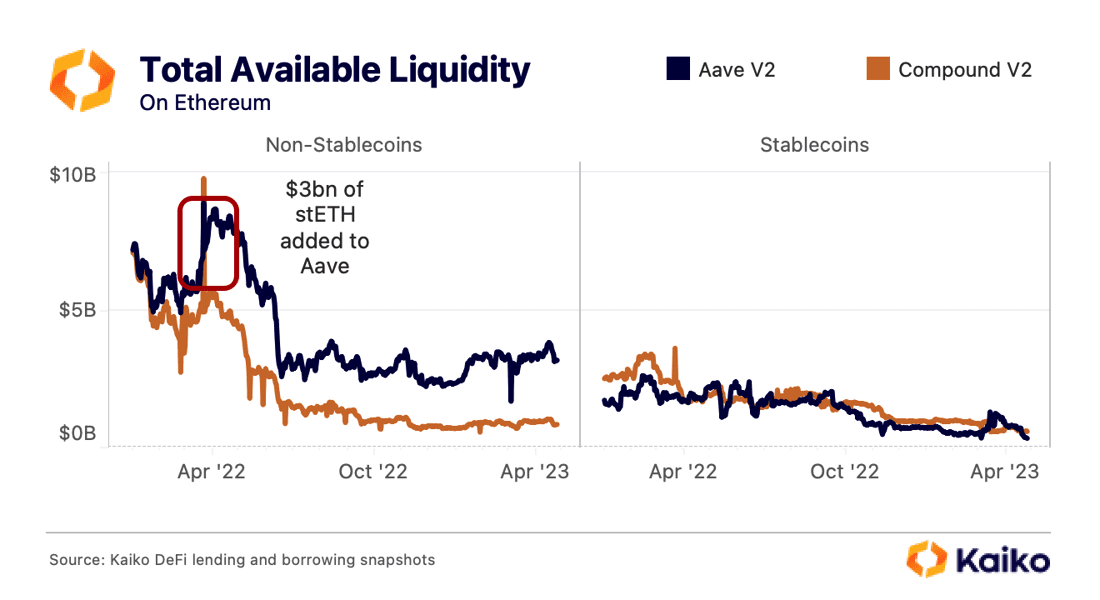

While lending and borrowing events provide a nice view of who is using the protocols and how, snapshots are helpful to get a broader picture of their status. Below is the total available liquidity (or sum of tokens deposited) on both Aave and Compound V2, split into stablecoins and non-stablecoins to mitigate the effect of price changes.

Both protocols have followed roughly the same pattern, shrinking significantly in both the stablecoin and non-stablecoin categories. Aave V2 made the savvy move to allow stETH deposits, which quickly netted it over $3bn of deposits in just a couple months, helping to explain the persistent gap between the two protocols.

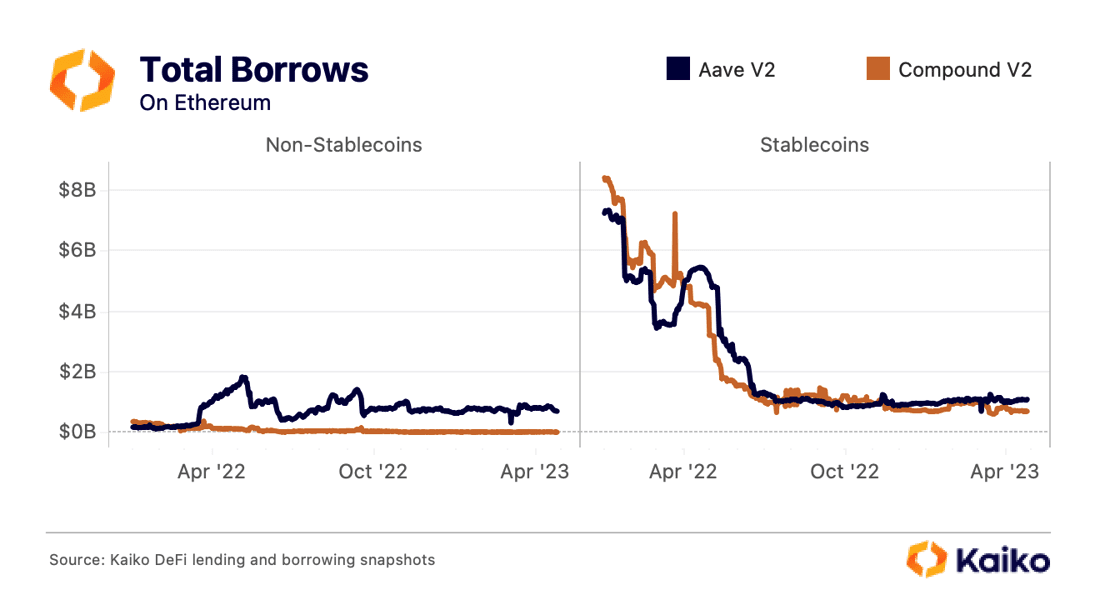

Next, we can examine the total borrows on each protocol. Notably, there is no significant drop in either available liquidity above or borrows below since both protocols began rolling out their V3s at the end of last year.

Compound’s lead in stablecoin borrows at the beginning of last year has evaporated, while Aave quickly expanded its lead in non-stablecoin borrows thanks to heavy ETH borrowing during the spring of 2022. A large portion of this was likely driven by users manually leveraging their stETH: depositing stETH, borrowing ETH, then staking it for stETH. This process can be repeated multiple times.

Currently, ETH is the most borrowed asset on Aave while DAI is the most borrowed on Compound. Meanwhile, stETH is the most deposited on Aave and ETH is the most deposited on Compound.

As I mentioned above, there is no obvious indication in the data that the V3s were ever released, no obvious rush of liquidity out of either protocol. Thus it appears that these protocols may follow a similar pattern as Uniswap, whose V2 still serves a niche and registers significant volumes.

Both V3s have achieved notable adoption in their first few months of existence, with Aave V3 reaching $750mn of available liquidity on Ethereum ($1.3bn total across 7 chains) while Compound has nearly $500mn of collateral deposited across its two available markets. It appears that Compound has learned from Aave’s success with stETH, as its V3 allows users to deposit both Coinbase Wrapped Staked ETH (cbETH) and Lido Wrapped Staked ETH (wstETH) as collateral to borrow ETH. Aave V3 allows for depositing and borrowing of cbETH, rETH, and wstETH.

Additionally, there are ongoing governance discussions surrounding Aave’s Safety Module, which holds AAVE tokens and LP tokens that can be sold to backstop the protocol in the event of a shortfall. I’ve discussed in more detail previously, but I still believe that the Safety Module containing mostly AAVE tokens provides little safety while being a significant risk to the token’s price. The governance proposals have suggested adding deeply liquid assets like ETH and USDC. This is a good idea, and I believe they should go a step further and consider removing AAVE from the Safety Module entirely.

Meanwhile, there are new competitors that have added some intrigue to the space. The first that I’ve been watching is Morpho, which adds a P2P layer to both Compound and Aave and has been growing steadily[2]. The next is Radiant Capital, whose token RDNT is up about 10x since the start of the year as it has proven itself to be the most popular lending protocol on Arbitrum by TVL, slightly beating out Aave. But, to truly challenge Aave and Compound, these protocols must prove themselves to be secure; Euler Finance provides a cautionary tale of a lending and borrowing protocol that seemed to be doing everything right, only to be undone by an exploit.

[1] Compound has been exploited for nearly $150mn, though it was related to the COMP token rather than the protocol’s actual architecture, making it more of a “bank error” than an exploit, as described by Rekt.

[2] Its token isn’t tradeable yet but is being used to incentivize lending and borrowing on the protocol.

—

Originally Posted April 27, 2023 – Leveraging LSDs: The Next Era of Lending and Borrowing

Smartkarma posts and insights are provided for informational purposes only and shall not be construed as or relied upon in any circumstances as professional, targeted financial or investment advice or be considered to form part of any offer for sale, subscription, solicitation or invitation to buy or subscribe for any securities or financial products. Views expressed in third-party articles are those of the authors and do not necessarily represent the views or opinion of Smartkarma.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Smartkarma and is being posted with its permission. The views expressed in this material are solely those of the author and/or Smartkarma and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!