- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 27, 2026 at 1:15 pm

Another day, another rally. Last week’s mini-shakeout seems to have convinced investors that stocks are relatively impervious to bad news. It vindicated the dip buyers, which we saw in force, and has converted many of them into rally chasers. Traders seem very sanguine about earnings overall and megacap tech specifically, and a push to the 7,000 level on the S&P 500 (SPX) seems all but inevitable. As we noted yesterday, VIX and VIX9D, its 9-day version, both show a relative lack of concern about impending volatility (remember, these are volatility measures, not fear gauges) ahead of a consequential slew of news.

I count 124 SPX companies reporting this week – almost exactly ¼ of the index. We have the usual vast majority of companies beating EPS estimates, which is a necessary, but not sufficient, condition for a post-earnings bounce. However, the response to guidance has been mixed. The latter is the necessary condition for a rally. Remember, stocks are forward-looking, while last quarter’s earnings tell us about the immediate past and maybe the present. Thus, we care more about guidance.

It’s also a bit concerning when stocks run up ahead of earnings because that raises the bar that they must hurdle over. It was particularly nasty as Intel (INTC) ran up ahead of an earnings miss last week. We saw something similar for some big banks as earnings season kicked off, though today we saw Boeing (BA) rise after a similar early dip. With Apple (AAPL) and Microsoft (MSFT) moving higher again today, and Meta Platforms (META) and Tesla (TSLA) barely pulling back after their own recent bumps, that concern must be noted ahead of these companies’ earnings tomorrow (META, MSFT, TSLA) and Thursday (AAPL).

And oh, we have an FOMC meeting tomorrow. Options traders seem to be implying that the lack of news will be interpreted as good news. We have noted that market expectations for a rate cut announcement tomorrow are essentially nil, and that any post-decision move will more likely be predicated upon the number and types of dissents along with the now lame-duck Chair’s comments not only about rates but about the political winds swirling around the Fed. (By the way, I assign a low but finite probability to the idea that the President will announce his pick for the next Fed Chair sometime between 1:30 and 4 PM ET tomorrow, and a relatively high probability to another set of negative comments about Chair Powell regardless.)

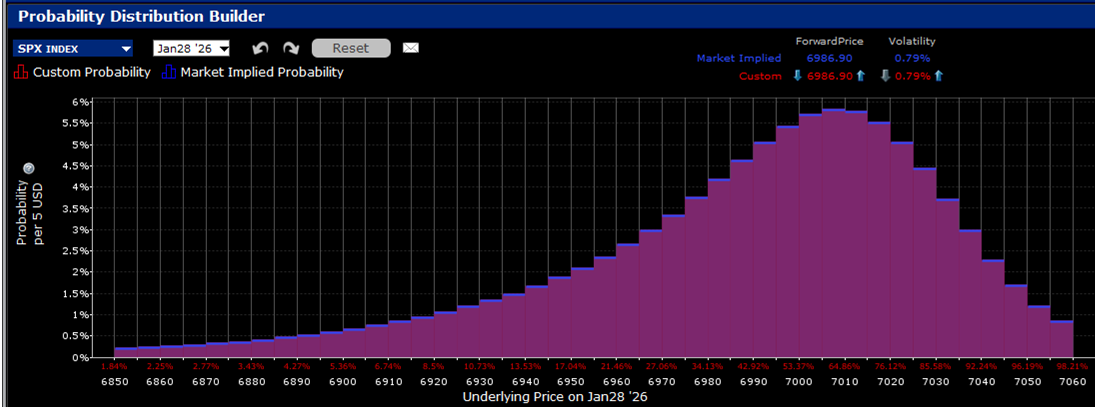

As is now customary, SPX options traders are assigning their highest probabilities to upward moves over the coming week. For SPX options expiring tomorrow, the probability peak is around 7,010; for those expiring Friday, that peak is around 7,040. While this looks sanguine, if not complacent – and it is – the bias is rational. If there is a consensus expecting stocks to continue their pattern of rising on a daily basis, options pricing will reflect that.

Source: Interactive Brokers

Source: Interactive Brokers

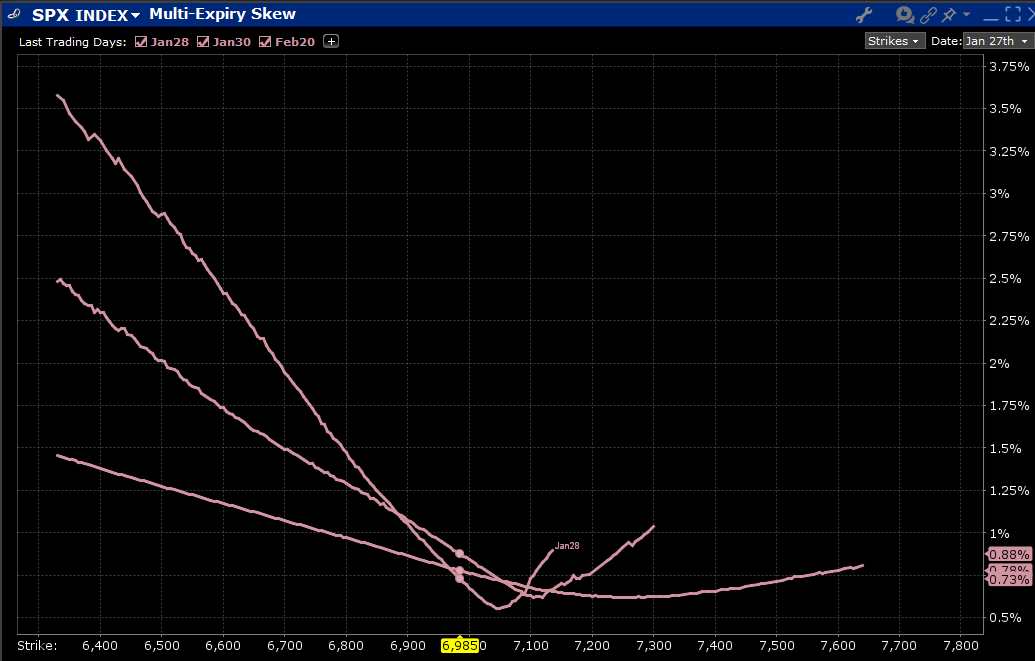

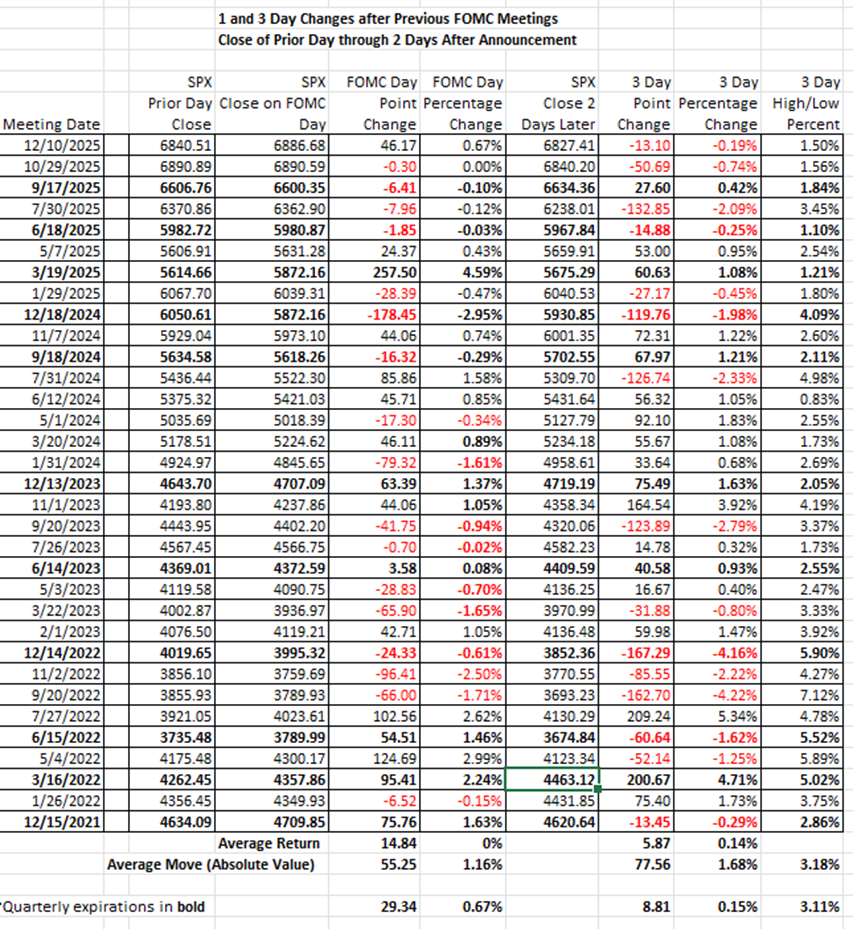

When we look at near-term skews, we see at-money volatilities pricing in moves of less than 1%, with even lower implied vols in above-market strikes (reflecting the probabilities displayed above). The average daily move on the afternoons of FOMC meetings since December 2021 is 1.16%, but we have not seen a Wednesday afternoon move of more than 1% since March 2025. We do see a fair degree of risk aversion in downside options though, particularly for those expiring tomorrow. For contrast, note the relatively normal skew for options expiring on the regular monthly date. Note that four of the last five FOMC events showed modest downturns on both one-day and three-day bases.

Source: Interactive Brokers

Bottom line, options traders are not particularly concerned ahead of tomorrow’s FOMC meeting. Should we be fearful that they seem to be greedy? We’ll find out soon enough.

Source: Interactive Brokers

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

“Traders seem very sanguine about earnings overall and megacap tech specifically,” well put. It is good to be able to short heavily when it becomes what it was instead of what it is.