- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 28, 2026 at 12:43 pm

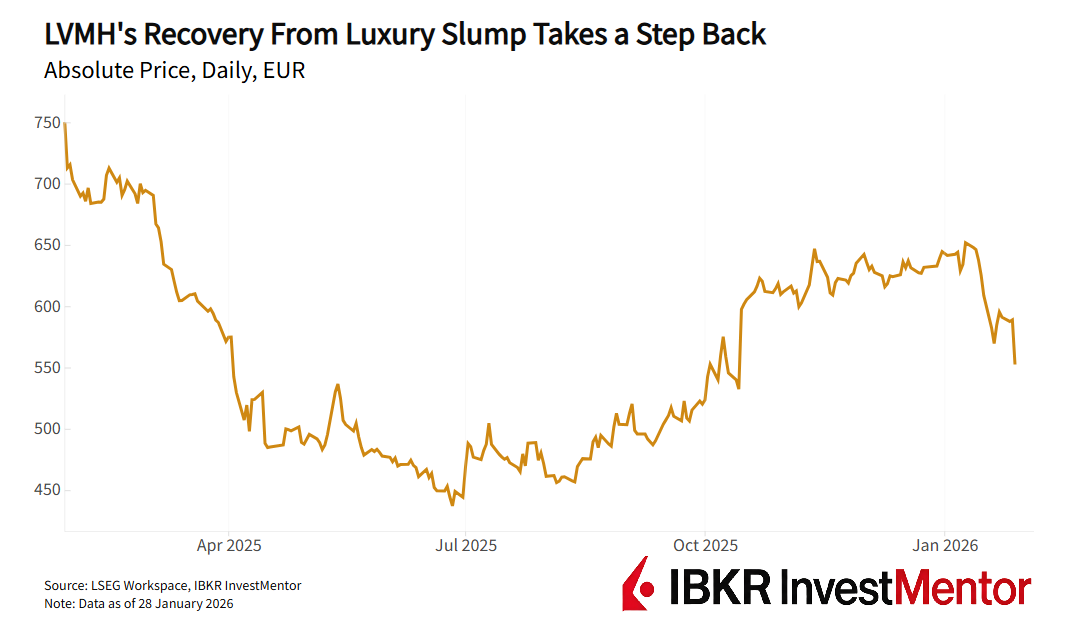

LVMH’s latest earnings were supposed to steady the ship. Instead, they reminded investors just how choppy the waters remain for global luxury.

The world’s largest luxury group beat expectations in the final quarter, reporting €22.7 billion in revenue — a 1% like‑for‑like rise from the year before, versus forecasts of a slight decline. Usually, a beat would have buoyed the sector. Instead, the stock sank 8% in Paris, dragging the entire luxury complex down with it.

The problem wasn’t the headline number. It was everything underneath it. LVMH’s fashion and leather goods division, the workhorse of the empire, posted a 3% year‑on‑year decline. Sales in Asia, including the crucial Chinese market, rose just 1%. After upbeat results from rivals Richemont and Burberry earlier, investors had been primed for a stronger signal that the luxury slump was yesterday’s news.

They didn’t get it. And Bernard Arnault didn’t sugar‑coat the mood. “With the continuing geopolitical crises, with economic uncertainty and the policies of certain states… to tax us to the maximum and create unemployment, I think there is reason to be a little cautious,” he told analysts on the earnings call.

This didn’t go down well with the investors.

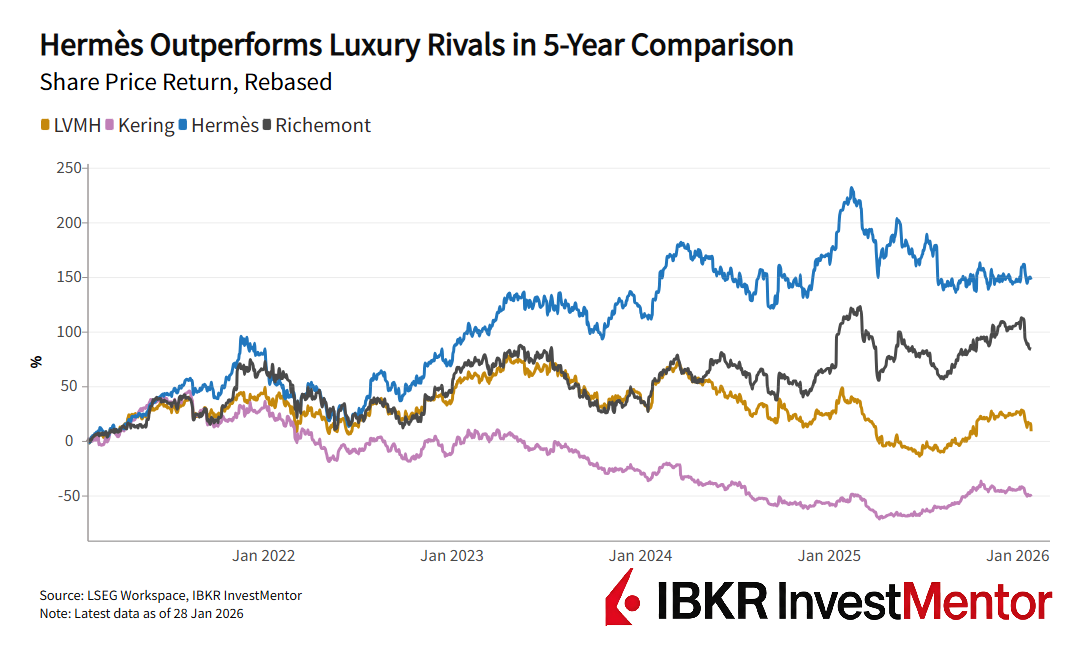

When LVMH stumbles, the rest of the industry feels it. The French group has a market cap of about €270 billion ($325 billion) and a rich portfolio of everything luxury from fashion and perfumes to watches, jewelry, and champagne. Not only does it own Louis Vuitton brand, but also Tiffany, Dior, Kenzo, Celine, Rihanna’s Fenty, and Dom Pérignon, among others. It also runs beauty retailer Sephora.

Competitors Burberry, Kering, Hermès, Richemont, and Moncler all lost between 2% and 4% on the day. Investors were reassessing the entire sector’s trajectory.

Luxury is a confidence game. It relies on affluent consumers feeling flush, tourists travelling freely, and markets believing in long‑term brand power. When the bellwether signals caution, the whole system recalibrates.

For all the talk of diversification, China remains the luxury sector’s gravitational center. Between 2019 and 2023, Chinese luxury spending grew more than 18% annually. Then came the reversal: a sharp drop in 2024 and a flat 2025.

Chinese shoppers, both domestic and travelling, account for nearly a third of LVMH’s fashion and leather sales. When they return, the sector rallies. When they hesitate, valuations wobble.

LVMH did report signs of improvement, but the recovery is uneven. A property downturn in China, rising competition from local brands, and a shift away from logo‑heavy conspicuous consumption are reshaping demand. Investors hoping for a clean, V‑shaped rebound are discovering that this cycle is more complicated.

Tariffs, Politics, and the Champagne Problem

Even if demand stabilizes, luxury faces another headwind: geopolitics.

The US has struck a series of deals, bringing tariffs down from the levels threatened by the White House back in April 2025. But LVMH still must deal with 15% tariffs on most European goods shipped to the US, for example.

Geopolitical flare-ups don’t help. Recent on-off tariffs over Greenland and a quip by US President Donald Trump to ramp up tariffs on French wines to 200% over a diplomatic spat all unnerved the investors. For LVMH, the world’s leading champagne producer, comments like this matter.

Luxury thrives on stability as it’s the first thing consumers skimp on when times are tough.

Beyond the macro story lies a more personal one: who succeeds Bernard Arnault?

At 76, Arnault has led LVMH since 1989 and has occasionally topped global wealth rankings. The company recently extended the age limit for the combined CEO‑and‑Chair role to 85, effectively giving him another decade at the helm. But he has not named a successor. All five of his adult children hold senior roles within the group, and investors are left to read tea leaves.

Some shareholders say the lack of clarity is becoming a governance concern. Analysts note that while there’s no obvious “succession discount” in the share price yet, the issue is gaining prominence. In a sector built on heritage and continuity, uncertainty at the top of its most powerful house is no small matter.

It’s a real‑world Succession storyline — minus the HBO writers, but with far more capital at stake.

LVMH’s results didn’t signal a crisis. But they did puncture the idea that luxury’s rebound would be smooth or swift. China is recovering, but unevenly. Tariffs remain a wild card. Margins are under pressure. And the Arnault succession question looms larger with each passing year.

The easy gains of the post‑pandemic boom are gone.

Download IBKR InvestMentor app for more daily explainers on market news and free courses on investing.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!